From Scale Monopoly to Green Specialty: Unpacking the 2025 Global Petrochemical Bifurcation

Date : 2026-03-28

Reading : 154

The global petrochemical industry has entered a brutal era of structural out-clearing. Battered by cyclical headwinds, including depressed Brent crude averages ($69.1/barrel) and severe overcapacity in the Asia-Pacific region, the competitive landscape in 2025 is no longer defined by mere capacity expansion. Based on a comprehensive financial and strategic audit of nine industry titans—BASF, Dow, ExxonMobil, Sinopec, Saudi Aramco, LG Chem, Lotte Chemical, Petronas Chemicals (PCG), and IRPC—HDIN Research reveals a fundamental bifurcation in sector positioning. The new strategic moats are strictly divided into two distinct survival pathways: extreme upstream feedstock integration and high-margin green specialty materials.

Figure 2025 Global Petrochemical Strategic Benchmarking

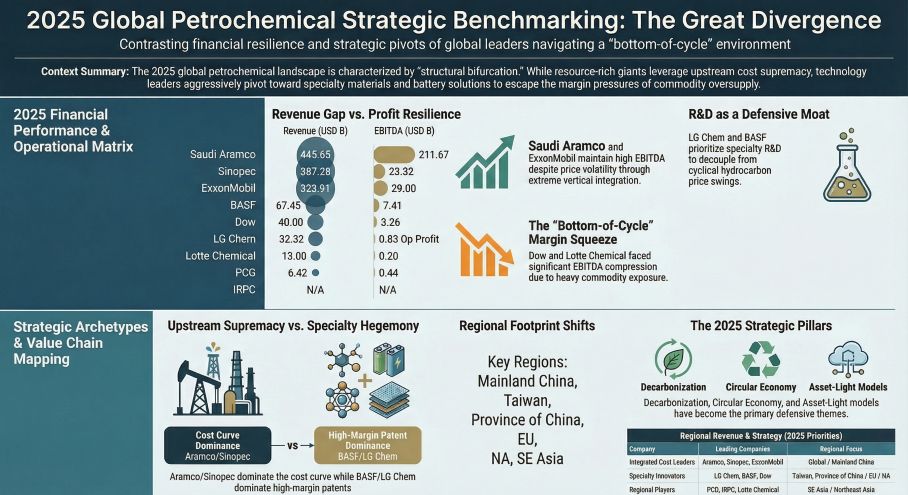

Sector Positioning: The Dual-Track Bifurcation

Sector Positioning: The Dual-Track Bifurcation

The traditional homogenised approach to petrochemicals is dead. Our analysis categorizes the current competitive dynamics into two dominant ecosystems:

* The Integrated Resource Titans (Saudi Aramco, Sinopec, ExxonMobil): These giants rely on extreme capital allocation efficiency and absolute raw material dominance. Saudi Aramco's unparalleled upstream lifting cost ($3.51/boe) and ExxonMobil’s North American ethane "feed advantage" provide them with a profound pricing buffer. Sinopec, generating nearly $387.2 billion in revenue, leverages its unmatched domestic refining scale and retail network of over 31,000 service stations to ensure base-cost absorption.

* The Specialty & Material Innovators (BASF, Dow, LG Chem): Facing margin compression in bulk commodities, these players are pivoting heavily into proprietary technologies. LG Chem has effectively transitioned into a semi-energy company, with battery solutions now driving over 51% of its revenue. BASF is doubling down on its "Verbund" (highly integrated) operational efficiency while shedding non-core assets, and Dow is aggressively pruning low-margin siloxane operations to focus on high-yield circular polymers and EV electronic materials.

Regional players like Lotte Chemical, PCG, and IRPC are caught in the crossfire. Lacking the upstream cost hegemony of Aramco or the R&D war chests of BASF, they face severe margin squeezes, rendering their survival dependent on capturing hyper-niche markets and optimizing localized supply chains.

Financial Health & Capital Allocation Efficiency

A forensic review of 2025 financial disclosures indicates a sector-wide "Big Bath" strategy. Operating cash flows and net profits have severely decoupled as companies aggressively write down assets to prepare for future cycles.

* Strategic Impairments: Saudi Aramco and Dow recorded massive asset impairments ($8.6 billion and $1.86 billion, respectively), heavily driven by European and US asset restructuring. Sinopec also utilized the cyclical trough to cleanly execute large-scale write-downs while sustaining an exceptionally robust operating cash flow of $24.67 billion.

* Hidden Balance Sheet Risks: South Korean conglomerates are exhibiting elevated off-balance-sheet vulnerabilities. LG Chem holds roughly $7 billion in debt guarantees for its global battery subsidiaries, highly sensitive to EV market fluctuations. Concurrently, Lotte Chemical's Indonesian integrated project (LCI) recently required waivers for core financial covenants, signaling acute liquidity constraints amid tightening spreads.

Geopolitical Headwinds & Supply Chain Resilience

In an era of rising trade protectionism and geopolitical volatility, supply chain resilience has become a critical valuation metric. A simulated blockade of the Strait of Hormuz vividly illustrates this risk asymmetry. Under an extreme crude price spike, ExxonMobil’s LIFO (Last-In, First-Out) inventory accounting and Dow’s North American ethane reliance would trigger immense global arbitrage opportunities and margin expansion. Conversely, import-dependent models like Europe-based BASF and Thailand's IRPC would face devastating EBIT collapses due to unmanageable naphtha and freight cost inflations.

Furthermore, localization in Asia remains a double-edged sword. While BASF initiates trial operations at its €8.7 billion Zhanjiang Verbund site and ExxonMobil launches its Huizhou complex, this influx of localized foreign capacity is exacerbating China’s structural overcapacity, effectively destroying the remaining spread margins for standard petrochemicals in 2026.

Strategic Pivots: Capex in Green Moats

Environmental compliance has evolved from a regulatory cost to a definitive "green entry barrier." Capital expenditure in 2025 confirms that the transition to circular economies is fully industrialized.

* Carbon Pricing as a Capex Filter: BASF has weaponized internal carbon pricing, setting thresholds as high as €365/ton, deliberately raising the hurdle rate for high-emission investments.

* CCS and Hydrogen Monopolies: ExxonMobil’s dedicated Low Carbon Solutions (LCS) unit and Saudi Aramco’s aggressive Blue Hydrogen (BHIG) acquisitions are locking down the Carbon Capture and Storage (CCS) infrastructure. Without access to these proprietary emission-reduction technologies, regional manufacturers facing the EU’s expanded CBAM (Carbon Border Adjustment Mechanism) will soon find their exports priced out of western markets entirely.

HDIN Viewpoint

HDIN Research posits that the global petrochemical market has crossed the Rubicon. The era of riding macroeconomic growth for bulk chemical profitability is over. The survivors of the 2025-2026 shakeout will be those who successfully fuse "cost-plus" resource dominance with "patent-protected" green specialty premiums. Institutional investors must scrutinize the widening gap between cash flow quality and reported book profits, while aggressively discounting regional operators who lack definitive CCS roadmaps or upstream feedstock sovereignty.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure 2025 Global Petrochemical Strategic Benchmarking

Sector Positioning: The Dual-Track BifurcationThe traditional homogenised approach to petrochemicals is dead. Our analysis categorizes the current competitive dynamics into two dominant ecosystems:

* The Integrated Resource Titans (Saudi Aramco, Sinopec, ExxonMobil): These giants rely on extreme capital allocation efficiency and absolute raw material dominance. Saudi Aramco's unparalleled upstream lifting cost ($3.51/boe) and ExxonMobil’s North American ethane "feed advantage" provide them with a profound pricing buffer. Sinopec, generating nearly $387.2 billion in revenue, leverages its unmatched domestic refining scale and retail network of over 31,000 service stations to ensure base-cost absorption.

* The Specialty & Material Innovators (BASF, Dow, LG Chem): Facing margin compression in bulk commodities, these players are pivoting heavily into proprietary technologies. LG Chem has effectively transitioned into a semi-energy company, with battery solutions now driving over 51% of its revenue. BASF is doubling down on its "Verbund" (highly integrated) operational efficiency while shedding non-core assets, and Dow is aggressively pruning low-margin siloxane operations to focus on high-yield circular polymers and EV electronic materials.

Regional players like Lotte Chemical, PCG, and IRPC are caught in the crossfire. Lacking the upstream cost hegemony of Aramco or the R&D war chests of BASF, they face severe margin squeezes, rendering their survival dependent on capturing hyper-niche markets and optimizing localized supply chains.

Financial Health & Capital Allocation Efficiency

A forensic review of 2025 financial disclosures indicates a sector-wide "Big Bath" strategy. Operating cash flows and net profits have severely decoupled as companies aggressively write down assets to prepare for future cycles.

* Strategic Impairments: Saudi Aramco and Dow recorded massive asset impairments ($8.6 billion and $1.86 billion, respectively), heavily driven by European and US asset restructuring. Sinopec also utilized the cyclical trough to cleanly execute large-scale write-downs while sustaining an exceptionally robust operating cash flow of $24.67 billion.

* Hidden Balance Sheet Risks: South Korean conglomerates are exhibiting elevated off-balance-sheet vulnerabilities. LG Chem holds roughly $7 billion in debt guarantees for its global battery subsidiaries, highly sensitive to EV market fluctuations. Concurrently, Lotte Chemical's Indonesian integrated project (LCI) recently required waivers for core financial covenants, signaling acute liquidity constraints amid tightening spreads.

Geopolitical Headwinds & Supply Chain Resilience

In an era of rising trade protectionism and geopolitical volatility, supply chain resilience has become a critical valuation metric. A simulated blockade of the Strait of Hormuz vividly illustrates this risk asymmetry. Under an extreme crude price spike, ExxonMobil’s LIFO (Last-In, First-Out) inventory accounting and Dow’s North American ethane reliance would trigger immense global arbitrage opportunities and margin expansion. Conversely, import-dependent models like Europe-based BASF and Thailand's IRPC would face devastating EBIT collapses due to unmanageable naphtha and freight cost inflations.

Furthermore, localization in Asia remains a double-edged sword. While BASF initiates trial operations at its €8.7 billion Zhanjiang Verbund site and ExxonMobil launches its Huizhou complex, this influx of localized foreign capacity is exacerbating China’s structural overcapacity, effectively destroying the remaining spread margins for standard petrochemicals in 2026.

Strategic Pivots: Capex in Green Moats

Environmental compliance has evolved from a regulatory cost to a definitive "green entry barrier." Capital expenditure in 2025 confirms that the transition to circular economies is fully industrialized.

* Carbon Pricing as a Capex Filter: BASF has weaponized internal carbon pricing, setting thresholds as high as €365/ton, deliberately raising the hurdle rate for high-emission investments.

* CCS and Hydrogen Monopolies: ExxonMobil’s dedicated Low Carbon Solutions (LCS) unit and Saudi Aramco’s aggressive Blue Hydrogen (BHIG) acquisitions are locking down the Carbon Capture and Storage (CCS) infrastructure. Without access to these proprietary emission-reduction technologies, regional manufacturers facing the EU’s expanded CBAM (Carbon Border Adjustment Mechanism) will soon find their exports priced out of western markets entirely.

HDIN Viewpoint

HDIN Research posits that the global petrochemical market has crossed the Rubicon. The era of riding macroeconomic growth for bulk chemical profitability is over. The survivors of the 2025-2026 shakeout will be those who successfully fuse "cost-plus" resource dominance with "patent-protected" green specialty premiums. Institutional investors must scrutinize the widening gap between cash flow quality and reported book profits, while aggressively discounting regional operators who lack definitive CCS roadmaps or upstream feedstock sovereignty.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com