2025 South Korean Camera Module Sector: Severe Polarization and the Imperative Automotive Pivot

Date : 2026-03-26

Reading : 120

The 2025 South Korean camera module industry has entered a definitive era of extreme polarization. A rigorous financial and operational analysis of nine leading manufacturers reveals a stark "K-shaped" trajectory. While top-tier conglomerates are leveraging deep vertical integration and scale to capture high-margin segments, mid-tier and tail-end manufacturers are battling severe cyclical headwinds. Facing global smartphone stagnation and relentless quarterly cost reduction (CR) pressures of 3% to 5% from major OEMs, these mid-tier players are aggressively reallocating capital toward Advanced Driver Assistance Systems (ADAS) and 3D sensing technologies to secure survival.

For institutional investors and supply chain strategists, the narrative is no longer about shipment volumes; it is about capital allocation efficiency, strategic moats, and the race to capture automotive tier-1 status.

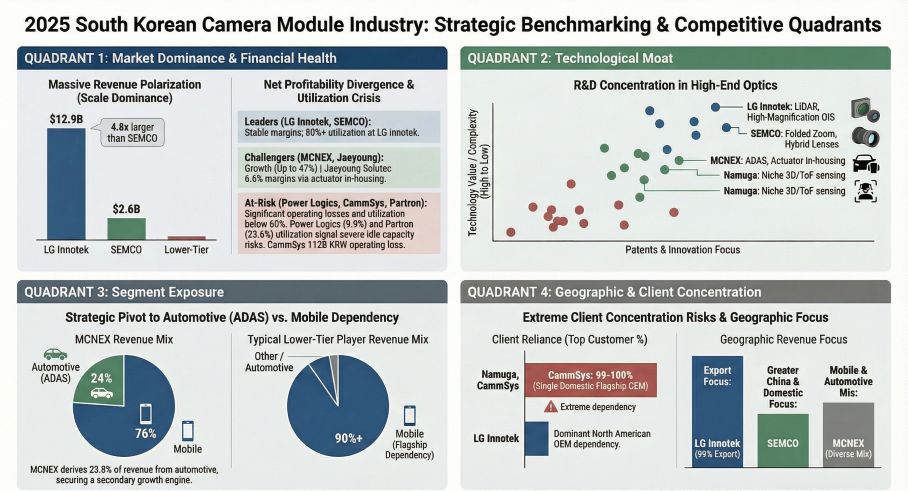

Figure 2025 South Korean Camera Module Industry: Strategic Benchmarking & Competitive Quadrants

Sector Positioning: The "Winner-Takes-All" Pyramid

Sector Positioning: The "Winner-Takes-All" Pyramid

The revenue distribution in 2025 highlights an uncompromising pyramid structure. LG Innotek maintains absolute dominance, posting over $12.88 billion in optical solution revenue—approximately 4.8 times larger than its closest competitor, Samsung Electro-Mechanics.

The "So What" factor here lies in operational efficiency. LG Innotek has successfully decoupled revenue growth from labor inflation through the implementation of unmanned, smart factories. This strategic moat has pushed their per-employee revenue past the $1 million mark, demonstrating a textbook example of economies of scale. Conversely, mid-tier players (revenue between $500M and $1B) and tail-end firms (under $500M) are trapped in a low-margin volume game, highly vulnerable to macroeconomic shocks and smartphone replacement cycle elongations.

Strategic Moats vs. Supply Chain Chokeholds

A deep dive into the 2025 annual reports reveals that pure-play module assembly is a dying business model. The new strategic moats are built on Actuator R&D and vertical integration. Companies like LG Innotek and Samsung Electro-Mechanics control the full stack—from optical lens design to high-precision OIS (Optical Image Stabilization) actuators and image processing software. Mid-tier challenger Jaeyoung Solutec achieved an impressive 47.7% YoY revenue surge precisely by internalizing OIS and Encoder actuator production, successfully penetrating flagship supply chains.

However, the industry faces severe supply chain chokeholds. The market for core sensor ICs remains a rigid duopoly dominated by Sony and Samsung Electronics. This lack of upstream bargaining power, combined with downstream customer concentration, creates a toxic squeeze. Firms overly reliant on the "S-Client" (Samsung Electronics) for lower-end A/M series smartphones are suffering severe margin compression, as they are unable to pass increased sensor costs onto the final OEM.

Strategic Pivots: Escaping Smartphone Saturation

With global smartphone shipments projected to grow at an anemic 1.5% to 2%, capital is aggressively moving toward vehicular applications. ADAS is the sector's definitive structural growth engine.

* The Automotive Transition: Mid-tier manufacturer MCNEX stands out as a successful pivot case, expanding its automotive camera revenue to nearly 23.8% of its total mix. Samsung Electro-Mechanics is pushing the technological envelope further, commercializing "Hybrid Lenses" that combine the weather resistance of glass with the moldability of plastic—a critical hardware solution for ADAS thermal distortion.

* Next-Gen Spatial Vision: Beyond vehicles, companies like Namuga are building moats in 3D depth sensing (ToF) technology, pivoting away from traditional mobile modules toward high-margin Extended Reality (XR) and robotic vision applications.

Capital Allocation Efficiency and Audit Red Flags

Our audit of the sector's 2025 capacity and cash flows uncovers critical warning signs. The industry is suffering from severe capacity mismatch. While LG Innotek maintains a healthy utilization rate of over 81%, firms heavily exposed to mid-to-low-end mobile segments are seeing their factory lines sit idle. Partron reported a high-risk utilization rate of 29.6%, and Power Logics plummeted to a critical 9.9%.

Furthermore, capital expenditure is uniformly shifting toward Vietnam (for labor cost arbitrage) and Mexico (for proximity to North American automotive OEMs). However, aggressive expansion without secure orders has led to financial strain. CammSys, despite reporting 29.5% top-line growth, recorded significant negative operating cash flows and operating losses due to a deteriorating product mix. Similarly, investors must be wary of "Big Bath" accounting tactics; Power Logics executed a massive impairment on its secondary battery unit, a red flag indicating failed diversification and potential balance sheet manipulation to lower future depreciation burdens.

HDIN Viewpoint

HDIN Research assesses that the 2025 Korean camera module sector is fundamentally bifurcated. The investment thesis must pivot from "growth at all costs" to "margin resilience." We advise stakeholders to exercise extreme caution regarding companies exhibiting negative operating cash flows, sub-60% capacity utilization, and over 80% reliance on a single mobile OEM.

The premium valuation moving into 2026 will belong to entities that demonstrate high R&D expense recognition (avoiding over-capitalization of R&D), possess in-house actuator manufacturing capabilities, and have successfully secured Tier-1 supplier status with global automotive and EV manufacturers.

---

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

For institutional investors and supply chain strategists, the narrative is no longer about shipment volumes; it is about capital allocation efficiency, strategic moats, and the race to capture automotive tier-1 status.

Figure 2025 South Korean Camera Module Industry: Strategic Benchmarking & Competitive Quadrants

Sector Positioning: The "Winner-Takes-All" PyramidThe revenue distribution in 2025 highlights an uncompromising pyramid structure. LG Innotek maintains absolute dominance, posting over $12.88 billion in optical solution revenue—approximately 4.8 times larger than its closest competitor, Samsung Electro-Mechanics.

The "So What" factor here lies in operational efficiency. LG Innotek has successfully decoupled revenue growth from labor inflation through the implementation of unmanned, smart factories. This strategic moat has pushed their per-employee revenue past the $1 million mark, demonstrating a textbook example of economies of scale. Conversely, mid-tier players (revenue between $500M and $1B) and tail-end firms (under $500M) are trapped in a low-margin volume game, highly vulnerable to macroeconomic shocks and smartphone replacement cycle elongations.

Strategic Moats vs. Supply Chain Chokeholds

A deep dive into the 2025 annual reports reveals that pure-play module assembly is a dying business model. The new strategic moats are built on Actuator R&D and vertical integration. Companies like LG Innotek and Samsung Electro-Mechanics control the full stack—from optical lens design to high-precision OIS (Optical Image Stabilization) actuators and image processing software. Mid-tier challenger Jaeyoung Solutec achieved an impressive 47.7% YoY revenue surge precisely by internalizing OIS and Encoder actuator production, successfully penetrating flagship supply chains.

However, the industry faces severe supply chain chokeholds. The market for core sensor ICs remains a rigid duopoly dominated by Sony and Samsung Electronics. This lack of upstream bargaining power, combined with downstream customer concentration, creates a toxic squeeze. Firms overly reliant on the "S-Client" (Samsung Electronics) for lower-end A/M series smartphones are suffering severe margin compression, as they are unable to pass increased sensor costs onto the final OEM.

Strategic Pivots: Escaping Smartphone Saturation

With global smartphone shipments projected to grow at an anemic 1.5% to 2%, capital is aggressively moving toward vehicular applications. ADAS is the sector's definitive structural growth engine.

* The Automotive Transition: Mid-tier manufacturer MCNEX stands out as a successful pivot case, expanding its automotive camera revenue to nearly 23.8% of its total mix. Samsung Electro-Mechanics is pushing the technological envelope further, commercializing "Hybrid Lenses" that combine the weather resistance of glass with the moldability of plastic—a critical hardware solution for ADAS thermal distortion.

* Next-Gen Spatial Vision: Beyond vehicles, companies like Namuga are building moats in 3D depth sensing (ToF) technology, pivoting away from traditional mobile modules toward high-margin Extended Reality (XR) and robotic vision applications.

Capital Allocation Efficiency and Audit Red Flags

Our audit of the sector's 2025 capacity and cash flows uncovers critical warning signs. The industry is suffering from severe capacity mismatch. While LG Innotek maintains a healthy utilization rate of over 81%, firms heavily exposed to mid-to-low-end mobile segments are seeing their factory lines sit idle. Partron reported a high-risk utilization rate of 29.6%, and Power Logics plummeted to a critical 9.9%.

Furthermore, capital expenditure is uniformly shifting toward Vietnam (for labor cost arbitrage) and Mexico (for proximity to North American automotive OEMs). However, aggressive expansion without secure orders has led to financial strain. CammSys, despite reporting 29.5% top-line growth, recorded significant negative operating cash flows and operating losses due to a deteriorating product mix. Similarly, investors must be wary of "Big Bath" accounting tactics; Power Logics executed a massive impairment on its secondary battery unit, a red flag indicating failed diversification and potential balance sheet manipulation to lower future depreciation burdens.

HDIN Viewpoint

HDIN Research assesses that the 2025 Korean camera module sector is fundamentally bifurcated. The investment thesis must pivot from "growth at all costs" to "margin resilience." We advise stakeholders to exercise extreme caution regarding companies exhibiting negative operating cash flows, sub-60% capacity utilization, and over 80% reliance on a single mobile OEM.

The premium valuation moving into 2026 will belong to entities that demonstrate high R&D expense recognition (avoiding over-capitalization of R&D), possess in-house actuator manufacturing capabilities, and have successfully secured Tier-1 supplier status with global automotive and EV manufacturers.

---

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com