MarkLines FY2025 Strategic Review: AI-Driven SaaS, ARPU Expansion, and Global Supply Chain Positioning

Date : 2026-03-29

Reading : 94

MarkLines Co., Ltd. is currently navigating a critical inflection point, transitioning from a volume-driven automotive data aggregator to a value-driven, high-margin intelligent platform. According to the latest analysis by HDIN Research, MarkLines’ FY2025 financial performance reflects the near-term friction of cyclical headwinds and aggressive global capacity expansion. However, beneath the surface of flat revenue growth lies a highly defensible SaaS business model. By executing its first contract price hike in two decades and deploying proprietary Generative AI, MarkLines is actively widening its structural moats to capture the next wave of the Electric Vehicle (EV) and Software-Defined Vehicle (SDV) intelligence market.

Figure MarkLines 2025-2026: The Intelligent Evolution of a Global Automotive Data Powerhouse

Financial Health: Cash Flow Resilience Amidst Capital Expansion

Financial Health: Cash Flow Resilience Amidst Capital Expansion

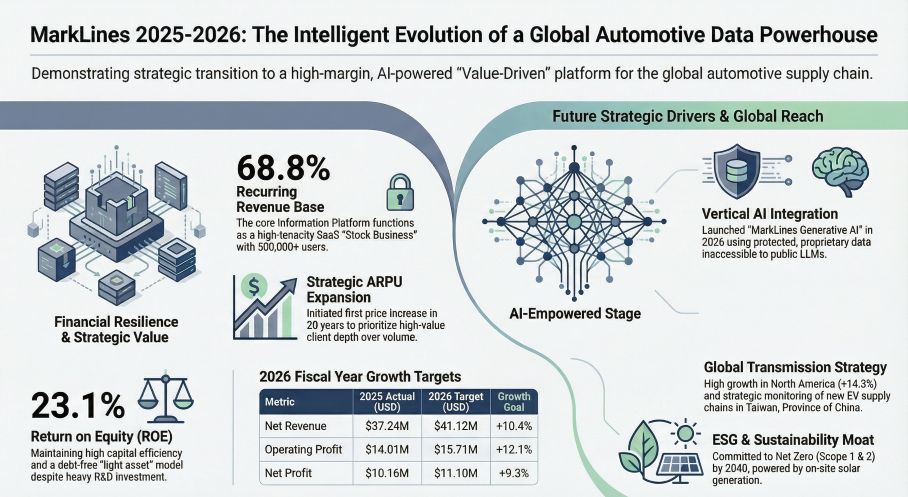

In FY2025, MarkLines reported flat revenue of $37.24 million (+0.1% YoY) and a 5.4% contraction in operating profit to $14.01 million. Rather than a structural deficit, this margin compression is the direct result of strategic fixed-cost investments required to build physical and regional moats—specifically, the establishment of the Shenzhen subsidiary, the Fukuoka call center, and the Atsugi Benchmark (Teardown) Center.

Despite these capital expenditures, MarkLines' financial health remains exceptional, defined by a distinct "asset-light premium." The core Information Platform continues to be a cash cow, contributing 68.8% of total revenue via recurring subscriptions. The company boasts an impressive Operating Cash Flow to Net Income ratio of 1.19x, indicating highly liquid earnings supported by a robust unearned revenue (prepaid contract) model. Furthermore, capital allocation efficiency remains a priority for the board; MarkLines maintained a rigorous 44.6% dividend payout ratio and executed significant share buybacks, sustaining a high Return on Equity (ROE) of 23.1%—well above the Japanese market average.

Strategic Pivots: Monetizing the Moat via Pricing and AI

MarkLines is decisively pivoting its operational KPIs from "total subscriber volume" to "Average Revenue Per User (ARPU) expansion."

Faced with budget contractions among legacy OEM suppliers, the platform experienced a slight 2.5% net churn, ending the year with 5,476 corporate subscribers. Management has strategically accepted the loss of lower-tier accounts to implement the company's first systematic price adjustment in 20 years.

To justify this premium, MarkLines launched its "Generative AI β version" in January 2026. Unlike generic Large Language Models (LLMs) that scrape public data, MarkLines’ AI is structurally walled. It functions as an enterprise solution by exclusively querying the company's proprietary, copyrighted database—spanning 20 years of supply chain mapping, factory capacity metrics, and exclusive engineering teardown data. This transition from "data extraction" to "decision-making solutions" fundamentally deepens SaaS stickiness and creates high switching costs for automotive R&D departments.

Industry Outlook & Sector Positioning: The Physical-Digital Convergence

As Chinese EV manufacturers like BYD rapidly reshape the global automotive landscape, MarkLines has aligned its geopolitical and sector positioning to capture alpha.

The establishment of the Shenzhen subsidiary serves as a critical forward-operating base to monitor the hyper-active Chinese Intelligent Connected Vehicle (ICV) supply chain. Simultaneously, the Bangkok office anchors its intelligence gathering in the ASEAN "Detroit of Asia."

More importantly, MarkLines has successfully differentiated itself from macroeconomic data giants (e.g., S&P Global Mobility) by integrating offline reverse-engineering with online data distribution. Through its Atsugi Benchmark Center, MarkLines physically tears down core EV components (such as e-Axles and battery packs) and digitizes the cost-analysis data. This closed-loop "physical-to-digital" capability is an insurmountable barrier to entry for pure-software competitors.

HDIN Viewpoint: A Defensive Growth Asset Approaching the J-Curve

From the perspective of HDIN Research, MarkLines exemplifies a classic "Defensive Growth" asset currently undergoing a strategic J-curve transformation. While the initial capital expenditures and macro-driven budget cuts from traditional automakers have temporarily muted operating profit, the company’s underlying competitive architecture is stronger than ever.

The true test for MarkLines will arrive in FY2026. We advise market observers to closely monitor the elasticity of demand following the comprehensive price hikes and the upselling efficiency of its proprietary AI platform. If MarkLines can successfully translate its exclusive teardown data and localized intelligence from Shenzhen and North America into high-tier enterprise subscriptions, the company is primed to unlock significant margin expansion and redefine the valuation multiples of automotive B2B intelligence.

Presentation Download & Media Access

* Click the PDF download link under “Related Topics” to access the presentation of this report.

* Click this link to watch the YouTube video.

About HDIN Research

Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure MarkLines 2025-2026: The Intelligent Evolution of a Global Automotive Data Powerhouse

Financial Health: Cash Flow Resilience Amidst Capital ExpansionIn FY2025, MarkLines reported flat revenue of $37.24 million (+0.1% YoY) and a 5.4% contraction in operating profit to $14.01 million. Rather than a structural deficit, this margin compression is the direct result of strategic fixed-cost investments required to build physical and regional moats—specifically, the establishment of the Shenzhen subsidiary, the Fukuoka call center, and the Atsugi Benchmark (Teardown) Center.

Despite these capital expenditures, MarkLines' financial health remains exceptional, defined by a distinct "asset-light premium." The core Information Platform continues to be a cash cow, contributing 68.8% of total revenue via recurring subscriptions. The company boasts an impressive Operating Cash Flow to Net Income ratio of 1.19x, indicating highly liquid earnings supported by a robust unearned revenue (prepaid contract) model. Furthermore, capital allocation efficiency remains a priority for the board; MarkLines maintained a rigorous 44.6% dividend payout ratio and executed significant share buybacks, sustaining a high Return on Equity (ROE) of 23.1%—well above the Japanese market average.

Strategic Pivots: Monetizing the Moat via Pricing and AI

MarkLines is decisively pivoting its operational KPIs from "total subscriber volume" to "Average Revenue Per User (ARPU) expansion."

Faced with budget contractions among legacy OEM suppliers, the platform experienced a slight 2.5% net churn, ending the year with 5,476 corporate subscribers. Management has strategically accepted the loss of lower-tier accounts to implement the company's first systematic price adjustment in 20 years.

To justify this premium, MarkLines launched its "Generative AI β version" in January 2026. Unlike generic Large Language Models (LLMs) that scrape public data, MarkLines’ AI is structurally walled. It functions as an enterprise solution by exclusively querying the company's proprietary, copyrighted database—spanning 20 years of supply chain mapping, factory capacity metrics, and exclusive engineering teardown data. This transition from "data extraction" to "decision-making solutions" fundamentally deepens SaaS stickiness and creates high switching costs for automotive R&D departments.

Industry Outlook & Sector Positioning: The Physical-Digital Convergence

As Chinese EV manufacturers like BYD rapidly reshape the global automotive landscape, MarkLines has aligned its geopolitical and sector positioning to capture alpha.

The establishment of the Shenzhen subsidiary serves as a critical forward-operating base to monitor the hyper-active Chinese Intelligent Connected Vehicle (ICV) supply chain. Simultaneously, the Bangkok office anchors its intelligence gathering in the ASEAN "Detroit of Asia."

More importantly, MarkLines has successfully differentiated itself from macroeconomic data giants (e.g., S&P Global Mobility) by integrating offline reverse-engineering with online data distribution. Through its Atsugi Benchmark Center, MarkLines physically tears down core EV components (such as e-Axles and battery packs) and digitizes the cost-analysis data. This closed-loop "physical-to-digital" capability is an insurmountable barrier to entry for pure-software competitors.

HDIN Viewpoint: A Defensive Growth Asset Approaching the J-Curve

From the perspective of HDIN Research, MarkLines exemplifies a classic "Defensive Growth" asset currently undergoing a strategic J-curve transformation. While the initial capital expenditures and macro-driven budget cuts from traditional automakers have temporarily muted operating profit, the company’s underlying competitive architecture is stronger than ever.

The true test for MarkLines will arrive in FY2026. We advise market observers to closely monitor the elasticity of demand following the comprehensive price hikes and the upselling efficiency of its proprietary AI platform. If MarkLines can successfully translate its exclusive teardown data and localized intelligence from Shenzhen and North America into high-tier enterprise subscriptions, the company is primed to unlock significant margin expansion and redefine the valuation multiples of automotive B2B intelligence.

Presentation Download & Media Access

* Click the PDF download link under “Related Topics” to access the presentation of this report.

* Click this link to watch the YouTube video.

About HDIN Research

Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com