ToolGen 2025 Financial Analysis: Navigating the Chasm Between CRISPR Patent Premiums and Liquidity Realities

Date : 2026-03-28

Reading : 56

Behind the veil of a 46.6% year-over-year revenue surge, ToolGen’s 2025 annual report reveals a biotechnology firm caught in a profound dichotomy: holding world-class intellectual property (IP) while battling a ticking 18-month liquidity clock. Generating approximately $919,100 in total revenue against an operating loss of $16.39 million, ToolGen is in a classic early-stage commercialization phase characterized by high gross margins, micro-revenue scale, and extreme R&D capital expenditure.

Based on HDIN Research’s in-depth teardown of the company's fiscal fundamentals and sector positioning, we analyze the strategic implications behind ToolGen’s current valuation and future viability.

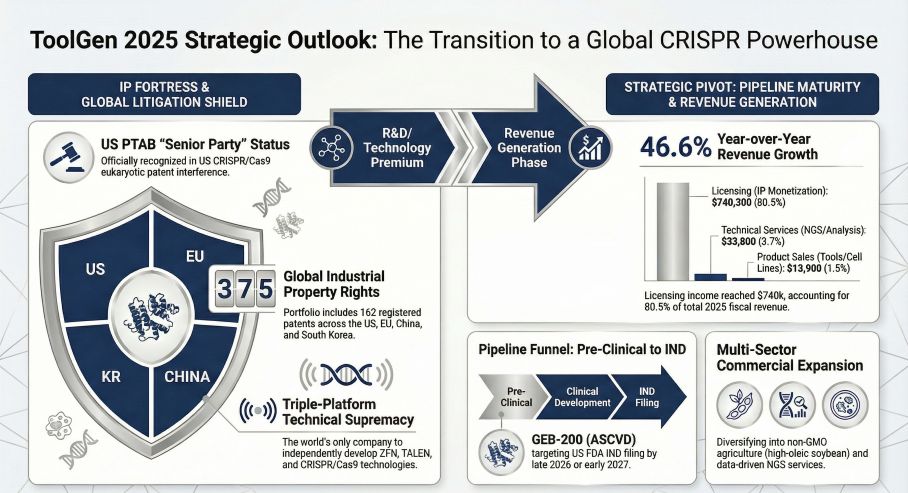

Figure ToolGen 2025 Strategic Outlook: The Transition to a Global CRISPR Powerhouse

Strategic Moats: The CRISPR Patent Premium

Strategic Moats: The CRISPR Patent Premium

ToolGen’s primary valuation driver is not its current cash flow, but its immense technology premium. The company remains the only entity globally to have independently developed all three generations of gene scissors (ZFN, TALEN, and CRISPR/Cas9).

In 2025, patent monetization (Licensing) drove 80.5% of total revenue, exhibiting a highly leveraged business model with an 87.25% gross margin. ToolGen’s strategic moat is fortified by its "Senior Party" status in the U.S. Patent Trial and Appeal Board (PTAB) interference proceedings against the CVC group and the Broad Institute. This legal positioning grants the company a formidable advantage in dictating global licensing fees. Furthermore, its proprietary Sniper Cas9 2.0 technology resolves the persistent industry trade-off between high specificity and high activity, reinforcing its competitive superiority over traditional Base Editor and Cpf1 (Cas12a) platforms.

Capital Allocation Efficiency & Financial Health

Despite strong IP, ToolGen's capital allocation efficiency reflects severe commercialization bottlenecks. The company’s R&D-to-revenue ratio remains at an extreme 580%, entirely sustained by external financing rather than organic cash flow.

HDIN Research's audit of the income statement reveals that the reported net loss was heavily distorted by non-cash items. An embedded derivative liability loss of $1.1 million artificially inflated the deficit, while a $2.8 million asset revaluation gain (on properties in South Korea and its trademark registrations in regions including China's Taiwan) was utilized to lower the debt-to-equity ratio to 10.4%. Stripping away these accounting maneuvers, the company's core operational burn rate stands at roughly $14.22 million annually. With current core liquid reserves of $21.24 million, ToolGen’s survival runway is projected at just 1.5 years, signaling a critical need for external capital injections or milestone payments by mid-2027.

Sector Positioning & Commercialization Bottlenecks

Geographically, ToolGen has successfully penetrated high-value markets, with North America accounting for 44.9% of revenues, followed by Asia (including China and its Taiwan region) at 21.5%. However, structural vulnerabilities persist in its revenue architecture. The company suffers from extreme customer concentration, with its top three clients contributing nearly 48% of total revenue—a single contract disruption could trigger a precipitous top-line collapse.

To counter cyclical headwinds in the biopharma sector, ToolGen is executing strategic pivots into synthetic biology and agriculture. By securing a Non-GMO regulatory exemption from the USDA for its gene-edited crops, the company has bypassed lengthy GMO approval processes, establishing a regulatory arbitrage advantage against traditional seed conglomerates. Concurrently, its therapeutic pipeline—anchored by TGT-001 for CMT1A—is aggressively targeting an FDA IND submission between 2026 and 2027, a milestone that serves as the ultimate litmus test for the company's valuation.

HDIN Viewpoint

From an institutional perspective, HDIN Research views ToolGen as a "high-risk, high-reward" technology option. The company’s intrinsic value is heavily skewed toward its CRISPR IP options rather than fundamental earnings growth. The glaring misalignment between management’s strategic forecasting (missing 2024 revenue targets by over 90%) and execution capabilities indicates a painful governance restructuring phase.

Moving forward, the market must closely monitor two catalysts: the resolution timeline of the U.S. patent litigation, which threatens substantial legal liabilities, and the company's ability to secure large-scale upfront milestone payments before its liquidity window closes in early 2027. ToolGen’s ultimate success will depend on bridging the gap between its scientific brilliance and sustainable commercial monetization.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

About HDIN Research Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Based on HDIN Research’s in-depth teardown of the company's fiscal fundamentals and sector positioning, we analyze the strategic implications behind ToolGen’s current valuation and future viability.

Figure ToolGen 2025 Strategic Outlook: The Transition to a Global CRISPR Powerhouse

Strategic Moats: The CRISPR Patent PremiumToolGen’s primary valuation driver is not its current cash flow, but its immense technology premium. The company remains the only entity globally to have independently developed all three generations of gene scissors (ZFN, TALEN, and CRISPR/Cas9).

In 2025, patent monetization (Licensing) drove 80.5% of total revenue, exhibiting a highly leveraged business model with an 87.25% gross margin. ToolGen’s strategic moat is fortified by its "Senior Party" status in the U.S. Patent Trial and Appeal Board (PTAB) interference proceedings against the CVC group and the Broad Institute. This legal positioning grants the company a formidable advantage in dictating global licensing fees. Furthermore, its proprietary Sniper Cas9 2.0 technology resolves the persistent industry trade-off between high specificity and high activity, reinforcing its competitive superiority over traditional Base Editor and Cpf1 (Cas12a) platforms.

Capital Allocation Efficiency & Financial Health

Despite strong IP, ToolGen's capital allocation efficiency reflects severe commercialization bottlenecks. The company’s R&D-to-revenue ratio remains at an extreme 580%, entirely sustained by external financing rather than organic cash flow.

HDIN Research's audit of the income statement reveals that the reported net loss was heavily distorted by non-cash items. An embedded derivative liability loss of $1.1 million artificially inflated the deficit, while a $2.8 million asset revaluation gain (on properties in South Korea and its trademark registrations in regions including China's Taiwan) was utilized to lower the debt-to-equity ratio to 10.4%. Stripping away these accounting maneuvers, the company's core operational burn rate stands at roughly $14.22 million annually. With current core liquid reserves of $21.24 million, ToolGen’s survival runway is projected at just 1.5 years, signaling a critical need for external capital injections or milestone payments by mid-2027.

Sector Positioning & Commercialization Bottlenecks

Geographically, ToolGen has successfully penetrated high-value markets, with North America accounting for 44.9% of revenues, followed by Asia (including China and its Taiwan region) at 21.5%. However, structural vulnerabilities persist in its revenue architecture. The company suffers from extreme customer concentration, with its top three clients contributing nearly 48% of total revenue—a single contract disruption could trigger a precipitous top-line collapse.

To counter cyclical headwinds in the biopharma sector, ToolGen is executing strategic pivots into synthetic biology and agriculture. By securing a Non-GMO regulatory exemption from the USDA for its gene-edited crops, the company has bypassed lengthy GMO approval processes, establishing a regulatory arbitrage advantage against traditional seed conglomerates. Concurrently, its therapeutic pipeline—anchored by TGT-001 for CMT1A—is aggressively targeting an FDA IND submission between 2026 and 2027, a milestone that serves as the ultimate litmus test for the company's valuation.

HDIN Viewpoint

From an institutional perspective, HDIN Research views ToolGen as a "high-risk, high-reward" technology option. The company’s intrinsic value is heavily skewed toward its CRISPR IP options rather than fundamental earnings growth. The glaring misalignment between management’s strategic forecasting (missing 2024 revenue targets by over 90%) and execution capabilities indicates a painful governance restructuring phase.

Moving forward, the market must closely monitor two catalysts: the resolution timeline of the U.S. patent litigation, which threatens substantial legal liabilities, and the company's ability to secure large-scale upfront milestone payments before its liquidity window closes in early 2027. ToolGen’s ultimate success will depend on bridging the gap between its scientific brilliance and sustainable commercial monetization.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

About HDIN Research Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com