Tokyo Ohka Kogyo (TOK) 2025: Expanding Strategic Moats Through EUV Dominance and Localized Supply Chains

Date : 2026-03-26

Reading : 202

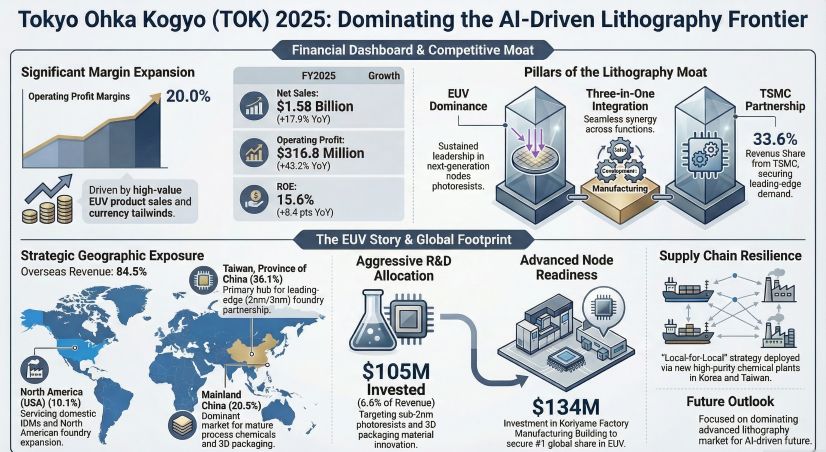

Tokyo Ohka Kogyo (TOK) has systematically transitioned from a traditional chemical supplier to a critical bottleneck controller in the generative AI hardware ecosystem. Driven by aggressive capital allocation in next-generation extreme ultraviolet (EUV) photoresists and deepening foundry integration, TOK achieved a Gross Profit Margin (GPM) of 37.7% and an Operating Profit Margin (OPM) of 20.0% in FY2025. However, beneath this margin expansion lies a complex web of high customer concentration, geopolitical hedging, and impending depreciation cycles that demand stringent investor scrutiny.

Figure Tokyo Ohka Kogyo (TOK) 2025: Dominating the Al-Driven Lithography Frontier

Strategic Synergy and Foundry Concentration

Strategic Synergy and Foundry Concentration

Rather than merely reacting to market demand, TOK is actively co-developing the future of semiconductor architectures with top-tier foundries. In FY2025, revenue exposure to its largest client, Taiwan Semiconductor Manufacturing Company (TSMC), expanded from 30.4% to 33.6% (approximately $532 million).

*The "So What" Factor:* This hyper-concentration is not a vulnerability, but a formidable strategic moat. By deploying "Sales Engineers" directly to client fabrication facilities, TOK has achieved a three-pronged integration (development, manufacturing, and sales). This structural lock-in ensures TOK's proprietary chemical formulations are fundamentally embedded into the early-stage validation of TSMC's 2nm and sub-2nm nodes, effectively shutting out secondary competitors.

Navigating Geopolitical Headwinds via "Local-for-Local" Strategy

With 84.5% of its revenue generated overseas, TOK is acutely exposed to macroeconomic trade friction. To mitigate geopolitical headwinds and logistical disruptions, the company has accelerated its "Local-for-Local" capital deployment.

* South Korea (Pyeongtaek): An $80.23 million investment in a new high-purity chemical facility aims to capture the high-bandwidth memory (HBM) and 3D NAND boom directly at the source, serving giants like Samsung and SK Hynix with minimal latency.

* Taiwan (Miaoli): Expanding localized R&D and manufacturing safeguards advanced node photoresist delivery against potential Taiwan Strait volatility, satisfying government-level demands for semiconductor supply chain sovereignty.

Furthermore, to hedge against upstream rare-chemical shortages, TOK proactively leveraged its balance sheet, increasing raw material inventory by 23.8% to $122 million. This shift from "just-in-time" to "just-in-case" procurement safeguards production continuity against external macroeconomic shocks.

Technological Moats: High-NA, 3D Integration, and GaaFET Preparedness

TOK directed $105 million toward R&D in FY2025, precisely anchoring its patent portfolio to the limits of process miniaturization.

*The "So What" Factor:* The company's $134 million expansion of the Koriyama Factory is a calculated move to dominate the upcoming High-NA EUV transition. Beyond traditional lithography, TOK is heavily investing in high-aspect-ratio etching materials for 3D NAND/DRAM and advanced packaging (TSV) materials. HDIN Research’s analysis of TOK’s forward-looking patents indicates aggressive preparation for Gate-All-Around (GaaFET) and Backside Power Delivery (BSPDN) architectures. By controlling the purity and edge-roughness parameters critical to these next-gen processes, TOK commands immense pricing power.

Capital Allocation Efficiency and Profitability Attribution

TOK’s FY2025 margin expansion was catalyzed by a potent convergence of product mix optimization, operating leverage, and currency tailwinds. The surge in high-value EUV photoresist sales provided the pricing power necessary to absorb raw material volatility. Concurrently, a 16.4% year-over-year increase in material business output successfully diluted fixed costs, generating positive operating leverage despite a $3.17 million increase in total depreciation expenses.

HDIN Viewpoint: Cyclical Headwinds and Financial Scrutiny

While TOK's market positioning is undeniable, HDIN Research advises institutional investors to monitor two critical risk vectors. First, the reported net profit includes a $9.51 million one-off contingent consideration gain, which flatters the bottom line but does not reflect core operational sustainability.

Second, the $134 million Koriyama facility expansion will trigger a massive depreciation cycle upon completion in 2026. If the current AI-driven capital expenditure cycle among top foundries cools, TOK will face severe downward pressure on its Fixed Asset Turnover ratio. The company's current profitability relies heavily on the synchronized expansion of its singular largest client. As such, TOK's long-term valuation will be dictated not just by its chemical engineering prowess, but by its ability to maintain capacity utilization amid volatile global semiconductor cycles.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research Profile:

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure Tokyo Ohka Kogyo (TOK) 2025: Dominating the Al-Driven Lithography Frontier

Strategic Synergy and Foundry ConcentrationRather than merely reacting to market demand, TOK is actively co-developing the future of semiconductor architectures with top-tier foundries. In FY2025, revenue exposure to its largest client, Taiwan Semiconductor Manufacturing Company (TSMC), expanded from 30.4% to 33.6% (approximately $532 million).

*The "So What" Factor:* This hyper-concentration is not a vulnerability, but a formidable strategic moat. By deploying "Sales Engineers" directly to client fabrication facilities, TOK has achieved a three-pronged integration (development, manufacturing, and sales). This structural lock-in ensures TOK's proprietary chemical formulations are fundamentally embedded into the early-stage validation of TSMC's 2nm and sub-2nm nodes, effectively shutting out secondary competitors.

Navigating Geopolitical Headwinds via "Local-for-Local" Strategy

With 84.5% of its revenue generated overseas, TOK is acutely exposed to macroeconomic trade friction. To mitigate geopolitical headwinds and logistical disruptions, the company has accelerated its "Local-for-Local" capital deployment.

* South Korea (Pyeongtaek): An $80.23 million investment in a new high-purity chemical facility aims to capture the high-bandwidth memory (HBM) and 3D NAND boom directly at the source, serving giants like Samsung and SK Hynix with minimal latency.

* Taiwan (Miaoli): Expanding localized R&D and manufacturing safeguards advanced node photoresist delivery against potential Taiwan Strait volatility, satisfying government-level demands for semiconductor supply chain sovereignty.

Furthermore, to hedge against upstream rare-chemical shortages, TOK proactively leveraged its balance sheet, increasing raw material inventory by 23.8% to $122 million. This shift from "just-in-time" to "just-in-case" procurement safeguards production continuity against external macroeconomic shocks.

Technological Moats: High-NA, 3D Integration, and GaaFET Preparedness

TOK directed $105 million toward R&D in FY2025, precisely anchoring its patent portfolio to the limits of process miniaturization.

*The "So What" Factor:* The company's $134 million expansion of the Koriyama Factory is a calculated move to dominate the upcoming High-NA EUV transition. Beyond traditional lithography, TOK is heavily investing in high-aspect-ratio etching materials for 3D NAND/DRAM and advanced packaging (TSV) materials. HDIN Research’s analysis of TOK’s forward-looking patents indicates aggressive preparation for Gate-All-Around (GaaFET) and Backside Power Delivery (BSPDN) architectures. By controlling the purity and edge-roughness parameters critical to these next-gen processes, TOK commands immense pricing power.

Capital Allocation Efficiency and Profitability Attribution

TOK’s FY2025 margin expansion was catalyzed by a potent convergence of product mix optimization, operating leverage, and currency tailwinds. The surge in high-value EUV photoresist sales provided the pricing power necessary to absorb raw material volatility. Concurrently, a 16.4% year-over-year increase in material business output successfully diluted fixed costs, generating positive operating leverage despite a $3.17 million increase in total depreciation expenses.

HDIN Viewpoint: Cyclical Headwinds and Financial Scrutiny

While TOK's market positioning is undeniable, HDIN Research advises institutional investors to monitor two critical risk vectors. First, the reported net profit includes a $9.51 million one-off contingent consideration gain, which flatters the bottom line but does not reflect core operational sustainability.

Second, the $134 million Koriyama facility expansion will trigger a massive depreciation cycle upon completion in 2026. If the current AI-driven capital expenditure cycle among top foundries cools, TOK will face severe downward pressure on its Fixed Asset Turnover ratio. The company's current profitability relies heavily on the synchronized expansion of its singular largest client. As such, TOK's long-term valuation will be dictated not just by its chemical engineering prowess, but by its ability to maintain capacity utilization amid volatile global semiconductor cycles.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research Profile:

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com