2025 Global Tire Industry: Navigating Cyclical Headwinds Through Strategic Moats and Capacity Optimization

Date : 2026-03-26

Reading : 608

The global tire industry in 2025 is defined by a critical inflection point: stagnant volumes and volatile input costs are being counterbalanced by aggressive pricing strategies and structural shifts in manufacturing. According to the latest proprietary analysis by HDIN Research, tier-one manufacturers are actively decoupling from the cyclical headwinds of the Original Equipment (OE) market by doubling down on the Replacement (RT) market and high-value product segments. Simultaneously, a massive reallocation of capital is underway, with production capacities rapidly migrating from high-cost Western geographies to high-density clusters in the Asia-Pacific (APAC) region, fundamentally reshaping the sector's operational efficiency.

Figure 2025 Global Tire Strategic Map: High-Value Resilience & Tech Transformation

Sector Positioning: The OE Headwind and High-Value Defense

Sector Positioning: The OE Headwind and High-Value Defense

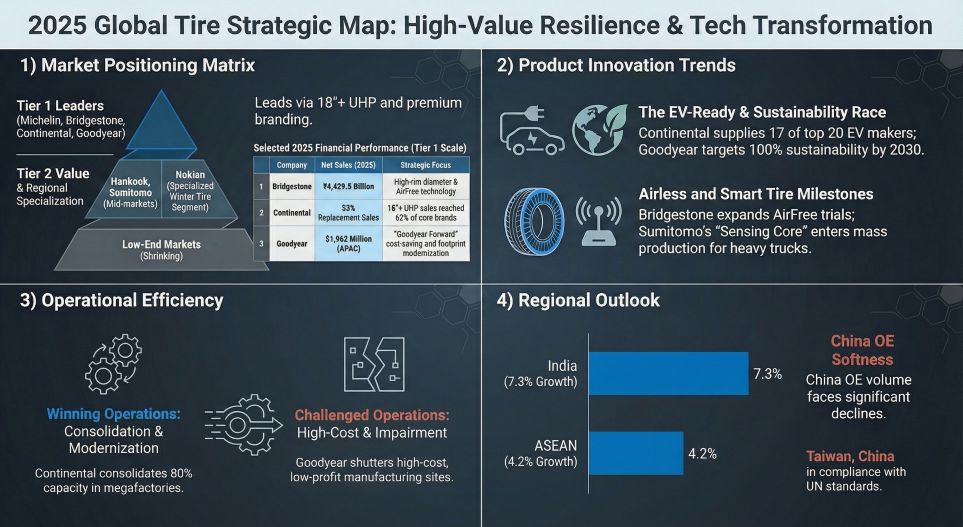

In 2025, the Original Equipment (OE) market became a significant drag on profitability, heavily impacted by geopolitical tensions, EV subsidy phase-outs, and automotive production plateaus. HDIN Research notes that top-tier OEMs exerted intense pricing pressure, forcing tire manufacturers to leverage the Replacement (RT) market as their primary margin stabilizer.

To defend against volume contraction, industry leaders successfully deployed sophisticated "price-mix" strategies. Rather than engaging in bottom-line price wars, manufacturers optimized their product mixes toward high-rim-diameter (18-inch and above) and EV-specific tires. Continental serves as a prime example of this strategic pivot; by aggressively executing its premiumization strategy, UHP (Ultra-High Performance) tires now account for a staggering 62% of its core brand volume. Similarly, Michelin offset a 2.28 million euro raw material headwind with an impressive 7.45 million euro gain generated entirely through premium price-mix optimization, proving that brand equity remains an impenetrable strategic moat during economic downcycles.

Capital Allocation Efficiency: The APAC Migration

Capital allocation in 2025 is characterized by a "trim the fat" philosophy. To lower break-even points, manufacturers are ruthlessly purging high-cost legacy capacities. Goodyear and Sumitomo have executed aggressive plant closures across Germany, South Africa, and the United States, shifting their capital expenditures toward low-cost, highly automated facilities in China (including Taiwan), Vietnam, and Thailand.

This geographic pivot is not merely about cheap labor; it is about next-generation operational efficiency. Nokian Tyres has set a new benchmark for human capital efficiency, generating an industry-leading $392,200 in revenue per employee, driven by its zero-emission, highly automated Romanian facility. Meanwhile, Asian-based manufacturers like Hankook and Kumho have deepened their supply chain moats by leveraging high-density manufacturing clusters in China, utilizing "local-to-local" supply networks to mitigate global freight volatility and tariff risks.

Financial Health & Accounting Prudence

While top-line growth remains muted, margin dispersion among the top 10 global players has widened significantly. Hankook leads the pack with an exceptional EBITDA margin of 21.4%, showcasing immense profitability elasticity. Conversely, Michelin demonstrated superior earnings quality, boasting a free cash flow-to-net income ratio of 1.31, underscoring its ability to generate robust cash liquidity even amid volume declines.

However, HDIN Research advises institutional investors to scrutinize the underlying accounting prudence of these financial health indicators:

* Impairment Risks: Goodyear reported a staggering $1.72 billion net loss in 2025, driven primarily by $714 million in goodwill impairments and deferred tax asset valuation allowances. This underscores the severe financial friction associated with delayed restructuring.

* Earnings Transparency: The complexity of related-party transactions requires careful auditing. Kumho relies heavily on intra-group transactions with its major shareholder, DoubleStar, raising flags regarding transfer pricing and the true nature of its operating margins. Furthermore, Hankook's capitalization of R&D expenses artificially shores up short-term operating profits compared to European peers who expense these costs immediately.

R&D Moats: Software-Defined Tires and Sustainability

The competitive battleground has officially shifted from chemical rubber formulations to "software-defined tires" and sustainable engineering. The impending Euro 7 emissions standards—which heavily regulate Tire and Road Wear Particles (TRWP)—have created a steep technological barrier to entry.

Michelin dominates this space with an unmatched R&D budget of approximately $1.35 billion (nearly six times that of its tier-two Asian competitors), granting it a formidable lead in abrasion performance and sustainable material integration. Concurrently, the digitization of tires is unlocking new B2B revenue streams. Sumitomo’s "Sensing Core" technology, which analyzes wheel-speed signals to detect tire pressure and load without physical sensors, represents a paradigm shift in fleet management and OEM integration.

HDIN Viewpoint

The 2025 fiscal data confirms our thesis: the global tire industry is bifurcating. The premium tier is insulating itself through a "Green Premium" (sustainable materials) and deep sensor-software integration, while mid-tier players are relying on raw manufacturing scale in APAC to survive. Looking ahead to 2026, HDIN Research believes that a manufacturer’s valuation multiple will be dictated by three factors: their agility in exiting European legacy manufacturing, their market share in the EV/18-inch+ segment, and their balance sheet transparency. Investors must remain hyper-vigilant regarding non-cash impairments and the actual execution speed of corporate restructuring programs.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure 2025 Global Tire Strategic Map: High-Value Resilience & Tech Transformation

Sector Positioning: The OE Headwind and High-Value DefenseIn 2025, the Original Equipment (OE) market became a significant drag on profitability, heavily impacted by geopolitical tensions, EV subsidy phase-outs, and automotive production plateaus. HDIN Research notes that top-tier OEMs exerted intense pricing pressure, forcing tire manufacturers to leverage the Replacement (RT) market as their primary margin stabilizer.

To defend against volume contraction, industry leaders successfully deployed sophisticated "price-mix" strategies. Rather than engaging in bottom-line price wars, manufacturers optimized their product mixes toward high-rim-diameter (18-inch and above) and EV-specific tires. Continental serves as a prime example of this strategic pivot; by aggressively executing its premiumization strategy, UHP (Ultra-High Performance) tires now account for a staggering 62% of its core brand volume. Similarly, Michelin offset a 2.28 million euro raw material headwind with an impressive 7.45 million euro gain generated entirely through premium price-mix optimization, proving that brand equity remains an impenetrable strategic moat during economic downcycles.

Capital Allocation Efficiency: The APAC Migration

Capital allocation in 2025 is characterized by a "trim the fat" philosophy. To lower break-even points, manufacturers are ruthlessly purging high-cost legacy capacities. Goodyear and Sumitomo have executed aggressive plant closures across Germany, South Africa, and the United States, shifting their capital expenditures toward low-cost, highly automated facilities in China (including Taiwan), Vietnam, and Thailand.

This geographic pivot is not merely about cheap labor; it is about next-generation operational efficiency. Nokian Tyres has set a new benchmark for human capital efficiency, generating an industry-leading $392,200 in revenue per employee, driven by its zero-emission, highly automated Romanian facility. Meanwhile, Asian-based manufacturers like Hankook and Kumho have deepened their supply chain moats by leveraging high-density manufacturing clusters in China, utilizing "local-to-local" supply networks to mitigate global freight volatility and tariff risks.

Financial Health & Accounting Prudence

While top-line growth remains muted, margin dispersion among the top 10 global players has widened significantly. Hankook leads the pack with an exceptional EBITDA margin of 21.4%, showcasing immense profitability elasticity. Conversely, Michelin demonstrated superior earnings quality, boasting a free cash flow-to-net income ratio of 1.31, underscoring its ability to generate robust cash liquidity even amid volume declines.

However, HDIN Research advises institutional investors to scrutinize the underlying accounting prudence of these financial health indicators:

* Impairment Risks: Goodyear reported a staggering $1.72 billion net loss in 2025, driven primarily by $714 million in goodwill impairments and deferred tax asset valuation allowances. This underscores the severe financial friction associated with delayed restructuring.

* Earnings Transparency: The complexity of related-party transactions requires careful auditing. Kumho relies heavily on intra-group transactions with its major shareholder, DoubleStar, raising flags regarding transfer pricing and the true nature of its operating margins. Furthermore, Hankook's capitalization of R&D expenses artificially shores up short-term operating profits compared to European peers who expense these costs immediately.

R&D Moats: Software-Defined Tires and Sustainability

The competitive battleground has officially shifted from chemical rubber formulations to "software-defined tires" and sustainable engineering. The impending Euro 7 emissions standards—which heavily regulate Tire and Road Wear Particles (TRWP)—have created a steep technological barrier to entry.

Michelin dominates this space with an unmatched R&D budget of approximately $1.35 billion (nearly six times that of its tier-two Asian competitors), granting it a formidable lead in abrasion performance and sustainable material integration. Concurrently, the digitization of tires is unlocking new B2B revenue streams. Sumitomo’s "Sensing Core" technology, which analyzes wheel-speed signals to detect tire pressure and load without physical sensors, represents a paradigm shift in fleet management and OEM integration.

HDIN Viewpoint

The 2025 fiscal data confirms our thesis: the global tire industry is bifurcating. The premium tier is insulating itself through a "Green Premium" (sustainable materials) and deep sensor-software integration, while mid-tier players are relying on raw manufacturing scale in APAC to survive. Looking ahead to 2026, HDIN Research believes that a manufacturer’s valuation multiple will be dictated by three factors: their agility in exiting European legacy manufacturing, their market share in the EV/18-inch+ segment, and their balance sheet transparency. Investors must remain hyper-vigilant regarding non-cash impairments and the actual execution speed of corporate restructuring programs.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com