Home Depot vs. Lowe’s FY2025: From DIY Tailwinds to

Date : 2026-03-29

Reading : 128

The home improvement retail sector is navigating a profound structural transition. Stifled by an extended high-interest-rate environment and record-low housing turnover, the era of macro-driven, DIY explosive growth has concluded. According to HDIN Research’s comprehensive FY2025 analysis, both The Home Depot (HD) and Lowe’s (LOW) are executing aggressive strategic pivots. By substituting share buybacks with massive heavy-asset acquisitions, the two retail titans are shifting their battleground from consumer retail to complex, Professional (Pro) contractor ecosystems.

Figure 2025 HOME IMPROVEMENT TITANS: HOME DEPOT VS LOWE'S STRATEGIC & FINANCIALCOMPARISON

Financial Health & Capital Allocation Efficiency

Financial Health & Capital Allocation Efficiency

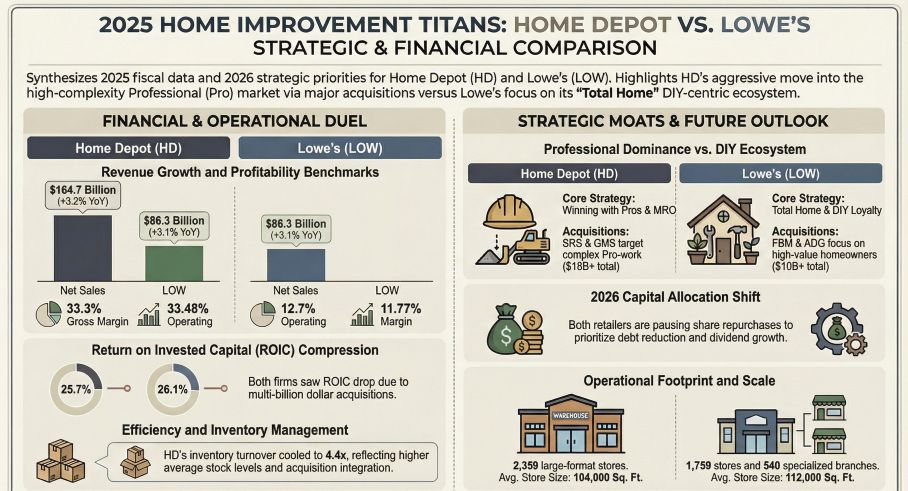

While both companies maintain remarkably similar gross margins (~33.4%), Home Depot possesses an overwhelming advantage in scale and asset utilization. Generating $164.6 billion in total revenue compared to Lowe's $86.2 billion, HD's operational efficiency is best illustrated by its sales per square foot: $673 versus LOW’s $440.

A critical "So What" emerges in their FY2025 capital allocation strategies. Both giants have effectively paused or drastically slashed their historical stock repurchase programs to fund debt repayments and integrations of multi-billion-dollar acquisitions. This "defensive contraction" in buybacks reflects a prudent management pivot: prioritizing balance sheet stability and dividend safety in a high-cost capital environment over short-term EPS artificial inflation.

Strategic Pivots: The Race for the "Pro" Segment

The most defining collective movement of FY2025 is the heavy-asset leap into the Pro segment, driven by the need to establish a "second growth curve" amidst a stagnant DIY market.

* Home Depot's Scale Moat: HD solidified its dominance through the acquisitions of SRS Distribution and GMS (totaling over $23 billion in combined recent M&A outlay). This strategic moat directly targets high-ticket, rapid-turnover professional projects. Crucially, HD's new "Other" segment (driven by SRS/GMS) is already generating a positive operating profit margin of 2.48%, proving the viability of its integration strategy. Furthermore, its MRO (Maintenance, Repair, and Operations) business acts as a vital counter-cyclical hedge against declining new home construction.

* Lowe’s Catch-Up Play: LOW doubled down on its Pro penetration by acquiring Foundation Building Materials (FBM) and Artisan Design Group (ADG) for approximately $10.1 billion. However, this pivot is currently in a "strategic loss" phase, operating at a -3.17% margin. LOW remains heavily reliant on its DIY-focused "Total Home" strategy to subsidize this Pro-segment transition.

Digital Transformation & AI-Driven Margin Protection

Facing severe wage pressures and a tight labor market, both companies deployed AI not just as a consumer gimmick, but as a core margin-protection mechanism.

Rather than traditional loss prevention, HD is utilizing Computer Vision to monitor overhead inventory in real-time, effectively reducing "shrink" and protecting its ~33% gross margin. In the Pro workflow, HD’s Blueprint Takeoffs tool uses AI to parse engineering blueprints and generate immediate material quotes, embedding HD into the earliest stages of contractor planning. Conversely, LOW’s AI application currently leans heavily on predictive inventory management and transaction friction reduction, leveraging a $400 million investment in supply chain hardware automation to offset labor costs.

Supply Chain Resilience & Cyclical Headwinds

As trade protectionism and tariff uncertainties loom, supply chain elasticity is paramount. HD operates a highly decentralized global sourcing network—spanning Mexico, Canada, India, Vietnam, and China (including Taiwan)—providing robust cost-sharing capabilities and agility. LOW, having divested its Canadian retail operations, now generates 99.9% of its revenue domestically while remaining highly concentrated in China and Mexico for imports, exposing it to higher structural tariff risks.

HDIN Viewpoint: The Institutional Perspective

From the desk of HDIN Research, the FY2025 performance reveals a sector transitioning from "asset-light" retail to "asset-heavy" B2B distribution. However, investors must scrutinize the severe ROIC (Return on Invested Capital) dilution both companies suffered this year (HD dropped from 31.3% to 25.7%; LOW from 32.0% to 26.1%). This indicates that the profitability of newly acquired M&A assets has not yet outpaced their cost of capital, weighed down by massive goodwill premiums.

Furthermore, we advise close monitoring of underlying accounting metrics. Lowe's exceptionally long Accounts Payable (AP) turnover (62.1 days vs. HD's 38.2 days) signals aggressive utilization of supplier financing. While this bolsters operating cash flow in the short term, any sudden contraction in supplier terms could expose hidden liquidity pressures. Ultimately, HD's structural integration into the Pro workflow affords it a superior ecosystem premium, while LOW’s valuation upside hinges entirely on successfully reversing the operating losses of its newly acquired Pro assets by FY2026.

Presentation Download & Media

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure 2025 HOME IMPROVEMENT TITANS: HOME DEPOT VS LOWE'S STRATEGIC & FINANCIALCOMPARISON

Financial Health & Capital Allocation EfficiencyWhile both companies maintain remarkably similar gross margins (~33.4%), Home Depot possesses an overwhelming advantage in scale and asset utilization. Generating $164.6 billion in total revenue compared to Lowe's $86.2 billion, HD's operational efficiency is best illustrated by its sales per square foot: $673 versus LOW’s $440.

A critical "So What" emerges in their FY2025 capital allocation strategies. Both giants have effectively paused or drastically slashed their historical stock repurchase programs to fund debt repayments and integrations of multi-billion-dollar acquisitions. This "defensive contraction" in buybacks reflects a prudent management pivot: prioritizing balance sheet stability and dividend safety in a high-cost capital environment over short-term EPS artificial inflation.

Strategic Pivots: The Race for the "Pro" Segment

The most defining collective movement of FY2025 is the heavy-asset leap into the Pro segment, driven by the need to establish a "second growth curve" amidst a stagnant DIY market.

* Home Depot's Scale Moat: HD solidified its dominance through the acquisitions of SRS Distribution and GMS (totaling over $23 billion in combined recent M&A outlay). This strategic moat directly targets high-ticket, rapid-turnover professional projects. Crucially, HD's new "Other" segment (driven by SRS/GMS) is already generating a positive operating profit margin of 2.48%, proving the viability of its integration strategy. Furthermore, its MRO (Maintenance, Repair, and Operations) business acts as a vital counter-cyclical hedge against declining new home construction.

* Lowe’s Catch-Up Play: LOW doubled down on its Pro penetration by acquiring Foundation Building Materials (FBM) and Artisan Design Group (ADG) for approximately $10.1 billion. However, this pivot is currently in a "strategic loss" phase, operating at a -3.17% margin. LOW remains heavily reliant on its DIY-focused "Total Home" strategy to subsidize this Pro-segment transition.

Digital Transformation & AI-Driven Margin Protection

Facing severe wage pressures and a tight labor market, both companies deployed AI not just as a consumer gimmick, but as a core margin-protection mechanism.

Rather than traditional loss prevention, HD is utilizing Computer Vision to monitor overhead inventory in real-time, effectively reducing "shrink" and protecting its ~33% gross margin. In the Pro workflow, HD’s Blueprint Takeoffs tool uses AI to parse engineering blueprints and generate immediate material quotes, embedding HD into the earliest stages of contractor planning. Conversely, LOW’s AI application currently leans heavily on predictive inventory management and transaction friction reduction, leveraging a $400 million investment in supply chain hardware automation to offset labor costs.

Supply Chain Resilience & Cyclical Headwinds

As trade protectionism and tariff uncertainties loom, supply chain elasticity is paramount. HD operates a highly decentralized global sourcing network—spanning Mexico, Canada, India, Vietnam, and China (including Taiwan)—providing robust cost-sharing capabilities and agility. LOW, having divested its Canadian retail operations, now generates 99.9% of its revenue domestically while remaining highly concentrated in China and Mexico for imports, exposing it to higher structural tariff risks.

HDIN Viewpoint: The Institutional Perspective

From the desk of HDIN Research, the FY2025 performance reveals a sector transitioning from "asset-light" retail to "asset-heavy" B2B distribution. However, investors must scrutinize the severe ROIC (Return on Invested Capital) dilution both companies suffered this year (HD dropped from 31.3% to 25.7%; LOW from 32.0% to 26.1%). This indicates that the profitability of newly acquired M&A assets has not yet outpaced their cost of capital, weighed down by massive goodwill premiums.

Furthermore, we advise close monitoring of underlying accounting metrics. Lowe's exceptionally long Accounts Payable (AP) turnover (62.1 days vs. HD's 38.2 days) signals aggressive utilization of supplier financing. While this bolsters operating cash flow in the short term, any sudden contraction in supplier terms could expose hidden liquidity pressures. Ultimately, HD's structural integration into the Pro workflow affords it a superior ecosystem premium, while LOW’s valuation upside hinges entirely on successfully reversing the operating losses of its newly acquired Pro assets by FY2026.

Presentation Download & Media

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com