2025 Global Home Care Giants: Navigating Cyclical Headwinds Through Pricing Power and Strategic Moats

Date : 2026-03-27

Reading : 318

In the complex macroeconomic landscape of 2025, global home care and FMCG giants have demonstrated remarkable resilience against cyclical headwinds. According to the latest sector analysis by HDIN Research, the industry is undergoing a profound paradigm shift. The era of volume-driven, all-category expansion has ended. Instead, market leaders are transitioning toward precision capital allocation, AI-driven operational efficiency, and value-driven pricing to combat inflation and the aggressive penetration of private labels.

Based on our deep-dive financial and strategic audits of top-tier players—including P&G, Unilever, Henkel, Kao, and Church & Dwight (C&D)—HDIN Research has identified the core competitive frameworks defining the 2025 market landscape.

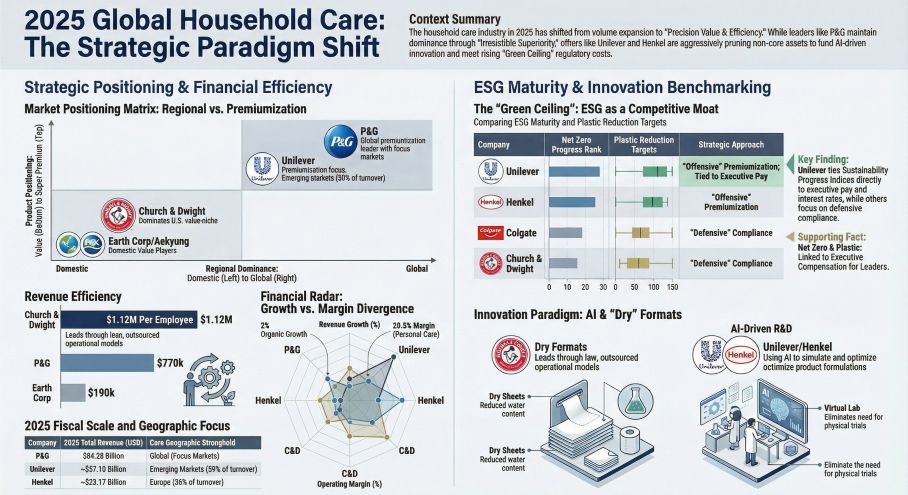

Figure 2025 Global Household Care: The Strategic Paradigm Shift

Strategic Pivots & Capital Allocation Efficiency

Strategic Pivots & Capital Allocation Efficiency

A defining characteristic of 2025 is the sharp polarization in capital allocation, specifically the strategic divestment of non-core, low-margin assets to optimize corporate profit pools. Companies are aggressively shedding structural weight to achieve organizational agility.

Unilever executed a radical simplification plan, notably spinning off its ice cream business to pivot its capital allocation toward high-margin "Power Brands" in the Beauty & Wellbeing sector. Similarly, Henkel divested its North American retail brand (private label) business, a calculated move that sacrificed pure top-line scale to dramatically enhance its adjusted EBIT margins to 14.8%. This structural "slimming down" allows these giants to redirect capital expenditures (CAPEX) toward high-growth, high-retention segments, fortifying their sector positioning against macroeconomic volatility.

Pricing Power and Defense Against Private Labels

Pure price hikes have reached a psychological and regulatory ceiling. To navigate inflation without destroying consumer demand, industry leaders have replaced blunt price increases with "technological premiumization."

Facing the threat of consumers trading down to private labels (white labels), companies are leveraging proprietary R&D to widen the performance gap. Unilever’s launch of *Wonder Wash*, engineered specifically for short-cycle, cold-water washing, exemplifies this moat. By addressing an unmet consumer need with advanced enzyme technology that white labels cannot easily replicate, Unilever achieved a 5.3% growth in developed markets.

Similarly, P&G continues to exercise its "Irresistible Superiority" strategy. By maintaining unparalleled performance and brand mindshare, P&G successfully pushed a 1% price increase to drive a 2% organic growth, showcasing absolute pricing power and channel clout, even as retailer partners like Walmart push their own store brands.

Financial Health & Supply Chain Resilience

A rigorous audit of operating cash flows (CFO) versus net income reveals a highly cash-generative industry, yet operational efficiency metrics expose clear divergence among the players.

P&G leads the sector in supply chain resilience, boasting an extraordinary inventory turnover rate of 7.13x. This is driven by deep investments in AI-powered demand forecasting and backend supply chain digitization, allowing the company to rapidly adapt to geographic disruptions.

Conversely, HDIN Research advises monitoring potential accounting risks tied to M&A integration and macroeconomic stress. Colgate-Palmolive’s massive $919 million impairment charge on its premium skin health business (Filorga) serves as a stark reminder of "Big Bath" accounting vulnerabilities when premiumization acquisitions collide with tightening consumer discretionary spending. Furthermore, heavy reliance on Supply Chain Financing (SCF) to artificially stretch payable cycles remains a hidden liquidity risk for several mid-to-large-tier players.

ESG as a Formidable Strategic Moat

Environmental, Social, and Governance (ESG) initiatives have officially transitioned from regulatory compliance costs to core drivers of brand premiumization. The "Green Ceiling" is reshaping product formats and supply chain economics.

Henkel has aggressively integrated post-consumer recycled (PCR) plastics, reaching up to 45% in its European consumer packaging, thereby mitigating future liabilities tied to impending plastic taxes. Meanwhile, Kao is defending its margins against volatile fossil-fuel-based raw material costs (like palm oil) through the deployment of its proprietary *Bio IOS* bio-surfactants.

Furthermore, structural innovation is redefining logistics. Church & Dwight’s strategic push into waterless formats, such as detergent sheets, not only appeals to eco-conscious consumers but drastically slashes water weight and transportation carbon footprints, creating a highly efficient value-niche positioning.

HDIN Viewpoint

The 2025 home care landscape is a watershed moment for brand valuation. HDIN Research concludes that the ultimate winners will be those who seamlessly translate complex sustainability tech and AI-driven R&D into perceptible consumer convenience. Mid-sized regional players like Earth Corp and Aekyung are finding success by monopolizing niche regional verticals and deploying "sharp top" technological agility. Moving forward, the true strategic moat will not simply be global scale, but the cognitive mindshare a brand commands and the speed at which its supply chain can pivot in a fragmented, post-inflationary world.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

About HDIN Research Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Based on our deep-dive financial and strategic audits of top-tier players—including P&G, Unilever, Henkel, Kao, and Church & Dwight (C&D)—HDIN Research has identified the core competitive frameworks defining the 2025 market landscape.

Figure 2025 Global Household Care: The Strategic Paradigm Shift

Strategic Pivots & Capital Allocation EfficiencyA defining characteristic of 2025 is the sharp polarization in capital allocation, specifically the strategic divestment of non-core, low-margin assets to optimize corporate profit pools. Companies are aggressively shedding structural weight to achieve organizational agility.

Unilever executed a radical simplification plan, notably spinning off its ice cream business to pivot its capital allocation toward high-margin "Power Brands" in the Beauty & Wellbeing sector. Similarly, Henkel divested its North American retail brand (private label) business, a calculated move that sacrificed pure top-line scale to dramatically enhance its adjusted EBIT margins to 14.8%. This structural "slimming down" allows these giants to redirect capital expenditures (CAPEX) toward high-growth, high-retention segments, fortifying their sector positioning against macroeconomic volatility.

Pricing Power and Defense Against Private Labels

Pure price hikes have reached a psychological and regulatory ceiling. To navigate inflation without destroying consumer demand, industry leaders have replaced blunt price increases with "technological premiumization."

Facing the threat of consumers trading down to private labels (white labels), companies are leveraging proprietary R&D to widen the performance gap. Unilever’s launch of *Wonder Wash*, engineered specifically for short-cycle, cold-water washing, exemplifies this moat. By addressing an unmet consumer need with advanced enzyme technology that white labels cannot easily replicate, Unilever achieved a 5.3% growth in developed markets.

Similarly, P&G continues to exercise its "Irresistible Superiority" strategy. By maintaining unparalleled performance and brand mindshare, P&G successfully pushed a 1% price increase to drive a 2% organic growth, showcasing absolute pricing power and channel clout, even as retailer partners like Walmart push their own store brands.

Financial Health & Supply Chain Resilience

A rigorous audit of operating cash flows (CFO) versus net income reveals a highly cash-generative industry, yet operational efficiency metrics expose clear divergence among the players.

P&G leads the sector in supply chain resilience, boasting an extraordinary inventory turnover rate of 7.13x. This is driven by deep investments in AI-powered demand forecasting and backend supply chain digitization, allowing the company to rapidly adapt to geographic disruptions.

Conversely, HDIN Research advises monitoring potential accounting risks tied to M&A integration and macroeconomic stress. Colgate-Palmolive’s massive $919 million impairment charge on its premium skin health business (Filorga) serves as a stark reminder of "Big Bath" accounting vulnerabilities when premiumization acquisitions collide with tightening consumer discretionary spending. Furthermore, heavy reliance on Supply Chain Financing (SCF) to artificially stretch payable cycles remains a hidden liquidity risk for several mid-to-large-tier players.

ESG as a Formidable Strategic Moat

Environmental, Social, and Governance (ESG) initiatives have officially transitioned from regulatory compliance costs to core drivers of brand premiumization. The "Green Ceiling" is reshaping product formats and supply chain economics.

Henkel has aggressively integrated post-consumer recycled (PCR) plastics, reaching up to 45% in its European consumer packaging, thereby mitigating future liabilities tied to impending plastic taxes. Meanwhile, Kao is defending its margins against volatile fossil-fuel-based raw material costs (like palm oil) through the deployment of its proprietary *Bio IOS* bio-surfactants.

Furthermore, structural innovation is redefining logistics. Church & Dwight’s strategic push into waterless formats, such as detergent sheets, not only appeals to eco-conscious consumers but drastically slashes water weight and transportation carbon footprints, creating a highly efficient value-niche positioning.

HDIN Viewpoint

The 2025 home care landscape is a watershed moment for brand valuation. HDIN Research concludes that the ultimate winners will be those who seamlessly translate complex sustainability tech and AI-driven R&D into perceptible consumer convenience. Mid-sized regional players like Earth Corp and Aekyung are finding success by monopolizing niche regional verticals and deploying "sharp top" technological agility. Moving forward, the true strategic moat will not simply be global scale, but the cognitive mindshare a brand commands and the speed at which its supply chain can pivot in a fragmented, post-inflationary world.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

About HDIN Research Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com