Global eVTOL 2025: Strategic Moats, Capital Allocation, and the Race to Commercialization

Date : 2026-03-30

Reading : 176

The Advanced Air Mobility (AAM) sector has officially crossed the rubicon from theoretical research and development to capital-intensive industrialization. Following a rigorous analysis of the 2025 annual reports from the top five global eVTOL leaders—Joby Aviation, Archer Aviation, Beta Technologies, Eve Holding, and Vertical Aerospace—HDIN Research notes a severe bifurcation in the market. The industry is no longer competing solely on aerodynamic physics; the new battlegrounds are capital allocation efficiency, supply chain sovereignty, and certification agility.

Here is our strategic breakdown of how these five pioneers are navigating the transition to commercialization and where the true systemic risks lie.

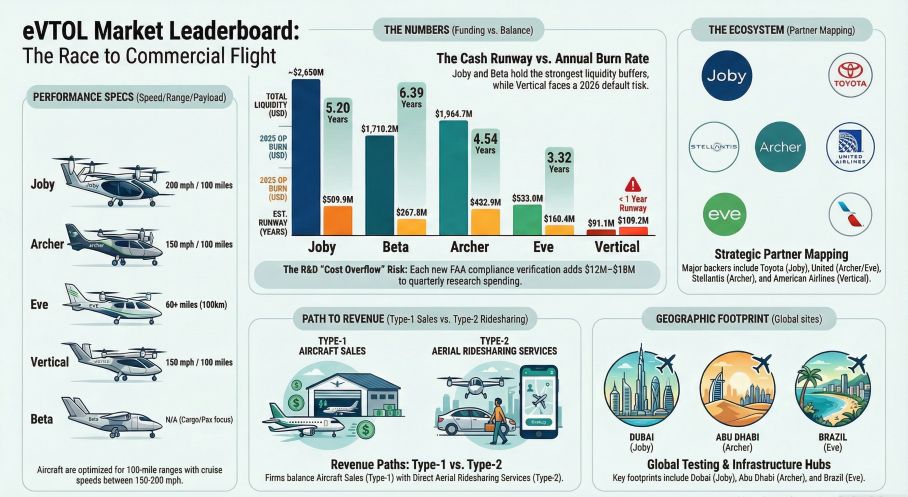

Figure eVTOL Market Leaderboard: The Race to Commercial Flight

Sector Positioning: Vertical Integration vs. Asset-Light Ecosystems

Sector Positioning: Vertical Integration vs. Asset-Light Ecosystems

The strategic moats within the eVTOL landscape are currently defined by two distinct operational philosophies: full-stack vertical integration and asset-light ecosystem partnerships.

* Deep Vertical Integration: Joby Aviation and Beta Technologies are aggressively insourcing their supply chains. By developing proprietary electric propulsion units (EPUs), flight control systems, and even charging infrastructure (Beta’s open-source Charge Cube network), these firms are strategically eliminating Tier-1 supplier premiums. The strategic implication: While this demands massive upfront capital, it secures high-margin, full-lifecycle revenue streams post-2028, positioning them to capture both hardware sales and software/service recurring revenues (e.g., Joby’s Elevate OS).

* Asset-Light Ecosystem Integration: Eve Holding and Vertical Aerospace have adopted an ecosystem-dependent model. Eve leverages the engineering dominance of its parent company, Embraer, transforming fixed overhead into variable costs. Vertical Aerospace relies entirely on premier aerospace suppliers like Honeywell and Rolls-Royce. The strategic implication: This limits R&D burn rates but exposes these companies to significant supply chain bottlenecks and margin compression as suppliers capture a larger share of the value chain.

Capital Allocation Efficiency & Financial Health

A deep dive into 2025 cash burn rates reveals a stark liquidity divide, determining which companies can weather the cyclical headwinds of regulatory delays.

* The Fortified Balance Sheets: Joby and Beta possess the deepest "cash moats" in the industry. Joby's aggressive capital allocation strategy, bolstered by a massive $1.24 billion capital raise in early 2026, pushes its total available liquidity to approximately $2.65 billion. This exceptional capital efficiency grants Joby the runway to scale high-volume manufacturing facilities in Ohio without the immediate threat of dilution.

* The High-Burn Growth Engine: Archer Aviation holds a robust $1.96 billion in liquidity, deeply backed by its automotive manufacturing partner, Stellantis. However, its operational cash burn exceeds $430 million annually. Its aggressive push to build out its Georgia facility means capital allocation must remain flawless to avoid returning to the equity markets.

* Imminent Liquidity Crises: Vertical Aerospace is facing severe cyclical headwinds. With cash reserves dwindling below $100 million and a formal "Going Concern" warning from its auditors, its capital structure is highly distressed. The company is on a ticking clock to secure vital funding before mid-2026, proving that technological milestones are irrelevant without absolute financial resilience.

Navigating Cyclical Headwinds: Red Flags in AAM

As the industry approaches its commercialization phase, HDIN Research urges investors to look past the marketing gloss and scrutinize several financial "red flags" masking underlying vulnerabilities:

1. The Illusion of the Backlog: Massive order books are often touted as future revenue, but they are predominantly non-binding. Eve claims an impressive 2,700-aircraft pipeline valued at $140 billion, yet nearly all are subject to successful certification and final terms. A failure to convert these Letters of Intent (LOIs) into firm, cash-backed Pre-Delivery Payments (PDPs) will cripple future revenue visibility.

2. Stock-Based Compensation (SBC) Camouflage: Companies like Archer are heavily utilizing SBC (accounting for over $223 million in 2025) to artificially suppress operational cash burn figures. While it protects cash reserves in the short term, it creates a massive equity dilution overhang for existing shareholders.

3. Debt Restructuring as "Profit": Vertical Aerospace’s reported 2025 net income of $307 million is not a triumph of operational efficiency; it is an accounting byproduct of convertible debt restructuring. Stripping away this non-cash gain reveals a deeply unprofitable enterprise struggling for survival.

HDIN Viewpoint: The 2026 Commercialization Inflection

At HDIN Research, we view 2026 as the definitive inflection point that will separate the enduring UAM titans from the speculative casualties. The FAA's categorization of eVTOLs as "Powered-Lift" vehicles has inherently raised the ceiling for certification costs.

Joby and Archer, currently navigating the intensive Phase 4 compliance execution, possess the capital moats required to absorb these regulatory shocks. Meanwhile, Beta’s pragmatic strategy of pursuing conventional takeoff and landing (CTOL) certification first will likely make it one of the earliest players to generate sustained, organic cash flow. Conversely, companies relying on asset-light models must rapidly convert non-binding momentum into hard capital, or they will be absorbed or driven out during the inevitable 2027-2028 industry consolidation phase.

Presentation Download & Media Access

* Click the PDF download link under “Related Topics” to access the presentation of this report.

* Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Here is our strategic breakdown of how these five pioneers are navigating the transition to commercialization and where the true systemic risks lie.

Figure eVTOL Market Leaderboard: The Race to Commercial Flight

Sector Positioning: Vertical Integration vs. Asset-Light EcosystemsThe strategic moats within the eVTOL landscape are currently defined by two distinct operational philosophies: full-stack vertical integration and asset-light ecosystem partnerships.

* Deep Vertical Integration: Joby Aviation and Beta Technologies are aggressively insourcing their supply chains. By developing proprietary electric propulsion units (EPUs), flight control systems, and even charging infrastructure (Beta’s open-source Charge Cube network), these firms are strategically eliminating Tier-1 supplier premiums. The strategic implication: While this demands massive upfront capital, it secures high-margin, full-lifecycle revenue streams post-2028, positioning them to capture both hardware sales and software/service recurring revenues (e.g., Joby’s Elevate OS).

* Asset-Light Ecosystem Integration: Eve Holding and Vertical Aerospace have adopted an ecosystem-dependent model. Eve leverages the engineering dominance of its parent company, Embraer, transforming fixed overhead into variable costs. Vertical Aerospace relies entirely on premier aerospace suppliers like Honeywell and Rolls-Royce. The strategic implication: This limits R&D burn rates but exposes these companies to significant supply chain bottlenecks and margin compression as suppliers capture a larger share of the value chain.

Capital Allocation Efficiency & Financial Health

A deep dive into 2025 cash burn rates reveals a stark liquidity divide, determining which companies can weather the cyclical headwinds of regulatory delays.

* The Fortified Balance Sheets: Joby and Beta possess the deepest "cash moats" in the industry. Joby's aggressive capital allocation strategy, bolstered by a massive $1.24 billion capital raise in early 2026, pushes its total available liquidity to approximately $2.65 billion. This exceptional capital efficiency grants Joby the runway to scale high-volume manufacturing facilities in Ohio without the immediate threat of dilution.

* The High-Burn Growth Engine: Archer Aviation holds a robust $1.96 billion in liquidity, deeply backed by its automotive manufacturing partner, Stellantis. However, its operational cash burn exceeds $430 million annually. Its aggressive push to build out its Georgia facility means capital allocation must remain flawless to avoid returning to the equity markets.

* Imminent Liquidity Crises: Vertical Aerospace is facing severe cyclical headwinds. With cash reserves dwindling below $100 million and a formal "Going Concern" warning from its auditors, its capital structure is highly distressed. The company is on a ticking clock to secure vital funding before mid-2026, proving that technological milestones are irrelevant without absolute financial resilience.

Navigating Cyclical Headwinds: Red Flags in AAM

As the industry approaches its commercialization phase, HDIN Research urges investors to look past the marketing gloss and scrutinize several financial "red flags" masking underlying vulnerabilities:

1. The Illusion of the Backlog: Massive order books are often touted as future revenue, but they are predominantly non-binding. Eve claims an impressive 2,700-aircraft pipeline valued at $140 billion, yet nearly all are subject to successful certification and final terms. A failure to convert these Letters of Intent (LOIs) into firm, cash-backed Pre-Delivery Payments (PDPs) will cripple future revenue visibility.

2. Stock-Based Compensation (SBC) Camouflage: Companies like Archer are heavily utilizing SBC (accounting for over $223 million in 2025) to artificially suppress operational cash burn figures. While it protects cash reserves in the short term, it creates a massive equity dilution overhang for existing shareholders.

3. Debt Restructuring as "Profit": Vertical Aerospace’s reported 2025 net income of $307 million is not a triumph of operational efficiency; it is an accounting byproduct of convertible debt restructuring. Stripping away this non-cash gain reveals a deeply unprofitable enterprise struggling for survival.

HDIN Viewpoint: The 2026 Commercialization Inflection

At HDIN Research, we view 2026 as the definitive inflection point that will separate the enduring UAM titans from the speculative casualties. The FAA's categorization of eVTOLs as "Powered-Lift" vehicles has inherently raised the ceiling for certification costs.

Joby and Archer, currently navigating the intensive Phase 4 compliance execution, possess the capital moats required to absorb these regulatory shocks. Meanwhile, Beta’s pragmatic strategy of pursuing conventional takeoff and landing (CTOL) certification first will likely make it one of the earliest players to generate sustained, organic cash flow. Conversely, companies relying on asset-light models must rapidly convert non-binding momentum into hard capital, or they will be absorbed or driven out during the inevitable 2027-2028 industry consolidation phase.

Presentation Download & Media Access

* Click the PDF download link under “Related Topics” to access the presentation of this report.

* Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com