Decoding 2025 Aero-Engine Strategic Moats: How GE, RTX, and Rolls-Royce Navigate Capital Efficiency and Supply Chain Headwinds

Date : 2026-03-30

Reading : 670

The 2025 global aero-engine landscape has crystallized into a highly entrenched oligopoly. Based on a deep-dive analysis of the latest annual reports, the sector is currently characterized by a dichotomy: unprecedented commercial backlogs offset by severe supply chain and maintenance, repair, and overhaul (MRO) bottlenecks.

For industry stakeholders, the narrative has shifted fundamentally. Market dominance is no longer solely dictated by engine sales; it is now defined by the ability to execute seamless generational transitions, enforce "value pricing" in aftermarket services, and mitigate geopolitical supply chain vulnerabilities.

Figure 2025 Aero-Engine Triopoly: Service-Led Growth Offsets Global Supply Constraints

Sector Positioning and Capital Allocation Efficiency

Sector Positioning and Capital Allocation Efficiency

The transition from legacy "cash cow" models to next-generation engines has distinctly bifurcated the financial health of the top three OEMs.

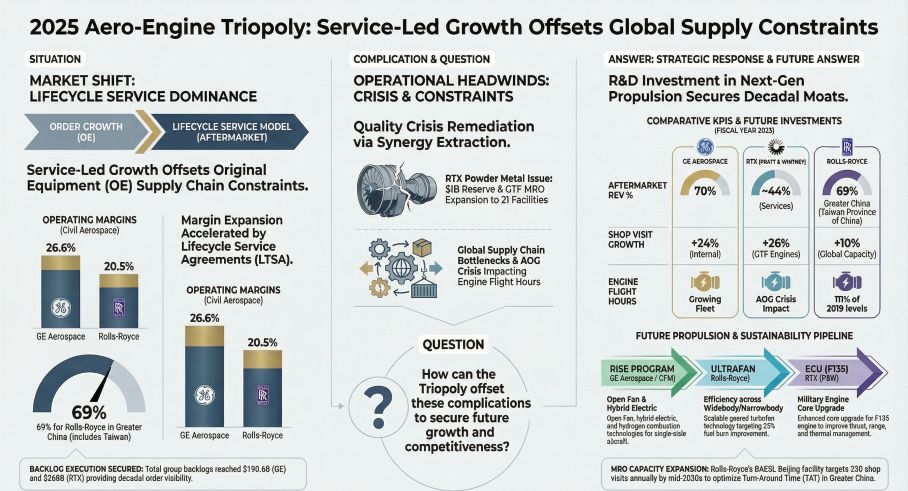

* GE Aerospace: Operating from a position of profound strength, GE’s seamless transition from the CFM56 to the LEAP engine has cemented its narrow-body dominance. Driven by its proprietary "FLIGHT DECK" lean management model, GE not only achieved a massive scale-up—delivering 1,802 LEAP engines in 2025—but also secured an industry-leading segment profit margin of 26.6%. By vertically integrating advanced materials (like CMC and 3D printing) under a "technological sovereignty" strategy, GE has effectively diluted its initial R&D capital expenditures through unparalleled scale.

* Rolls-Royce (RR): RR has executed a dramatic financial turnaround, pushing its underlying civil aerospace operating margin to 20.5%. By dominating the wide-body market (capturing a 38% installed base share via sole-source platforms like the A350 and A330neo), RR has successfully renegotiated Long-Term Service Agreements (LTSAs). This shift toward aggressive "value pricing" has transformed its next-generation Trent engines into a formidable free-cash-flow generator, elevating its LTSA balance to nearly $13.72 billion.

* RTX (Pratt & Whitney): Despite sitting on a staggering $151 billion departmental backlog, RTX is currently battling severe cyclical headwinds. The fallout from the GTF powder metal quality event has forced RTX to allocate $1 billion in customer compensation, dragging its departmental profit margin down to a subdued 7.9%. This serves as a stark reminder that in advanced aerospace manufacturing, the financial penalty for core material failures far outweighs the cost savings of outsourced integration.

Navigating Supply Chain Vulnerabilities and Geopolitical Headwinds

In 2025, upstream material procurement is characterized by the dual threats of structural shortages and geopolitical fragility. OEMs are pivoting from cost-reduction to supply-chain resilience.

The reliance on critical minerals—such as titanium, cobalt, and rare earths—has exposed deep geopolitical soft spots. Sanctions on Russian titanium have forced OEMs like RTX to absorb non-recurring impairment charges as they scramble for alternative sources. Meanwhile, potential trade decoupling with China threatens the supply of rare earths vital for advanced magnetic components.

To hedge against these risks, capital allocation strategies have diverged. GE is injecting $1 billion into MRO and supply capacity expansion, deeply integrating into Tier-2 suppliers to improve yield rates. Rolls-Royce has adopted an aggressive hands-on approach, physically embedding RR personnel within key suppliers to unblock bottlenecks. Conversely, RTX is leveraging its "CORE" digital platform to monitor global supply dynamics in real-time, mandating dual-sourcing to buffer against single-point-of-failure risks.

MRO Bottlenecks and the "Aircraft on Ground" (AOG) Crisis

The MRO sector has structurally transformed from a high-margin profit engine into a critical delivery bottleneck. A shortage of skilled labor combined with unpredictable spare parts delivery has triggered an industry-wide spike in Turn-Around Times (TAT).

RTX is facing the most acute pressure, with GTF powder metal inspections causing a prolonged "Aircraft on Ground" (AOG) crisis expected to persist through late 2026. To alleviate these facility overloads, OEMs are accelerating the deployment of Predictive Health Monitoring (PHM) and Digital Twins to shift from reactive maintenance to optimized, predictive part replacement. Additionally, Used Serviceable Materials (USM) are being strategically utilized to bypass raw material delays and protect OEM profit margins, though they introduce complex actuarial risks for future LTSA cost projections.

The Strategic Role of Greater China Joint Ventures

Greater China has fully transitioned from a mere "sales destination" into the epicenter of global lifecycle service support. Compliance with global ESG standards and local joint venture dynamics are now key drivers of regional profitability.

Rolls-Royce’s robust net cash position is heavily underpinned by its MRO joint ventures in Greater China. The HAESL facility in Hong Kong generated nearly $4.84 billion in revenue, while the newly established BAESL facility in Beijing locks in the servicing rights for China’s expanding wide-body fleet for the next decade. GE relies heavily on its Taiwan-based joint venture to maintain the high-frequency TAT required by the LEAP fleet. Meanwhile, RTX faces a more complex operational environment; while its Shanghai MRO center is a critical node for the GTF network, the company must carefully navigate heightened export controls and compliance scrutiny linked to its extensive defense portfolio.

Furthermore, all OEMs are facing a rising "Green Premium." Imposed carbon pricing and ESG compliance within the supply chain are projected to increase LTSA cost bases by roughly 1%, forcing OEMs to pass these costs onto airlines during contract renewals.

HDIN Viewpoint: Institutional Perspective

From the analytical lens of HDIN Research, the 2025 aero-engine market rewards operational predictability over mere technological promise.

GE Aerospace currently presents the highest strategic certainty. Its mastery of the FLIGHT DECK lean model and in-house control over additive manufacturing patents create an incredibly deep moat against MRO capacity constraints. Rolls-Royce represents the most successful pivot to a "light-asset, high-yield" partnership model; however, its comparatively low R&D expenditure warrants close monitoring regarding its next-generation narrow-body pipeline (e.g., UltraFan). RTX carries the highest near-term uncertainty. While its long-term backlog remains a massive asset, its immediate cash flow will be heavily dictated by its ability to resolve the GTF AOG backlog and navigate complex geopolitical compliance frameworks in the Asia-Pacific region.

Ultimately, the OEMs that can successfully digitize their supply chains and enforce value-based aftermarket pricing will monopolize the industry's profit pools through the end of the decade.

Presentation Download:

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research Profile:

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

For industry stakeholders, the narrative has shifted fundamentally. Market dominance is no longer solely dictated by engine sales; it is now defined by the ability to execute seamless generational transitions, enforce "value pricing" in aftermarket services, and mitigate geopolitical supply chain vulnerabilities.

Figure 2025 Aero-Engine Triopoly: Service-Led Growth Offsets Global Supply Constraints

Sector Positioning and Capital Allocation EfficiencyThe transition from legacy "cash cow" models to next-generation engines has distinctly bifurcated the financial health of the top three OEMs.

* GE Aerospace: Operating from a position of profound strength, GE’s seamless transition from the CFM56 to the LEAP engine has cemented its narrow-body dominance. Driven by its proprietary "FLIGHT DECK" lean management model, GE not only achieved a massive scale-up—delivering 1,802 LEAP engines in 2025—but also secured an industry-leading segment profit margin of 26.6%. By vertically integrating advanced materials (like CMC and 3D printing) under a "technological sovereignty" strategy, GE has effectively diluted its initial R&D capital expenditures through unparalleled scale.

* Rolls-Royce (RR): RR has executed a dramatic financial turnaround, pushing its underlying civil aerospace operating margin to 20.5%. By dominating the wide-body market (capturing a 38% installed base share via sole-source platforms like the A350 and A330neo), RR has successfully renegotiated Long-Term Service Agreements (LTSAs). This shift toward aggressive "value pricing" has transformed its next-generation Trent engines into a formidable free-cash-flow generator, elevating its LTSA balance to nearly $13.72 billion.

* RTX (Pratt & Whitney): Despite sitting on a staggering $151 billion departmental backlog, RTX is currently battling severe cyclical headwinds. The fallout from the GTF powder metal quality event has forced RTX to allocate $1 billion in customer compensation, dragging its departmental profit margin down to a subdued 7.9%. This serves as a stark reminder that in advanced aerospace manufacturing, the financial penalty for core material failures far outweighs the cost savings of outsourced integration.

Navigating Supply Chain Vulnerabilities and Geopolitical Headwinds

In 2025, upstream material procurement is characterized by the dual threats of structural shortages and geopolitical fragility. OEMs are pivoting from cost-reduction to supply-chain resilience.

The reliance on critical minerals—such as titanium, cobalt, and rare earths—has exposed deep geopolitical soft spots. Sanctions on Russian titanium have forced OEMs like RTX to absorb non-recurring impairment charges as they scramble for alternative sources. Meanwhile, potential trade decoupling with China threatens the supply of rare earths vital for advanced magnetic components.

To hedge against these risks, capital allocation strategies have diverged. GE is injecting $1 billion into MRO and supply capacity expansion, deeply integrating into Tier-2 suppliers to improve yield rates. Rolls-Royce has adopted an aggressive hands-on approach, physically embedding RR personnel within key suppliers to unblock bottlenecks. Conversely, RTX is leveraging its "CORE" digital platform to monitor global supply dynamics in real-time, mandating dual-sourcing to buffer against single-point-of-failure risks.

MRO Bottlenecks and the "Aircraft on Ground" (AOG) Crisis

The MRO sector has structurally transformed from a high-margin profit engine into a critical delivery bottleneck. A shortage of skilled labor combined with unpredictable spare parts delivery has triggered an industry-wide spike in Turn-Around Times (TAT).

RTX is facing the most acute pressure, with GTF powder metal inspections causing a prolonged "Aircraft on Ground" (AOG) crisis expected to persist through late 2026. To alleviate these facility overloads, OEMs are accelerating the deployment of Predictive Health Monitoring (PHM) and Digital Twins to shift from reactive maintenance to optimized, predictive part replacement. Additionally, Used Serviceable Materials (USM) are being strategically utilized to bypass raw material delays and protect OEM profit margins, though they introduce complex actuarial risks for future LTSA cost projections.

The Strategic Role of Greater China Joint Ventures

Greater China has fully transitioned from a mere "sales destination" into the epicenter of global lifecycle service support. Compliance with global ESG standards and local joint venture dynamics are now key drivers of regional profitability.

Rolls-Royce’s robust net cash position is heavily underpinned by its MRO joint ventures in Greater China. The HAESL facility in Hong Kong generated nearly $4.84 billion in revenue, while the newly established BAESL facility in Beijing locks in the servicing rights for China’s expanding wide-body fleet for the next decade. GE relies heavily on its Taiwan-based joint venture to maintain the high-frequency TAT required by the LEAP fleet. Meanwhile, RTX faces a more complex operational environment; while its Shanghai MRO center is a critical node for the GTF network, the company must carefully navigate heightened export controls and compliance scrutiny linked to its extensive defense portfolio.

Furthermore, all OEMs are facing a rising "Green Premium." Imposed carbon pricing and ESG compliance within the supply chain are projected to increase LTSA cost bases by roughly 1%, forcing OEMs to pass these costs onto airlines during contract renewals.

HDIN Viewpoint: Institutional Perspective

From the analytical lens of HDIN Research, the 2025 aero-engine market rewards operational predictability over mere technological promise.

GE Aerospace currently presents the highest strategic certainty. Its mastery of the FLIGHT DECK lean model and in-house control over additive manufacturing patents create an incredibly deep moat against MRO capacity constraints. Rolls-Royce represents the most successful pivot to a "light-asset, high-yield" partnership model; however, its comparatively low R&D expenditure warrants close monitoring regarding its next-generation narrow-body pipeline (e.g., UltraFan). RTX carries the highest near-term uncertainty. While its long-term backlog remains a massive asset, its immediate cash flow will be heavily dictated by its ability to resolve the GTF AOG backlog and navigate complex geopolitical compliance frameworks in the Asia-Pacific region.

Ultimately, the OEMs that can successfully digitize their supply chains and enforce value-based aftermarket pricing will monopolize the industry's profit pools through the end of the decade.

Presentation Download:

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research Profile:

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com