Microsoft vs. Kingsoft Office 2025: Deciphering AI Moats and Capital Allocation Efficiency

Date : 2026-03-30

Reading : 173

The 2025 financial landscape for productivity software reveals a definitive paradigm shift from legacy toolsets to AI-driven organizational ecosystems. Based on a rigorous structural teardown by HDIN Research, Microsoft and Kingsoft Office are demonstrating diverging yet highly effective approaches to capital allocation efficiency and sector positioning.

While Microsoft is leveraging its sheer scale to drive immediate Average Revenue Per User (ARPU) expansion via Copilot, Kingsoft Office is aggressively capitalizing on localized "Xinchuang" (IT Application Innovation) policies to forge deep, impenetrable B2B networks. Beyond the top-line growth, a closer look at their financial architecture reveals the true strategic moats—and hidden cyclical headwinds—defining the AI Agent era.

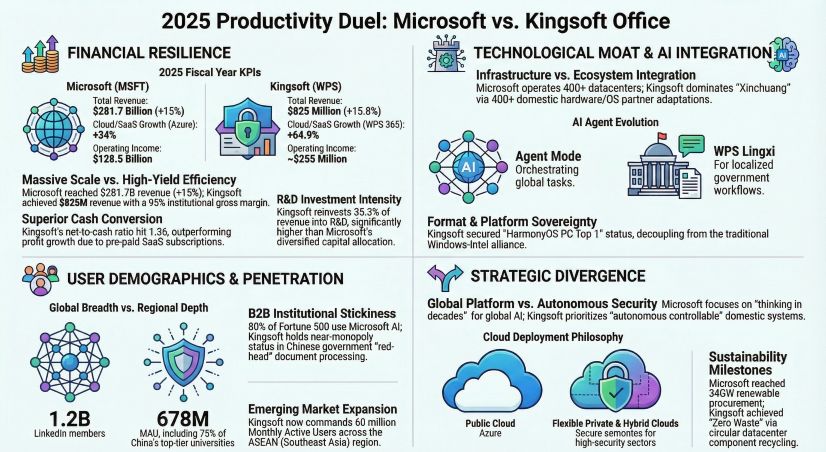

Figure 2025 Productivity Duel Microsoft vs Kingsoft Office Financial Health: The Power of the Subscription Cash Buffer

Financial Health: The Power of the Subscription Cash Buffer

A structural analysis of both firms reveals exceptional earnings quality, characterized by a Net-to-Cash ratio exceeding 1.0. Operating Cash Flow (OCF) consistently outpaces Net Income (NI) for both entities, but the underlying mechanics differ significantly.

* Kingsoft Office’s "Excess Cash" Phase: Kingsoft Office achieved a stellar Net-to-Cash ratio of 1.36 in 2025. This was driven by its aggressive transition from a licensing model to an institutional SaaS subscription model (WPS 365). Its massive accumulation of contract liabilities (totaling $362 million by the end of 2025) acts as an interest-free liquidity reservoir, insulating the company from macroeconomic shocks.

* Microsoft’s CapEx Balance: Microsoft’s colossal OCF is structured to absorb immense non-cash expenses, notably over $34 billion in depreciation and amortization from its aggressive AI infrastructure build-out, alongside nearly $12 billion in stock-based compensation (SBC). The strategic implication here is profound: Microsoft’s core business generates enough cash to fully self-fund its global AI dominance without stressing its balance sheet.

Strategic Moats and Sector Positioning

Both companies have successfully transitioned to the SaaS model, but their strategic moats are built on entirely different foundations.

* Microsoft: Global Ecosystem and ARPU Expansion: Microsoft’s moat is its ubiquitous "Intelligent Cloud" ecosystem. By embedding Copilot across Word, Excel, Teams, and Azure, Microsoft is driving a "bundling premium." This strategy directly translated into a 14% year-over-year revenue surge in its Microsoft 365 commercial and cloud services, proving that its AI value proposition is successfully extracting higher ARPU from existing enterprise clients.

* Kingsoft Office: Format Sovereignty and Private Deployment: Kingsoft Office’s sector positioning is anchored in hyper-localized compliance. It has established an impenetrable moat in China’s government and central state-owned enterprise (SOE) markets. By offering flexible private and hybrid cloud deployments, resolving AI hallucinations via its Knowledge Augmented Generation (KAG) framework, and achieving a 64.93% revenue surge in its WPS 365 business, Kingsoft has effectively neutralized Microsoft's public-cloud dominance in highly regulated regional sectors.

Cyclical Headwinds and Structural Risk Exposure

Despite robust top-line performance, our analysis flags specific financial stress points that warrant careful investor scrutiny.

* Accounts Receivable vs. Revenue Asymmetry: Kingsoft Office reported a 26.1% surge in Accounts Receivable, notably outpacing its 15.78% revenue growth. This structural risk exposure highlights the cost of aggressive B2B market expansion. As Kingsoft penetrates deeper into the institutional market, elongated payment cycles could squeeze short-term liquidity, serving as a critical indicator of shifting enterprise bargaining power.

* Capital Allocation and Margin Compression: Both companies exhibit extreme accounting prudence by fully expensing their R&D outlays rather than capitalizing them. However, Kingsoft’s R&D intensity stands at a staggering 35.34% of revenue—more than three times that of Microsoft (~10.6%). While this "All in AI" strategy ensures long-term technological independence, it creates near-term margin friction. Concurrently, Microsoft faces its own cyclical headwinds: the massive capital expenditure required to scale Azure’s AI infrastructure poses future margin dilution risks if AI token consumption fails to outpace server depreciation.

HDIN Viewpoint: The Shift to AI Agents

From the perspective of HDIN Research, the productivity software sector is crossing the rubicon from "functional AI tools" to "autonomous AI Agents."

Microsoft is currently winning the global scale war, utilizing its unmatched capital efficiency—where revenue per employee is roughly nine times that of Kingsoft—to blanket the enterprise market. However, Kingsoft Office is executing a masterclass in asymmetric warfare. By enduring short-term profitability compression to maintain a 35%+ R&D ratio, Kingsoft is transitioning from "passive compatibility" to establishing dominant, autonomous industry standards within the domestic tech ecosystem (such as dominating HarmonyOS PC application rankings). Ultimately, the victor in the next 24 months will be the platform that seamlessly transitions high-cost AI R&D into sticky, indispensable enterprise automation.

Presentation download:

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

While Microsoft is leveraging its sheer scale to drive immediate Average Revenue Per User (ARPU) expansion via Copilot, Kingsoft Office is aggressively capitalizing on localized "Xinchuang" (IT Application Innovation) policies to forge deep, impenetrable B2B networks. Beyond the top-line growth, a closer look at their financial architecture reveals the true strategic moats—and hidden cyclical headwinds—defining the AI Agent era.

Figure 2025 Productivity Duel Microsoft vs Kingsoft Office

Financial Health: The Power of the Subscription Cash BufferA structural analysis of both firms reveals exceptional earnings quality, characterized by a Net-to-Cash ratio exceeding 1.0. Operating Cash Flow (OCF) consistently outpaces Net Income (NI) for both entities, but the underlying mechanics differ significantly.

* Kingsoft Office’s "Excess Cash" Phase: Kingsoft Office achieved a stellar Net-to-Cash ratio of 1.36 in 2025. This was driven by its aggressive transition from a licensing model to an institutional SaaS subscription model (WPS 365). Its massive accumulation of contract liabilities (totaling $362 million by the end of 2025) acts as an interest-free liquidity reservoir, insulating the company from macroeconomic shocks.

* Microsoft’s CapEx Balance: Microsoft’s colossal OCF is structured to absorb immense non-cash expenses, notably over $34 billion in depreciation and amortization from its aggressive AI infrastructure build-out, alongside nearly $12 billion in stock-based compensation (SBC). The strategic implication here is profound: Microsoft’s core business generates enough cash to fully self-fund its global AI dominance without stressing its balance sheet.

Strategic Moats and Sector Positioning

Both companies have successfully transitioned to the SaaS model, but their strategic moats are built on entirely different foundations.

* Microsoft: Global Ecosystem and ARPU Expansion: Microsoft’s moat is its ubiquitous "Intelligent Cloud" ecosystem. By embedding Copilot across Word, Excel, Teams, and Azure, Microsoft is driving a "bundling premium." This strategy directly translated into a 14% year-over-year revenue surge in its Microsoft 365 commercial and cloud services, proving that its AI value proposition is successfully extracting higher ARPU from existing enterprise clients.

* Kingsoft Office: Format Sovereignty and Private Deployment: Kingsoft Office’s sector positioning is anchored in hyper-localized compliance. It has established an impenetrable moat in China’s government and central state-owned enterprise (SOE) markets. By offering flexible private and hybrid cloud deployments, resolving AI hallucinations via its Knowledge Augmented Generation (KAG) framework, and achieving a 64.93% revenue surge in its WPS 365 business, Kingsoft has effectively neutralized Microsoft's public-cloud dominance in highly regulated regional sectors.

Cyclical Headwinds and Structural Risk Exposure

Despite robust top-line performance, our analysis flags specific financial stress points that warrant careful investor scrutiny.

* Accounts Receivable vs. Revenue Asymmetry: Kingsoft Office reported a 26.1% surge in Accounts Receivable, notably outpacing its 15.78% revenue growth. This structural risk exposure highlights the cost of aggressive B2B market expansion. As Kingsoft penetrates deeper into the institutional market, elongated payment cycles could squeeze short-term liquidity, serving as a critical indicator of shifting enterprise bargaining power.

* Capital Allocation and Margin Compression: Both companies exhibit extreme accounting prudence by fully expensing their R&D outlays rather than capitalizing them. However, Kingsoft’s R&D intensity stands at a staggering 35.34% of revenue—more than three times that of Microsoft (~10.6%). While this "All in AI" strategy ensures long-term technological independence, it creates near-term margin friction. Concurrently, Microsoft faces its own cyclical headwinds: the massive capital expenditure required to scale Azure’s AI infrastructure poses future margin dilution risks if AI token consumption fails to outpace server depreciation.

HDIN Viewpoint: The Shift to AI Agents

From the perspective of HDIN Research, the productivity software sector is crossing the rubicon from "functional AI tools" to "autonomous AI Agents."

Microsoft is currently winning the global scale war, utilizing its unmatched capital efficiency—where revenue per employee is roughly nine times that of Kingsoft—to blanket the enterprise market. However, Kingsoft Office is executing a masterclass in asymmetric warfare. By enduring short-term profitability compression to maintain a 35%+ R&D ratio, Kingsoft is transitioning from "passive compatibility" to establishing dominant, autonomous industry standards within the domestic tech ecosystem (such as dominating HarmonyOS PC application rankings). Ultimately, the victor in the next 24 months will be the platform that seamlessly transitions high-cost AI R&D into sticky, indispensable enterprise automation.

Presentation download:

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com