SMIC 2025 Strategic Review: How Localization and Specialty Moats Forged a $9.36 Billion Revenue Surge

Date : 2026-03-30

Reading : 75

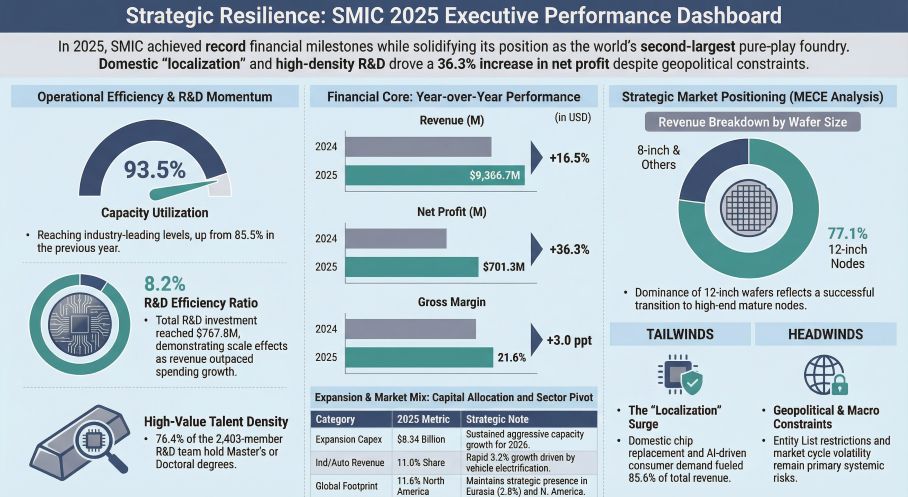

In 2025, Semiconductor Manufacturing International Corporation (SMIC) successfully navigated a labyrinth of geopolitical restrictions and cyclical headwinds, solidifying its position as the world’s second-largest pure-play foundry. Far beyond merely posting a record-breaking $9.36 billion in revenue, SMIC’s latest annual data reveals a profound structural transformation. By aggressively accelerating supply chain “localization” and pivoting toward high-margin specialty processes, the company has effectively rewritten its growth logic—shifting from sheer technological catch-up to a resilient, three-pronged strategy of technological differentiation, platform diversity, and regional supply security.

Figure Strategic Resilience: SMlC 2025 Executive Performance Dashboard

Financial Health: Capital Allocation Efficiency and Margin Expansion

Financial Health: Capital Allocation Efficiency and Margin Expansion

In a highly capital-intensive sector, SMIC’s 2025 financial posture demonstrates exceptional capital allocation efficiency. The company achieved a 16.5% year-over-year revenue growth, reaching $9.36 billion, alongside a remarkable 36.3% surge in net profit to $701.32 million.

The strategic takeaway lies in the anatomy of its gross margin recovery, which expanded to 21.6%. This margin expansion was not driven by favorable pricing power—in fact, the average selling price (ASP) for 8-inch equivalent wafers experienced a slight contraction to $901. Instead, the profitability surge was engineered through a massive scale effect. Capacity utilization climbed sharply to 93.5% (up from 85.5% in 2024), effectively diluting the massive $3.8 billion in annual depreciation costs. Furthermore, a structural shift toward 12-inch wafers, which now account for 77.1% of total revenue, optimized the product mix and cemented the financial baseline for future capital expenditures.

Strategic Moats: Specialty Processes and Advanced Packaging

Facing entrenched global competitors and severe geopolitical chokepoints regarding extreme ultraviolet (EUV) equipment and advanced EDA tools, SMIC has pragmatically deepened its strategic moats in "Specialty Platforms."

Rather than engaging in a symmetric war over single-digit nanometer nodes, SMIC has dominated the mid-to-high-end mature nodes. Key milestones in 2025 include the mass production of the 28nm ultra-low leakage platform, breakthroughs in 28nm embedded flash (crucial for high-end automotive MCUs), and the advancement of 65nm RF-SOI technologies which now boast industry-leading performance metrics.

Simultaneously, recognizing that the future of compute lies beyond traditional Moore's Law scaling, SMIC established a dedicated Advanced Packaging Institute in 2025. This strategic pivot toward heterogeneous integration serves as a critical bridge to capture future AI and data center computational demands, offsetting limitations in transistor miniaturization.

Sector Positioning: Navigating Cyclical Headwinds

SMIC’s revenue geometry in 2025 reflects a deliberate recalibration of its sector positioning. While traditional smartphone contributions declined to 23.1% amidst elongated upgrade cycles and memory chip cost pressures, the company successfully aggressively captured ground in the Industrial and Automotive sectors, which grew to represent 11.0% of total revenue.

This sectoral pivot is a vital defense mechanism against cyclical headwinds. Automotive electronics demand rigorous certification cycles, creating high client stickiness. By serving as the primary vehicle for Chinese domestic automotive substitution, SMIC has locked in long-term, high-visibility demand that buffers the inherent volatility of the consumer electronics market.

HDIN Viewpoint: Prudent Defense Meets Offensive Expansion

From the institutional perspective of HDIN Research, SMIC’s 2025 performance marks its entry into a mature phase characterized by "scale effect plus quality optimization." Management's 2026 guidance—projecting revenue growth above the industry average while holding capital expenditures flat at approximately $8.3 billion—signals a sophisticated balancing act.

However, we advise institutional investors to maintain a vigilant watch on specific structural risks. While the balance sheet remains exceptionally robust with over $11 billion in liquidity, SMIC's inventory swelled by 36.8% to $3.55 billion in 2025. If the macroeconomic recovery in downstream consumer electronics falters, this inventory buildup, coupled with the impending peak depreciation cliff from ongoing mega-fab expansions in Shanghai and Beijing, could introduce asset impairment vulnerabilities. Ultimately, SMIC's 2026 trajectory will be defined by its ability to maintain its localization momentum while outmaneuvering the looming specter of global mature-node overcapacity.

Presentation Download & Media Access

To dive deeper into the data and strategic frameworks discussed in this analysis:

* Click the PDF download link under “Related Topics” to access the presentation of this report.

* Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure Strategic Resilience: SMlC 2025 Executive Performance Dashboard

Financial Health: Capital Allocation Efficiency and Margin ExpansionIn a highly capital-intensive sector, SMIC’s 2025 financial posture demonstrates exceptional capital allocation efficiency. The company achieved a 16.5% year-over-year revenue growth, reaching $9.36 billion, alongside a remarkable 36.3% surge in net profit to $701.32 million.

The strategic takeaway lies in the anatomy of its gross margin recovery, which expanded to 21.6%. This margin expansion was not driven by favorable pricing power—in fact, the average selling price (ASP) for 8-inch equivalent wafers experienced a slight contraction to $901. Instead, the profitability surge was engineered through a massive scale effect. Capacity utilization climbed sharply to 93.5% (up from 85.5% in 2024), effectively diluting the massive $3.8 billion in annual depreciation costs. Furthermore, a structural shift toward 12-inch wafers, which now account for 77.1% of total revenue, optimized the product mix and cemented the financial baseline for future capital expenditures.

Strategic Moats: Specialty Processes and Advanced Packaging

Facing entrenched global competitors and severe geopolitical chokepoints regarding extreme ultraviolet (EUV) equipment and advanced EDA tools, SMIC has pragmatically deepened its strategic moats in "Specialty Platforms."

Rather than engaging in a symmetric war over single-digit nanometer nodes, SMIC has dominated the mid-to-high-end mature nodes. Key milestones in 2025 include the mass production of the 28nm ultra-low leakage platform, breakthroughs in 28nm embedded flash (crucial for high-end automotive MCUs), and the advancement of 65nm RF-SOI technologies which now boast industry-leading performance metrics.

Simultaneously, recognizing that the future of compute lies beyond traditional Moore's Law scaling, SMIC established a dedicated Advanced Packaging Institute in 2025. This strategic pivot toward heterogeneous integration serves as a critical bridge to capture future AI and data center computational demands, offsetting limitations in transistor miniaturization.

Sector Positioning: Navigating Cyclical Headwinds

SMIC’s revenue geometry in 2025 reflects a deliberate recalibration of its sector positioning. While traditional smartphone contributions declined to 23.1% amidst elongated upgrade cycles and memory chip cost pressures, the company successfully aggressively captured ground in the Industrial and Automotive sectors, which grew to represent 11.0% of total revenue.

This sectoral pivot is a vital defense mechanism against cyclical headwinds. Automotive electronics demand rigorous certification cycles, creating high client stickiness. By serving as the primary vehicle for Chinese domestic automotive substitution, SMIC has locked in long-term, high-visibility demand that buffers the inherent volatility of the consumer electronics market.

HDIN Viewpoint: Prudent Defense Meets Offensive Expansion

From the institutional perspective of HDIN Research, SMIC’s 2025 performance marks its entry into a mature phase characterized by "scale effect plus quality optimization." Management's 2026 guidance—projecting revenue growth above the industry average while holding capital expenditures flat at approximately $8.3 billion—signals a sophisticated balancing act.

However, we advise institutional investors to maintain a vigilant watch on specific structural risks. While the balance sheet remains exceptionally robust with over $11 billion in liquidity, SMIC's inventory swelled by 36.8% to $3.55 billion in 2025. If the macroeconomic recovery in downstream consumer electronics falters, this inventory buildup, coupled with the impending peak depreciation cliff from ongoing mega-fab expansions in Shanghai and Beijing, could introduce asset impairment vulnerabilities. Ultimately, SMIC's 2026 trajectory will be defined by its ability to maintain its localization momentum while outmaneuvering the looming specter of global mature-node overcapacity.

Presentation Download & Media Access

To dive deeper into the data and strategic frameworks discussed in this analysis:

* Click the PDF download link under “Related Topics” to access the presentation of this report.

* Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com