Spectral AI 2025 Financial Review: Bridging the Gap Between Government R&D and Commercial SaaS

Date : 2026-03-30

Reading : 330

For Spectral AI, Inc., fiscal 2025 represents a high-stakes inflection point. As the company transitions from a pre-commercialization entity heavily reliant on government R&D funding to a commercial enterprise, its strategic roadmap faces both unprecedented market-defining opportunities and stringent regulatory hurdles. HDIN Research’s in-depth analysis of Spectral AI’s 2025 annual disclosures reveals a company successfully leveraging non-dilutive government capital to build a deep technological moat, though its near-term financial viability remains inextricably tethered to its upcoming FDA De Novo authorization.

Figure Spectral Al (MDAl): Strategic Inflection and the Path to Commercialization (FY2025)

Financial Health & Capital Allocation Efficiency

Financial Health & Capital Allocation Efficiency

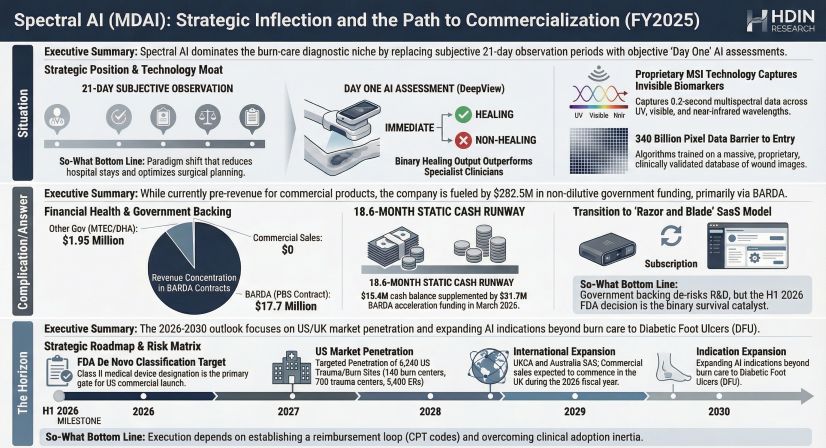

A surface-level reading of Spectral AI’s FY2025 income statement shows a 33.6% revenue contraction to $19.65 million and a 41.5% drop in total R&D expenditures. However, the strategic implication behind this data is not operational decay, but rather a cyclical transition. The revenue decline is primarily driven by the winding down of the base phase of its Project BioShield (PBS) BARDA contract, highlighting a high sensitivity to government procurement cycles.

While the company’s net loss narrowed significantly by 50.1% to $7.57 million, HDIN analysts caution against taking this metric at face value. This apparent improvement in capital efficiency was heavily distorted by a $3.2 million positive swing in non-cash, non-operating warrant liability fair value adjustments. Stripping away these non-cash gains, the company’s operating cash outflow actually increased by 7.8% to $9.92 million.

Despite an average monthly cash burn rate of approximately $827,000, Spectral AI has successfully padded its financial runway. A crucial $31.7 million contract modification advance from BARDA announced in March 2026—requiring a $9.7 million co-investment from the company—has substantially extended its liquidity, providing a vital bridge toward its commercialization targets.

Strategic Moats and the "Razor-and-Blade" SaaS Pivot

Spectral AI is engineering a highly sticky, mixed revenue model designed to shift the company away from its current 100% reliance on R&D grants. Post-commercialization, the company plans to deploy a "razor-and-blade" strategy:

* The Hardware Entry (Razor): Strategic placement of the proprietary DeepView SnapShot multi-spectral imaging (MSI) devices in emergency rooms, burn centers, and trauma clinics.

* Software as a Medical Device (Blade): A SaaS-driven recurring revenue stream capturing software licensing, image hosting, and continuous algorithm updates.

The company's ultimate strategic moat lies not just in its hardware, but in its data. Because core AI algorithms face patentability challenges, Spectral AI has fortified its competitive barrier through exclusive access to a proprietary, clinically validated database exceeding 340 billion pixels. This end-to-end controlled data ecosystem prevents potential disruptors from easily replicating its predictive accuracy.

Sector Positioning and Cyclical Headwinds

Within the AI medical diagnostic sector, Spectral AI possesses a distinct first-mover advantage, effectively operating without direct AI competitors in predictive burn management. Traditional burn assessment relies on subjective clinical observation requiring up to 21 days for an accurate prognosis. The DeepView system disrupts this standard of care by providing a "Day One" binary output (healing vs. non-healing) based on deep-tissue physiological biomarkers invisible to the naked eye.

However, this pioneering sector positioning is accompanied by severe cyclical headwinds. In FY2025, 90.1% of Spectral AI’s revenue was derived from a single customer: BARDA. This extreme customer concentration exposes the firm to macro-level federal budget shifts. Furthermore, commercializing a disruptive technology requires dismantling established clinical habits and securing complex medical reimbursement (CPT) codes—tasks for which the company currently lacks direct sales execution history.

HDIN Viewpoint: The Institutional Perspective

From an institutional advisory perspective, HDIN Research views Spectral AI's 2026 fiscal year as a binary event. The technological premise is highly compelling, validated by roughly $282.5 million in cumulative historical government funding and a successful UKCA mark acquisition. However, the transition from an R&D contractor to a SaaS-driven medical device manufacturer hinges entirely on securing FDA De Novo Class II clearance, anticipated in the first half of 2026.

Investors and stakeholders must closely monitor this regulatory timeline. Any friction in the FDA approval process will instantly amplify the company's financial risks, potentially triggering defaults on subsequent debt tranches. Additionally, HDIN Research advises monitoring the material weaknesses in internal controls acknowledged by management in the 2025 report—particularly regarding complex equity agreements and revenue recognition—as these factors require stringent governance overhauls as the company scales its commercial footprint.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research Profile:

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure Spectral Al (MDAl): Strategic Inflection and the Path to Commercialization (FY2025)

Financial Health & Capital Allocation EfficiencyA surface-level reading of Spectral AI’s FY2025 income statement shows a 33.6% revenue contraction to $19.65 million and a 41.5% drop in total R&D expenditures. However, the strategic implication behind this data is not operational decay, but rather a cyclical transition. The revenue decline is primarily driven by the winding down of the base phase of its Project BioShield (PBS) BARDA contract, highlighting a high sensitivity to government procurement cycles.

While the company’s net loss narrowed significantly by 50.1% to $7.57 million, HDIN analysts caution against taking this metric at face value. This apparent improvement in capital efficiency was heavily distorted by a $3.2 million positive swing in non-cash, non-operating warrant liability fair value adjustments. Stripping away these non-cash gains, the company’s operating cash outflow actually increased by 7.8% to $9.92 million.

Despite an average monthly cash burn rate of approximately $827,000, Spectral AI has successfully padded its financial runway. A crucial $31.7 million contract modification advance from BARDA announced in March 2026—requiring a $9.7 million co-investment from the company—has substantially extended its liquidity, providing a vital bridge toward its commercialization targets.

Strategic Moats and the "Razor-and-Blade" SaaS Pivot

Spectral AI is engineering a highly sticky, mixed revenue model designed to shift the company away from its current 100% reliance on R&D grants. Post-commercialization, the company plans to deploy a "razor-and-blade" strategy:

* The Hardware Entry (Razor): Strategic placement of the proprietary DeepView SnapShot multi-spectral imaging (MSI) devices in emergency rooms, burn centers, and trauma clinics.

* Software as a Medical Device (Blade): A SaaS-driven recurring revenue stream capturing software licensing, image hosting, and continuous algorithm updates.

The company's ultimate strategic moat lies not just in its hardware, but in its data. Because core AI algorithms face patentability challenges, Spectral AI has fortified its competitive barrier through exclusive access to a proprietary, clinically validated database exceeding 340 billion pixels. This end-to-end controlled data ecosystem prevents potential disruptors from easily replicating its predictive accuracy.

Sector Positioning and Cyclical Headwinds

Within the AI medical diagnostic sector, Spectral AI possesses a distinct first-mover advantage, effectively operating without direct AI competitors in predictive burn management. Traditional burn assessment relies on subjective clinical observation requiring up to 21 days for an accurate prognosis. The DeepView system disrupts this standard of care by providing a "Day One" binary output (healing vs. non-healing) based on deep-tissue physiological biomarkers invisible to the naked eye.

However, this pioneering sector positioning is accompanied by severe cyclical headwinds. In FY2025, 90.1% of Spectral AI’s revenue was derived from a single customer: BARDA. This extreme customer concentration exposes the firm to macro-level federal budget shifts. Furthermore, commercializing a disruptive technology requires dismantling established clinical habits and securing complex medical reimbursement (CPT) codes—tasks for which the company currently lacks direct sales execution history.

HDIN Viewpoint: The Institutional Perspective

From an institutional advisory perspective, HDIN Research views Spectral AI's 2026 fiscal year as a binary event. The technological premise is highly compelling, validated by roughly $282.5 million in cumulative historical government funding and a successful UKCA mark acquisition. However, the transition from an R&D contractor to a SaaS-driven medical device manufacturer hinges entirely on securing FDA De Novo Class II clearance, anticipated in the first half of 2026.

Investors and stakeholders must closely monitor this regulatory timeline. Any friction in the FDA approval process will instantly amplify the company's financial risks, potentially triggering defaults on subsequent debt tranches. Additionally, HDIN Research advises monitoring the material weaknesses in internal controls acknowledged by management in the 2025 report—particularly regarding complex equity agreements and revenue recognition—as these factors require stringent governance overhauls as the company scales its commercial footprint.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research Profile:

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com