OHB SE 2025 Annual Analysis: Breaking the Space Duopoly Amidst Working Capital Pressures

Date : 2026-03-31

Reading : 93

OHB SE’s fiscal year 2025 financial disclosures mark a definitive inflection point for the European aerospace sector. Surpassing internal targets, the company delivered $1.41 billion in total revenues—a 21.1% year-over-year surge—fueled by institutional budget expansions and strategic maneuverings within the European Space Agency (ESA). However, beneath a record-breaking $3.61 billion order backlog lies a complex financial narrative.

For institutional investors and industry stakeholders, the numbers dictate a shift in focus: OHB is no longer just a niche challenger but a Tier-1 Prime contractor. Yet, this aggressive expansion introduces critical questions regarding capital allocation efficiency and working capital conversion in an era of supply chain fragility.

Figure OHB SE 2025 Strategic Summary: Transitioning to European Tier-1 Space Leadership

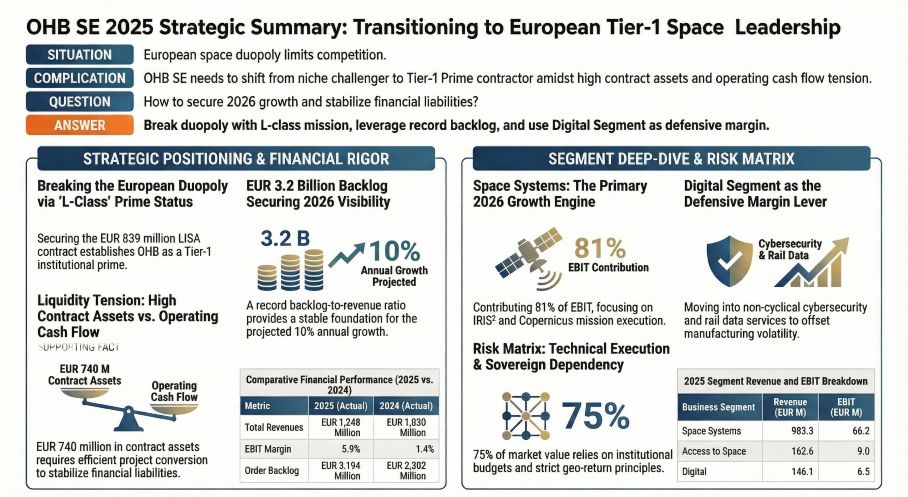

Sector Positioning: Breaking the European Duopoly

Sector Positioning: Breaking the European Duopoly

The strategic moat of OHB SE is deeply anchored in its ability to leverage ESA’s "Geo-return" principle. With Germany acting as the largest contributor to the record $22.3 billion ESA budget (accounting for 23.1%), OHB effectively captured domestic and regional tailwinds.

The structural implication here is profound. Historically, highly complex, budget-heavy "L-class" (Large-class) scientific missions were monopolized by the Airbus-Thales duopoly. In 2025, OHB successfully secured the $949 million primary contractor role for the LISA gravitational wave observatory. This milestone is not merely a revenue injection; it represents a permanent elevation in OHB’s technical sovereignty and project management credibility, securing its seat at the apex of the European space supply chain.

Financial Health & Capital Allocation Efficiency

While top-line growth is robust, a granular breakdown of OHB’s balance sheet reveals elevated liquidity absorption tied to long-cycle integration projects.

OHB utilizes the cost-to-cost method for revenue recognition. By the end of 2025, the company accumulated $740 million in contract assets—representing 41.8% of its total assets. This highlights a structural lag between recognized accounting profit and actual cash conversion. Consequently, while the EBIT margin rebounded to a normalized 5.9%, operating cash flow stood at only $43.5 million, lagging behind the $56.6 million net profit.

To finance these extended work-in-progress (WIP) cycles, OHB has had to lean on external financing, with financial liabilities escalating to $317 million. Moving forward, capital allocation efficiency will heavily depend on the successful on-orbit delivery of critical payloads (such as the Galileo and Copernicus satellites) to trigger milestone payments and deleverage the balance sheet.

Strategic Moats: Sovereign Security and Downstream Digitalization

OHB is actively recalibrating its business model to insulate against the disruptive pricing pressures of "NewSpace" competitors like SpaceX. The company has constructed a multi-layered defense mechanism:

* Sovereign Security Pivot: Unlike commercial satellite constellations that are highly sensitive to launch costs, 75% of OHB’s market value is derived from institutional clients prioritizing sovereign defense over cost-cutting. OHB is heavily entrenched in projects like the IRIS² secure communications constellation and the SARah radar reconnaissance system, shielding its core revenue from commercial market volatility.

* Downstream Digitalization: The *Digital* business segment, generating $165.2 million in 2025, acts as a high-margin counterbalance to hardware manufacturing. By securing recurring contracts for satellite data analysis, ground station operations, and cybersecurity for non-space clients like Deutsche Bahn (DB Netz AG), OHB is effectively establishing a less cyclical, software-driven revenue stream.

Cyclical Headwinds & Governance Structure

Despite an optimized market position, HDIN Research identifies two primary operational headwinds. First, global supply chain bottlenecks—specifically regarding critical electronic subsystems—continue to threaten project timelines and induce cost overruns. A $42.4 million provision recorded in 2024 for satellite anomalies serves as a stark reminder of the financial toll exacted by technical or supply chain missteps.

Second, the company’s ownership structure is highly centralized. The Fuchs family (65.35%) and KKR (28.64%) collectively control 92.02% of voting rights. While this ensures strategic continuity required for decades-long space programs, existing syndicate loan "change of control" covenants practically restrict the company from pursuing large-scale equity financing, potentially limiting aggressive M&A activities.

HDIN Viewpoint

The 2026 management guidance outlines an ambitious roadmap: projecting $1.58 billion in total revenue and an EBIT margin expansion to 8%. From the perspective of HDIN Research, this profitability jump is plausible but highly contingent on two catalysts: the realization of economies of scale in the Ariane 6 mass production phase (benefiting the *Access to Space* segment) and the accelerated scaling of the *Digital* segment.

OHB has successfully engineered the ultimate geopolitical moat in European aerospace. The primary mandate for 2026–2027 is no longer capturing market share, but operational execution—specifically, converting its massive $740 million in contract assets into operating cash flow before macroeconomic shifts threaten European sovereign defense budgets.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

For institutional investors and industry stakeholders, the numbers dictate a shift in focus: OHB is no longer just a niche challenger but a Tier-1 Prime contractor. Yet, this aggressive expansion introduces critical questions regarding capital allocation efficiency and working capital conversion in an era of supply chain fragility.

Figure OHB SE 2025 Strategic Summary: Transitioning to European Tier-1 Space Leadership

Sector Positioning: Breaking the European DuopolyThe strategic moat of OHB SE is deeply anchored in its ability to leverage ESA’s "Geo-return" principle. With Germany acting as the largest contributor to the record $22.3 billion ESA budget (accounting for 23.1%), OHB effectively captured domestic and regional tailwinds.

The structural implication here is profound. Historically, highly complex, budget-heavy "L-class" (Large-class) scientific missions were monopolized by the Airbus-Thales duopoly. In 2025, OHB successfully secured the $949 million primary contractor role for the LISA gravitational wave observatory. This milestone is not merely a revenue injection; it represents a permanent elevation in OHB’s technical sovereignty and project management credibility, securing its seat at the apex of the European space supply chain.

Financial Health & Capital Allocation Efficiency

While top-line growth is robust, a granular breakdown of OHB’s balance sheet reveals elevated liquidity absorption tied to long-cycle integration projects.

OHB utilizes the cost-to-cost method for revenue recognition. By the end of 2025, the company accumulated $740 million in contract assets—representing 41.8% of its total assets. This highlights a structural lag between recognized accounting profit and actual cash conversion. Consequently, while the EBIT margin rebounded to a normalized 5.9%, operating cash flow stood at only $43.5 million, lagging behind the $56.6 million net profit.

To finance these extended work-in-progress (WIP) cycles, OHB has had to lean on external financing, with financial liabilities escalating to $317 million. Moving forward, capital allocation efficiency will heavily depend on the successful on-orbit delivery of critical payloads (such as the Galileo and Copernicus satellites) to trigger milestone payments and deleverage the balance sheet.

Strategic Moats: Sovereign Security and Downstream Digitalization

OHB is actively recalibrating its business model to insulate against the disruptive pricing pressures of "NewSpace" competitors like SpaceX. The company has constructed a multi-layered defense mechanism:

* Sovereign Security Pivot: Unlike commercial satellite constellations that are highly sensitive to launch costs, 75% of OHB’s market value is derived from institutional clients prioritizing sovereign defense over cost-cutting. OHB is heavily entrenched in projects like the IRIS² secure communications constellation and the SARah radar reconnaissance system, shielding its core revenue from commercial market volatility.

* Downstream Digitalization: The *Digital* business segment, generating $165.2 million in 2025, acts as a high-margin counterbalance to hardware manufacturing. By securing recurring contracts for satellite data analysis, ground station operations, and cybersecurity for non-space clients like Deutsche Bahn (DB Netz AG), OHB is effectively establishing a less cyclical, software-driven revenue stream.

Cyclical Headwinds & Governance Structure

Despite an optimized market position, HDIN Research identifies two primary operational headwinds. First, global supply chain bottlenecks—specifically regarding critical electronic subsystems—continue to threaten project timelines and induce cost overruns. A $42.4 million provision recorded in 2024 for satellite anomalies serves as a stark reminder of the financial toll exacted by technical or supply chain missteps.

Second, the company’s ownership structure is highly centralized. The Fuchs family (65.35%) and KKR (28.64%) collectively control 92.02% of voting rights. While this ensures strategic continuity required for decades-long space programs, existing syndicate loan "change of control" covenants practically restrict the company from pursuing large-scale equity financing, potentially limiting aggressive M&A activities.

HDIN Viewpoint

The 2026 management guidance outlines an ambitious roadmap: projecting $1.58 billion in total revenue and an EBIT margin expansion to 8%. From the perspective of HDIN Research, this profitability jump is plausible but highly contingent on two catalysts: the realization of economies of scale in the Ariane 6 mass production phase (benefiting the *Access to Space* segment) and the accelerated scaling of the *Digital* segment.

OHB has successfully engineered the ultimate geopolitical moat in European aerospace. The primary mandate for 2026–2027 is no longer capturing market share, but operational execution—specifically, converting its massive $740 million in contract assets into operating cash flow before macroeconomic shifts threaten European sovereign defense budgets.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com