Beyond the Patent Cliff: How Global OTC & Consumer Health Giants Are Redefining Strategic Moats in 2025

Date : 2026-03-31

Reading : 191

The global Over-The-Counter (OTC) and consumer health landscape has permanently transitioned from an era of episodic, pandemic-driven windfalls to a highly contested battleground of chronic disease management and proactive wellness. Based on a penetrative audit of the 2025 annual reports of Tier-1 conglomerates—including Kenvue, Haleon, Reckitt, P&G, and Perrigo, alongside regional leaders like Kobayashi and Jiuzhitang—HDIN Research reveals a structural divergence in the market. The ultimate differentiator is no longer isolated patent monopolies, but rather a composite strategic moat defined by the triad of "Powerbrands, Healthcare Professional (HCP) Endorsement, and Supply Chain Scale."

Here is our in-depth analysis of the sector positioning, capital allocation efficiency, and cyclical headwinds shaping the global consumer health industry in 2025.

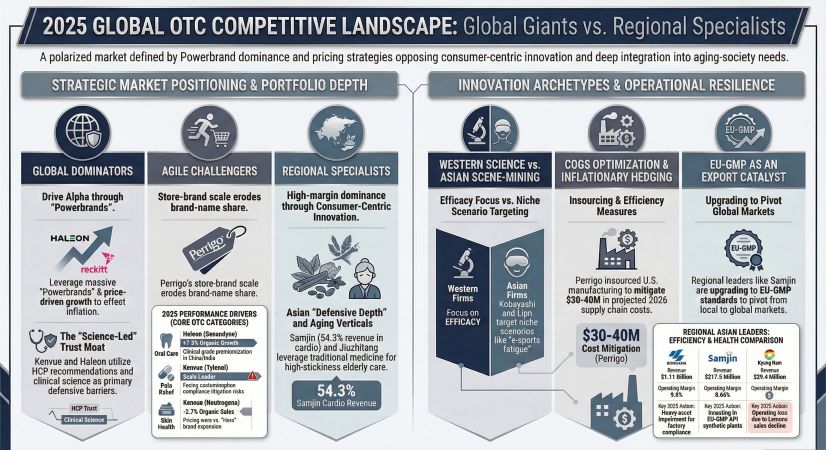

Figure 2025 GLOBAL OTC COMPETITIVE LANDSCAPE: Global Giants vs Regional Specialists

Strategic Moats: The Composite Wall of Trust and Pricing Power

Strategic Moats: The Composite Wall of Trust and Pricing Power

In an inflationary macroeconomic environment, brand equity translates directly into margin defense. Our analysis indicates that top-tier players are executing a strict "Powerbrand" focus to maintain capital allocation efficiency.

The "So What" factor here is pricing power: Haleon’s dominance in sensitivity toothpaste (Sensodyne) and Reckitt’s reliance on its 11 core brands grant them the elasticity to offset volatile raw material costs without suffering terminal volume loss. Furthermore, these consumer health giants are weaponizing HCP endorsements. Kenvue and Haleon treat pharmacy-channel expertise and doctor recommendations not merely as marketing channels, but as high-friction switching costs for consumers. When brand loyalty is anchored in scientific validation and clinical trust, it creates a defensive barrier that is exceedingly expensive for new entrants to replicate.

Sector Positioning: The Structural Pivot to Proactive Self-Care

The 2025 financial data exposes a unified structural pivot: consumer behavior has fundamentally shifted from "passive treatment" to "proactive defense."

This transition is not merely a consumer fad but a structural necessity. Driven by a projected global shortage of 18 million healthcare workers by 2030 and mounting public health insurance pressures, the medical system is actively forcing a shift toward self-care. Consequently, the Vitamins, Minerals, and Supplements (VMS) category has transcended seasonal volatility to become a daily necessity. Reckitt’s *Move Free* joint health portfolio surged by 64% in the Chinese market, while Haleon’s *Emergen-C* continues to capture structural growth in the US through immunity-boosting daily regimens.

Capital Allocation Efficiency: Formulation Over Pure Discovery

An analysis of R&D expenditures reveals a pragmatic shift in capital allocation. Instead of deploying capital toward high-risk, high-cost new Active Pharmaceutical Ingredient (API) discoveries, industry leaders are hyper-focusing on Drug Delivery Systems (DDS) and usage scenario enhancements.

The strategic implication is profound: navigating FDA monograph updates for new compounds is capital-intensive and slow. Instead, companies achieve premiumization through formulation upgrades. Haleon’s conversion of standard calcium into a high-bioavailability *Kids Liquid* formula, or Reckitt’s introduction of *Nurofen Mini* liquid capsules for faster onset, exemplifies this trend. By solving specific consumer pain points—such as difficulty in swallowing or the need for 12-hour sustained release—these companies are engineering premium product tiers that command price points 20% higher than generic equivalents.

Cyclical Headwinds: Regulatory Ceilings and Private Label Erosion

Despite robust top-line strategies, the industry faces severe cyclical headwinds and regulatory ceilings that threaten to compress historical margins.

1. The Regulatory Ceiling: Core API ingredients are facing an existential crisis. The FDA’s proposed removal of oral Phenylephrine (PE) due to efficacy concerns is restructuring the multi-hundred-million-dollar cold and flu market. Concurrently, Acetaminophen (the core ingredient in Kenvue’s *Tylenol*) faces looming litigation and potential FDA label changes regarding neurodevelopmental risks.

2. Private Label Cannibalization: Macroeconomic inflation has triggered a profound consumer downgrade in basic therapeutic categories. Perrigo, leveraging its position as the apex supplier of store brands to major retailers like Walmart, is executing a margin squeeze. By offering identical active ingredients at steep discounts, private labels are aggressively eroding the volume shares of legacy analgesic and digestive brands.

3. Geopolitical Supply Chain Risks: Heavy reliance on specific regions for APIs—such as the Middle East for Omeprazole—introduces asymmetric supply chain vulnerabilities that could trigger unexpected cost-of-goods-sold (COGS) spikes in the near term.

Financial Health: The Alpha Growth Divergence

The 2025 financial matrix highlights a stark divergence in earnings quality. Haleon and Reckitt successfully captured "Alpha growth" by pushing through price increases while maintaining volume stability via clinical-grade innovations (e.g., *Sensodyne Clinical White*). Conversely, Kenvue experienced organic sales contraction, indicating that excessive pricing strategies without concurrent formulation innovation can permanently damage brand volume.

Regionally, Asian leaders display unique defensive traits. Japan's Kobayashi Pharmaceutical demonstrated exceptional cash-flow resilience despite a massive 14.78 billion JPY impairment related to its Sendai facility, proving the inherent stability of its localized product matrix. In China, Jiuzhitang is aggressively circumventing the regulatory ceilings of Traditional Chinese Medicine (TCM) by acquiring peptide platforms, successfully crossing the chasm into high-barrier biologic therapies for cardiovascular and reproductive health.

HDIN Viewpoint

HDIN Research assesses that the post-pandemic consumer health market is a zero-sum game of habit monetization. The victors of the next half-decade will be those who successfully transition their portfolios from episodic sickness interventions to daily wellness regimens.

However, institutional investors must exercise heightened financial prudence. We advise strict scrutiny of Q4 Days Sales Outstanding (DSO) metrics among multinational players. In a weakening North American retail environment, sudden surges in late-year receivables disconnected from end-consumer demand are a classic red flag for channel stuffing. Capital should be allocated toward entities that demonstrate genuine formulation-driven pricing power and pristine cash-flow conversion.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Here is our in-depth analysis of the sector positioning, capital allocation efficiency, and cyclical headwinds shaping the global consumer health industry in 2025.

Figure 2025 GLOBAL OTC COMPETITIVE LANDSCAPE: Global Giants vs Regional Specialists

Strategic Moats: The Composite Wall of Trust and Pricing PowerIn an inflationary macroeconomic environment, brand equity translates directly into margin defense. Our analysis indicates that top-tier players are executing a strict "Powerbrand" focus to maintain capital allocation efficiency.

The "So What" factor here is pricing power: Haleon’s dominance in sensitivity toothpaste (Sensodyne) and Reckitt’s reliance on its 11 core brands grant them the elasticity to offset volatile raw material costs without suffering terminal volume loss. Furthermore, these consumer health giants are weaponizing HCP endorsements. Kenvue and Haleon treat pharmacy-channel expertise and doctor recommendations not merely as marketing channels, but as high-friction switching costs for consumers. When brand loyalty is anchored in scientific validation and clinical trust, it creates a defensive barrier that is exceedingly expensive for new entrants to replicate.

Sector Positioning: The Structural Pivot to Proactive Self-Care

The 2025 financial data exposes a unified structural pivot: consumer behavior has fundamentally shifted from "passive treatment" to "proactive defense."

This transition is not merely a consumer fad but a structural necessity. Driven by a projected global shortage of 18 million healthcare workers by 2030 and mounting public health insurance pressures, the medical system is actively forcing a shift toward self-care. Consequently, the Vitamins, Minerals, and Supplements (VMS) category has transcended seasonal volatility to become a daily necessity. Reckitt’s *Move Free* joint health portfolio surged by 64% in the Chinese market, while Haleon’s *Emergen-C* continues to capture structural growth in the US through immunity-boosting daily regimens.

Capital Allocation Efficiency: Formulation Over Pure Discovery

An analysis of R&D expenditures reveals a pragmatic shift in capital allocation. Instead of deploying capital toward high-risk, high-cost new Active Pharmaceutical Ingredient (API) discoveries, industry leaders are hyper-focusing on Drug Delivery Systems (DDS) and usage scenario enhancements.

The strategic implication is profound: navigating FDA monograph updates for new compounds is capital-intensive and slow. Instead, companies achieve premiumization through formulation upgrades. Haleon’s conversion of standard calcium into a high-bioavailability *Kids Liquid* formula, or Reckitt’s introduction of *Nurofen Mini* liquid capsules for faster onset, exemplifies this trend. By solving specific consumer pain points—such as difficulty in swallowing or the need for 12-hour sustained release—these companies are engineering premium product tiers that command price points 20% higher than generic equivalents.

Cyclical Headwinds: Regulatory Ceilings and Private Label Erosion

Despite robust top-line strategies, the industry faces severe cyclical headwinds and regulatory ceilings that threaten to compress historical margins.

1. The Regulatory Ceiling: Core API ingredients are facing an existential crisis. The FDA’s proposed removal of oral Phenylephrine (PE) due to efficacy concerns is restructuring the multi-hundred-million-dollar cold and flu market. Concurrently, Acetaminophen (the core ingredient in Kenvue’s *Tylenol*) faces looming litigation and potential FDA label changes regarding neurodevelopmental risks.

2. Private Label Cannibalization: Macroeconomic inflation has triggered a profound consumer downgrade in basic therapeutic categories. Perrigo, leveraging its position as the apex supplier of store brands to major retailers like Walmart, is executing a margin squeeze. By offering identical active ingredients at steep discounts, private labels are aggressively eroding the volume shares of legacy analgesic and digestive brands.

3. Geopolitical Supply Chain Risks: Heavy reliance on specific regions for APIs—such as the Middle East for Omeprazole—introduces asymmetric supply chain vulnerabilities that could trigger unexpected cost-of-goods-sold (COGS) spikes in the near term.

Financial Health: The Alpha Growth Divergence

The 2025 financial matrix highlights a stark divergence in earnings quality. Haleon and Reckitt successfully captured "Alpha growth" by pushing through price increases while maintaining volume stability via clinical-grade innovations (e.g., *Sensodyne Clinical White*). Conversely, Kenvue experienced organic sales contraction, indicating that excessive pricing strategies without concurrent formulation innovation can permanently damage brand volume.

Regionally, Asian leaders display unique defensive traits. Japan's Kobayashi Pharmaceutical demonstrated exceptional cash-flow resilience despite a massive 14.78 billion JPY impairment related to its Sendai facility, proving the inherent stability of its localized product matrix. In China, Jiuzhitang is aggressively circumventing the regulatory ceilings of Traditional Chinese Medicine (TCM) by acquiring peptide platforms, successfully crossing the chasm into high-barrier biologic therapies for cardiovascular and reproductive health.

HDIN Viewpoint

HDIN Research assesses that the post-pandemic consumer health market is a zero-sum game of habit monetization. The victors of the next half-decade will be those who successfully transition their portfolios from episodic sickness interventions to daily wellness regimens.

However, institutional investors must exercise heightened financial prudence. We advise strict scrutiny of Q4 Days Sales Outstanding (DSO) metrics among multinational players. In a weakening North American retail environment, sudden surges in late-year receivables disconnected from end-consumer demand are a classic red flag for channel stuffing. Capital should be allocated toward entities that demonstrate genuine formulation-driven pricing power and pristine cash-flow conversion.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com