2025 Global Veterinary Drug Market Analysis: Strategic Moats, Biologics Pivot, and Value Chain Polarization

Date : 2026-03-31

Reading : 381

The global veterinary drug industry in 2025 has officially transitioned from broad-based volume expansion into an era of structural optimization. Based on an in-depth financial and operational audit of nine global leaders—including Zoetis, Merck, Boehringer Ingelheim (BI), Elanco, and Guobang Pharma—HDIN Research notes a profound market polarization. Driven by the irreversible macroeconomic trend of "Pet Humanization," tier-one pharmaceutical giants are aggressively rotating capital toward high-margin biologics and chronic care. Conversely, the livestock sector is facing severe cyclical headwinds dictated by stringent antimicrobial resistance (AMR) regulations and escalating ESG compliance costs.

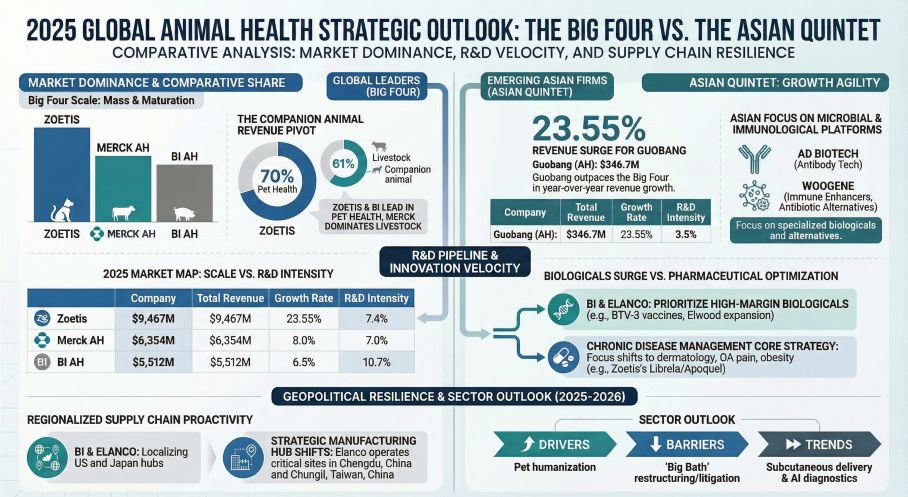

Figure 2025 GLOBAL ANIMAL HEALTH STRATEGIC OUTLOOK: THE BIG FOUR VS THE ASIAN QUINTET

Pet Humanization Drives Biologics and Chronic Care Premiums

Pet Humanization Drives Biologics and Chronic Care Premiums

The strategic implication behind 2025's revenue data is clear: companion animal portfolios are providing the ultimate anti-cyclical buffer. Zoetis now derives approximately 70% of its $9.46 billion revenue from the companion animal segment, demonstrating massive margin resilience. The growth engine has fundamentally shifted from basic immunization to preventative care and chronic disease management.

This pivot is spearheaded by next-generation parasiticides and dermatological treatments. Boehringer Ingelheim’s NexGard® franchise generated €1.40 billion ($1.58 billion), anchoring its animal health division, while Merck’s Bravecto® surpassed $1.1 billion. More importantly, the rapid penetration of monoclonal antibodies (mAbs), such as Zoetis’s Apoquel®, Cytopoint®, and osteoarthritis treatments Librela® and Solensia®, indicates an industry-wide elevation in pricing power. These biologics represent highly fortified technological moats that limit the threat of reverse engineering from generic competitors.

Strategic Moats: Lifecycle Management and the "Patent Cliff"

As the industry approaches a critical "patent cliff" window between 2025 and 2028, leading firms are executing sophisticated Lifecycle Management (LCM) strategies to defend their intellectual property. The defense mechanisms are threefold:

* Formulation Complexity: Shifting from single-agent drugs to complex combinations. For instance, Zoetis's Simparica Trio and Elanco’s Credelio Quattro (a four-in-one chewable) create physical and chemical stability hurdles that delay generic entry and increase clinical premium.

* Long-Acting Modalities: Merck’s introduction of the Bravecto Quantum (an annual injectable) aims to elevate the competitive dimension from oral chemical formulations to high-barrier biological injections, effectively neutralizing upcoming generic oral alternatives.

* Omnichannel Lock-in: Top-tier companies are decoupling from exclusive veterinary clinic reliance, deeply integrating with retail and e-commerce giants to secure distribution stickiness.

Capital Allocation Efficiency and Value Chain Polarization

A forensic analysis of capital allocation reveals stark divergences in financial health and sector positioning across the global value chain.

On one end of the spectrum, cash-cow operators like Zoetis maintain operating margins above 35% through brand equity and patent monopolies. However, aggressive M&A strategies have triggered financial turbulence for others. Elanco recorded a $232 million net loss in 2025, heavily weighed down by $1.55 million in restructuring fees and intangible asset impairments. While operating cash flow remains stable, this "big bath" accounting signals immense pressure to digest historical acquisition premiums while refocusing capital expenditure (CAPEX) onto mAb manufacturing facilities.

On the other end of the value chain sits the API (Active Pharmaceutical Ingredient) cost-leader paradigm, epitomized by China’s Guobang Pharma. As the indispensable "platform manufacturer" supplying global giants, Guobang operates with an ultra-conservative 22.1% debt-to-asset ratio. By controlling the upstream supply of core intermediates (e.g., florfenicol and doxycycline), Guobang mitigates end-market volatility. However, with an animal health gross margin of 23.19% compared to Zoetis's ~71.8%, API suppliers must continuously fight for pricing leverage against consolidated downstream buyers.

Cyclical Headwinds: Regulatory Pressures and ESG Compliance

Growth in the livestock segment is being structurally suppressed by legislative ceilings. The European Union's ban on prophylactic antibiotics in feed, with Vietnam implementing similar restrictions by 2026, has forced a rapid "de-antibiotic" shakeout. This directly correlates with Zoetis’s 5% year-over-year decline in its livestock segment.

Furthermore, ESG compliance has transitioned from a corporate PR exercise to a hard operational cost. Merck’s mandate to achieve net-zero across its entire Scope 1-3 supply chain by 2045, alongside BI’s massive investments in carbon-neutral facilities, means that upstream suppliers will soon face prohibitive environmental entry barriers.

HDIN Viewpoint

HDIN Research anticipates that the next 12 to 18 months will be defined by an intense tug-of-war between "consolidation" and "substitution." Global incumbents will leverage M&A—such as Merck’s $1.29 billion cash acquisition of Elanco’s aqua business—to widen their moats and monopolize niche sectors. Meanwhile, regional players will attempt flank attacks. We are observing South Korean biotech firms bypassing traditional chemical pathways entirely, opting instead to develop novel IgY (yolk antibody) platforms and stem-cell therapies to capture specialized market premiums.

For institutional investors and supply chain strategists, the key performance indicator moving into 2026 is no longer mere top-line growth, but the ability to successfully execute biological pivots while absorbing the escalating marginal costs of regulatory compliance.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure 2025 GLOBAL ANIMAL HEALTH STRATEGIC OUTLOOK: THE BIG FOUR VS THE ASIAN QUINTET

Pet Humanization Drives Biologics and Chronic Care PremiumsThe strategic implication behind 2025's revenue data is clear: companion animal portfolios are providing the ultimate anti-cyclical buffer. Zoetis now derives approximately 70% of its $9.46 billion revenue from the companion animal segment, demonstrating massive margin resilience. The growth engine has fundamentally shifted from basic immunization to preventative care and chronic disease management.

This pivot is spearheaded by next-generation parasiticides and dermatological treatments. Boehringer Ingelheim’s NexGard® franchise generated €1.40 billion ($1.58 billion), anchoring its animal health division, while Merck’s Bravecto® surpassed $1.1 billion. More importantly, the rapid penetration of monoclonal antibodies (mAbs), such as Zoetis’s Apoquel®, Cytopoint®, and osteoarthritis treatments Librela® and Solensia®, indicates an industry-wide elevation in pricing power. These biologics represent highly fortified technological moats that limit the threat of reverse engineering from generic competitors.

Strategic Moats: Lifecycle Management and the "Patent Cliff"

As the industry approaches a critical "patent cliff" window between 2025 and 2028, leading firms are executing sophisticated Lifecycle Management (LCM) strategies to defend their intellectual property. The defense mechanisms are threefold:

* Formulation Complexity: Shifting from single-agent drugs to complex combinations. For instance, Zoetis's Simparica Trio and Elanco’s Credelio Quattro (a four-in-one chewable) create physical and chemical stability hurdles that delay generic entry and increase clinical premium.

* Long-Acting Modalities: Merck’s introduction of the Bravecto Quantum (an annual injectable) aims to elevate the competitive dimension from oral chemical formulations to high-barrier biological injections, effectively neutralizing upcoming generic oral alternatives.

* Omnichannel Lock-in: Top-tier companies are decoupling from exclusive veterinary clinic reliance, deeply integrating with retail and e-commerce giants to secure distribution stickiness.

Capital Allocation Efficiency and Value Chain Polarization

A forensic analysis of capital allocation reveals stark divergences in financial health and sector positioning across the global value chain.

On one end of the spectrum, cash-cow operators like Zoetis maintain operating margins above 35% through brand equity and patent monopolies. However, aggressive M&A strategies have triggered financial turbulence for others. Elanco recorded a $232 million net loss in 2025, heavily weighed down by $1.55 million in restructuring fees and intangible asset impairments. While operating cash flow remains stable, this "big bath" accounting signals immense pressure to digest historical acquisition premiums while refocusing capital expenditure (CAPEX) onto mAb manufacturing facilities.

On the other end of the value chain sits the API (Active Pharmaceutical Ingredient) cost-leader paradigm, epitomized by China’s Guobang Pharma. As the indispensable "platform manufacturer" supplying global giants, Guobang operates with an ultra-conservative 22.1% debt-to-asset ratio. By controlling the upstream supply of core intermediates (e.g., florfenicol and doxycycline), Guobang mitigates end-market volatility. However, with an animal health gross margin of 23.19% compared to Zoetis's ~71.8%, API suppliers must continuously fight for pricing leverage against consolidated downstream buyers.

Cyclical Headwinds: Regulatory Pressures and ESG Compliance

Growth in the livestock segment is being structurally suppressed by legislative ceilings. The European Union's ban on prophylactic antibiotics in feed, with Vietnam implementing similar restrictions by 2026, has forced a rapid "de-antibiotic" shakeout. This directly correlates with Zoetis’s 5% year-over-year decline in its livestock segment.

Furthermore, ESG compliance has transitioned from a corporate PR exercise to a hard operational cost. Merck’s mandate to achieve net-zero across its entire Scope 1-3 supply chain by 2045, alongside BI’s massive investments in carbon-neutral facilities, means that upstream suppliers will soon face prohibitive environmental entry barriers.

HDIN Viewpoint

HDIN Research anticipates that the next 12 to 18 months will be defined by an intense tug-of-war between "consolidation" and "substitution." Global incumbents will leverage M&A—such as Merck’s $1.29 billion cash acquisition of Elanco’s aqua business—to widen their moats and monopolize niche sectors. Meanwhile, regional players will attempt flank attacks. We are observing South Korean biotech firms bypassing traditional chemical pathways entirely, opting instead to develop novel IgY (yolk antibody) platforms and stem-cell therapies to capture specialized market premiums.

For institutional investors and supply chain strategists, the key performance indicator moving into 2026 is no longer mere top-line growth, but the ability to successfully execute biological pivots while absorbing the escalating marginal costs of regulatory compliance.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com