Global Brokerage 2025 Strategic Divergence: US Wealth Moats, China’s IB Pivot, and Korea’s Digital Arbitrage

Date : 2026-03-31

Reading : 151

In 2025, the global brokerage landscape fundamentally bifurcated as top-tier institutions navigated pronounced macroeconomic volatility and geopolitical realignments. Rather than pursuing uniform scale, the world's leading financial institutions optimized their operating models to capture distinct alpha. Based on the latest financial disclosures, HDIN Research has identified three divergent evolutionary paths: US titans are insulating themselves from cyclical headwinds through highly valued, fee-based wealth management moats; Chinese market leaders are prioritizing structural sector positioning to fund the real economy via "Investment Banking + Investment" synergies; and Korean challengers are executing aggressive digital arbitrage to capture emerging market growth.

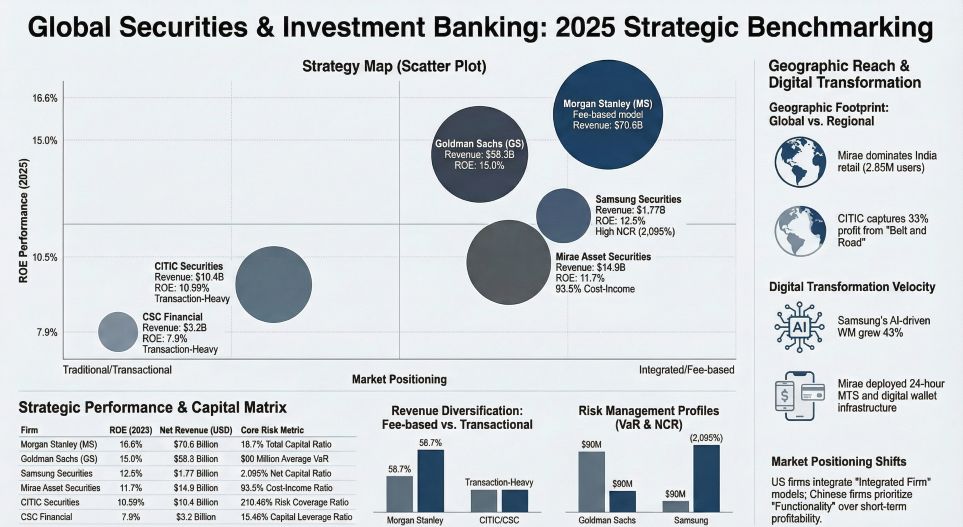

Figure Global Securities & Investment Banking: 2025 Strategic Benchmarking

Strategic Moats: The Wealth and Asset Management Imperative

Strategic Moats: The Wealth and Asset Management Imperative

The transition from high-beta trading revenue to stable, recurring fee-based income has become the ultimate determinant of valuation premiums in 2025.

Morgan Stanley (MS) has established the global gold standard for this transition. Generating $70.64 billion in total net revenues, its Wealth Management division contributed 45% ($31.75 billion). More crucially, 58.7% of this wealth revenue stems from asset-based fees rather than transactional commissions. This recurring revenue model effectively smooths the cyclical volatility of traditional investment banking, granting the firm a superior return on equity (ROE) of 16.6% and robust capital allocation efficiency.

Similarly, Goldman Sachs (GS) is strategically retreating from high-friction consumer banking to reinforce its core institutional prowess, aggressively expanding its Alternative Assets Under Supervision (AUS) to $420 billion. By contrast, while Chinese brokerages like CITIC Securities command massive client bases (over 17 million) and a formidable $2.08 trillion in custody assets, their revenue models remain heavily reliant on trading commissions. However, they are rapidly closing the gap by capturing secular growth in the pension sector, establishing a new runway for long-term capital accumulation.

Sector Positioning: China’s "IB + Investment" Synergy

In the investment banking arena, the revenue generation models highlight stark regional mandates. US banks capture outsized margins through global M&A advisory, with Goldman Sachs deriving over 50% of its IB net revenues from its elite advisory brand premium.

Conversely, Chinese brokerages exhibit a "functionality over profitability" mandate, channeling capital toward strategic "New Productive Forces." CITIC Securities and CSC Financial dominate the underwriting volume in China's technology boards. Instead of relying on advisory fees, they have constructed a closed-loop "IB + Investment" ecosystem. By utilizing subsidiary direct investment (PE/VC) to co-invest alongside their underwriting projects, these firms provide full-lifecycle funding for hard-tech enterprises. This strategic sector positioning yielded a staggering 41.4% net profit margin for CITIC Securities ($4.18 billion net profit on $10.41 billion revenue), demonstrating immense domestic pricing power and structural resilience.

Capital Allocation Efficiency: Operating Leverage and Digitalization

A comparative analysis of human capital efficiency reveals profound differences in global incentive structures. Goldman Sachs leads the cohort in profit per employee (PPE) at $362,400, but relies on a high-leverage compensation model where the compensation-to-profit ratio stands at a costly 1.10.

Korean brokerages, however, represent the pinnacle of cost efficiency. Mirae Asset Securities achieved a remarkably low compensation-to-profit ratio of 0.34, driven by its "Mirae Asset 3.0" strategy. By transforming its mobile trading systems (MTS) into highly automated digital wallet infrastructures, Mirae drastically diluted middle- and back-office human capital costs. Samsung Securities mirrored this success, utilizing AI-driven Robo-advisors to grow its ultra-high-net-worth individual (UHNWI) base by over 51%, proving that digital transformation is a tangible driver of margin expansion, not just corporate rhetoric.

Cyclical Headwinds and Risk Management Divergence

As the market prepares for a complex 2026, risk management architectures have shifted from mere compliance to active capital deployment strategies.

US institutions operate on a "Model-Driven" high-leverage market-making framework. Goldman Sachs maintains a leverage multiple (trading assets to equity) of 5.61x, utilizing complex OTC derivatives to hedge massive risk exposures. Meanwhile, Chinese firms operate a "Compliance-Driven" model. CITIC Securities maintains a conservative 1.51x leverage ratio and a massive 210.46% risk coverage ratio, reflecting a balance sheet utilized for holding strategic assets rather than high-frequency liquidity provision.

Geopolitically, the institutions are actively hedging against fragmentation. While US brokerages build capital buffers against potential Asia-Pacific supply chain disruptions, CITIC Securities is advancing a "One Firm" global configuration. Generating 33.3% of its net profit off-shore, primarily through CLSA, CITIC is cementing its financial infrastructure across Belt and Road and Middle Eastern corridors, moving from simple overseas outposts to genuine global resource allocation.

The HDIN Viewpoint

HDIN Research observes that while top-tier brokerages display exceptional capital adequacy, investors must scrutinize the underlying quality of their earnings. Morgan Stanley’s "Integrated Firm" model clearly provides the most defensive revenue moat against global cyclical headwinds. However, we urge institutional investors to remain vigilant on two fronts: First, the valuation opacity of Level 3 financial instruments embedded within the US banks' massive derivative liabilities. Second, the potential for cross-period profit management via Expected Credit Loss (ECL) provisions among Chinese and Korean brokerages as they aggressively expand into emerging tech sectors and high-interest overseas markets. Moving forward, the true winners will be those who can seamlessly translate balance sheet scale into sustainable, fee-based ROE.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure Global Securities & Investment Banking: 2025 Strategic Benchmarking

Strategic Moats: The Wealth and Asset Management ImperativeThe transition from high-beta trading revenue to stable, recurring fee-based income has become the ultimate determinant of valuation premiums in 2025.

Morgan Stanley (MS) has established the global gold standard for this transition. Generating $70.64 billion in total net revenues, its Wealth Management division contributed 45% ($31.75 billion). More crucially, 58.7% of this wealth revenue stems from asset-based fees rather than transactional commissions. This recurring revenue model effectively smooths the cyclical volatility of traditional investment banking, granting the firm a superior return on equity (ROE) of 16.6% and robust capital allocation efficiency.

Similarly, Goldman Sachs (GS) is strategically retreating from high-friction consumer banking to reinforce its core institutional prowess, aggressively expanding its Alternative Assets Under Supervision (AUS) to $420 billion. By contrast, while Chinese brokerages like CITIC Securities command massive client bases (over 17 million) and a formidable $2.08 trillion in custody assets, their revenue models remain heavily reliant on trading commissions. However, they are rapidly closing the gap by capturing secular growth in the pension sector, establishing a new runway for long-term capital accumulation.

Sector Positioning: China’s "IB + Investment" Synergy

In the investment banking arena, the revenue generation models highlight stark regional mandates. US banks capture outsized margins through global M&A advisory, with Goldman Sachs deriving over 50% of its IB net revenues from its elite advisory brand premium.

Conversely, Chinese brokerages exhibit a "functionality over profitability" mandate, channeling capital toward strategic "New Productive Forces." CITIC Securities and CSC Financial dominate the underwriting volume in China's technology boards. Instead of relying on advisory fees, they have constructed a closed-loop "IB + Investment" ecosystem. By utilizing subsidiary direct investment (PE/VC) to co-invest alongside their underwriting projects, these firms provide full-lifecycle funding for hard-tech enterprises. This strategic sector positioning yielded a staggering 41.4% net profit margin for CITIC Securities ($4.18 billion net profit on $10.41 billion revenue), demonstrating immense domestic pricing power and structural resilience.

Capital Allocation Efficiency: Operating Leverage and Digitalization

A comparative analysis of human capital efficiency reveals profound differences in global incentive structures. Goldman Sachs leads the cohort in profit per employee (PPE) at $362,400, but relies on a high-leverage compensation model where the compensation-to-profit ratio stands at a costly 1.10.

Korean brokerages, however, represent the pinnacle of cost efficiency. Mirae Asset Securities achieved a remarkably low compensation-to-profit ratio of 0.34, driven by its "Mirae Asset 3.0" strategy. By transforming its mobile trading systems (MTS) into highly automated digital wallet infrastructures, Mirae drastically diluted middle- and back-office human capital costs. Samsung Securities mirrored this success, utilizing AI-driven Robo-advisors to grow its ultra-high-net-worth individual (UHNWI) base by over 51%, proving that digital transformation is a tangible driver of margin expansion, not just corporate rhetoric.

Cyclical Headwinds and Risk Management Divergence

As the market prepares for a complex 2026, risk management architectures have shifted from mere compliance to active capital deployment strategies.

US institutions operate on a "Model-Driven" high-leverage market-making framework. Goldman Sachs maintains a leverage multiple (trading assets to equity) of 5.61x, utilizing complex OTC derivatives to hedge massive risk exposures. Meanwhile, Chinese firms operate a "Compliance-Driven" model. CITIC Securities maintains a conservative 1.51x leverage ratio and a massive 210.46% risk coverage ratio, reflecting a balance sheet utilized for holding strategic assets rather than high-frequency liquidity provision.

Geopolitically, the institutions are actively hedging against fragmentation. While US brokerages build capital buffers against potential Asia-Pacific supply chain disruptions, CITIC Securities is advancing a "One Firm" global configuration. Generating 33.3% of its net profit off-shore, primarily through CLSA, CITIC is cementing its financial infrastructure across Belt and Road and Middle Eastern corridors, moving from simple overseas outposts to genuine global resource allocation.

The HDIN Viewpoint

HDIN Research observes that while top-tier brokerages display exceptional capital adequacy, investors must scrutinize the underlying quality of their earnings. Morgan Stanley’s "Integrated Firm" model clearly provides the most defensive revenue moat against global cyclical headwinds. However, we urge institutional investors to remain vigilant on two fronts: First, the valuation opacity of Level 3 financial instruments embedded within the US banks' massive derivative liabilities. Second, the potential for cross-period profit management via Expected Credit Loss (ECL) provisions among Chinese and Korean brokerages as they aggressively expand into emerging tech sectors and high-interest overseas markets. Moving forward, the true winners will be those who can seamlessly translate balance sheet scale into sustainable, fee-based ROE.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com