Fresenius Medical Care Accelerates Value-Based Care Integration as Weigao’s Hemodialysis Margins Compress to 40.5% in FY2025

Date : 2026-04-01

Reading : 174

In FY2025, global hemodialysis leaders Fresenius (NYSE: FMS) and Weigao restructured supply chains across the US and China. Deploying HVHDF technology and localized manufacturing to counter Medicare's rigid 2.1% rate hike and China’s Volume-Based Procurement (VBP), the sector has definitively shifted from hardware distribution to value-based risk management.

Financial Health & Operational Moats: The CapEx Rotation to Digital Yield

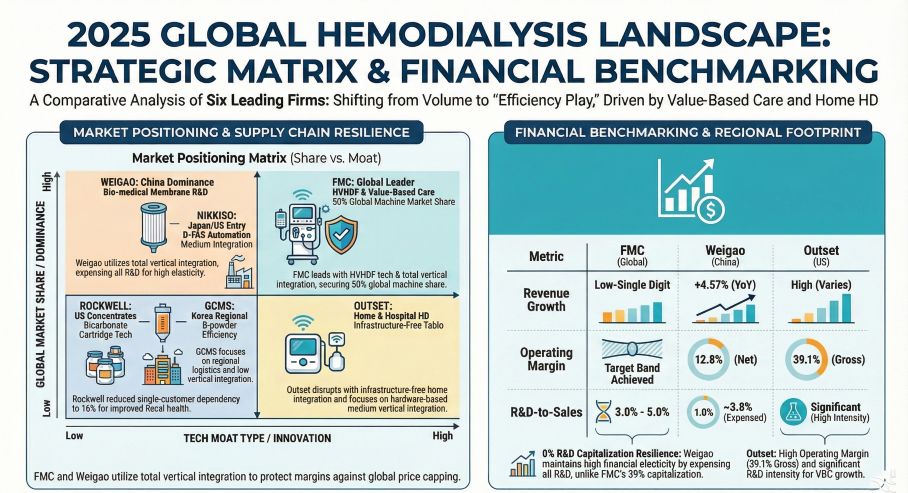

The transition sweeping the hemodialysis sector is not merely a clinical upgrade; it is a forced financial restructuring. With the US Medicare ESRD PPS baseline rate capped at a stagnant 2.1% increase for 2026, traditional cost-pass-through mechanisms for inflation are effectively broken. Fresenius Medical Care (NYSE: FMS) reacted by generating $2.54 billion in Value-Based Care (VBC) revenue (+34% YoY in constant currency), converting clinical risk management directly into operational yield. However, FMC elevated its R&D capitalization rate to an aggressive 39% (capitalizing ~$102 million), smoothing its income statement ahead of the commercial rollout of the FDA-cleared 5008X CAREsystem.

Conversely, Weigao Blood Purification absorbed China’s VBP-induced margin compression—with gross margins dropping 2.18% to 40.55%—through ruthless vertical integration. By expensing 100% of its R&D and generating $110.4 million in operating cash flow, Weigao bypasses the earnings management trap seen in Western peers. Their strategic CapEx focus on the Weihai Phase VI plant (99.25% complete) signals a tactical pivot from defending unit gross margins to securing absolute volume dominance.

Meanwhile, Rockwell Medical (NASDAQ: RMTI) navigated a brutal inventory de-stocking cycle, reducing its historic revenue reliance on DaVita from 45% down to 16%, yet managing to defend a 16.9% gross margin through hyper-specialized concentrate logistics and its new single-use bicarbonate cartridges.

Supply Chain Pivot: Geopolitical De-Risking and Localization

The era of unfettered, globalized medical device shipping is over. Outset Medical (NASDAQ: OM) currently faces acute geographic vulnerability. Highly dependent on its Tijuana, Mexico manufacturing facility and a fragmented web of global PCBA (Printed Circuit Board Assembly) suppliers, Outset’s recently improved 39.1% gross margin remains directly exposed to North American tariff volatility.

To insulate themselves, international incumbents are executing extreme localization strategies. FMC mitigates border friction through a robust multi-source framework, leveraging its Changshu, China facility to directly satisfy Beijing's domestic production mandates while retaining its St. Wendel, Germany plant for core dialyzer membrane IP.

Nikkiso (TYO: 6436) executed the most aggressive geopolitical hedge via an equity joint venture. By establishing Weigao Nikkiso (Weihai) Dialysis Equipment Co., Ltd. (Weigao 51%, Nikkiso 49%), Nikkiso stripped away its foreign entity risk. Manufacturing the DBB-EXA ESS system domestically allows Nikkiso's automation technology to participate in Chinese hospital tenders as a de facto national brand, rendering VBP exclusion risks obsolete.

Figure 2025 CLOBAL HEMODIALYSIS LANDSCAPE

HDIN Institutional Perspective: The "Service-as-a-Product" Trough

HDIN Institutional Perspective: The "Service-as-a-Product" Trough

The hemodialysis sector is currently scraping a cyclical trough in hardware profitability but peaking in service monetization. The structural headwind isn't solely the rise of GLP-1 receptor agonists delaying end-stage renal disease (ESRD) progression; it is the unsustainable capital intensity of clinic infrastructure.

Outset's Tablo system—coupled with the TabloDash data platform that captures 3 million telemetry points per treatment—aims to dismantle this centralized clinic dependence. Yet, operating with a -50.0% EBITDA margin, Outset is racing against its own cash burn to achieve critical mass in the home-hemodialysis (Home HD) market before funding constraints choke its CapEx.

The ultimate institutional moat now belongs to entities managing the patient outcome data, not just the consumable flow. FMC's deployment of AI via AskHUGO to accelerate HVHDF adoption proves that future accretive acquisitions in this space will target software architecture and VBC patient lives, rather than legacy membrane manufacturing capacity. The divergence is clear: hardware without software-driven risk-sharing is a depreciating asset.

Related Topics & Resources

* Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

* Video Link: Click this link to watch the YouTube video.

About HDIN Research

HDIN Research is a premier market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain auditing, and geopolitical risk assessment within the global healthcare and medical device sectors. (www.hdinresearch.com)

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*

Financial Health & Operational Moats: The CapEx Rotation to Digital Yield

The transition sweeping the hemodialysis sector is not merely a clinical upgrade; it is a forced financial restructuring. With the US Medicare ESRD PPS baseline rate capped at a stagnant 2.1% increase for 2026, traditional cost-pass-through mechanisms for inflation are effectively broken. Fresenius Medical Care (NYSE: FMS) reacted by generating $2.54 billion in Value-Based Care (VBC) revenue (+34% YoY in constant currency), converting clinical risk management directly into operational yield. However, FMC elevated its R&D capitalization rate to an aggressive 39% (capitalizing ~$102 million), smoothing its income statement ahead of the commercial rollout of the FDA-cleared 5008X CAREsystem.

Conversely, Weigao Blood Purification absorbed China’s VBP-induced margin compression—with gross margins dropping 2.18% to 40.55%—through ruthless vertical integration. By expensing 100% of its R&D and generating $110.4 million in operating cash flow, Weigao bypasses the earnings management trap seen in Western peers. Their strategic CapEx focus on the Weihai Phase VI plant (99.25% complete) signals a tactical pivot from defending unit gross margins to securing absolute volume dominance.

Meanwhile, Rockwell Medical (NASDAQ: RMTI) navigated a brutal inventory de-stocking cycle, reducing its historic revenue reliance on DaVita from 45% down to 16%, yet managing to defend a 16.9% gross margin through hyper-specialized concentrate logistics and its new single-use bicarbonate cartridges.

Supply Chain Pivot: Geopolitical De-Risking and Localization

The era of unfettered, globalized medical device shipping is over. Outset Medical (NASDAQ: OM) currently faces acute geographic vulnerability. Highly dependent on its Tijuana, Mexico manufacturing facility and a fragmented web of global PCBA (Printed Circuit Board Assembly) suppliers, Outset’s recently improved 39.1% gross margin remains directly exposed to North American tariff volatility.

To insulate themselves, international incumbents are executing extreme localization strategies. FMC mitigates border friction through a robust multi-source framework, leveraging its Changshu, China facility to directly satisfy Beijing's domestic production mandates while retaining its St. Wendel, Germany plant for core dialyzer membrane IP.

Nikkiso (TYO: 6436) executed the most aggressive geopolitical hedge via an equity joint venture. By establishing Weigao Nikkiso (Weihai) Dialysis Equipment Co., Ltd. (Weigao 51%, Nikkiso 49%), Nikkiso stripped away its foreign entity risk. Manufacturing the DBB-EXA ESS system domestically allows Nikkiso's automation technology to participate in Chinese hospital tenders as a de facto national brand, rendering VBP exclusion risks obsolete.

Figure 2025 CLOBAL HEMODIALYSIS LANDSCAPE

HDIN Institutional Perspective: The "Service-as-a-Product" TroughThe hemodialysis sector is currently scraping a cyclical trough in hardware profitability but peaking in service monetization. The structural headwind isn't solely the rise of GLP-1 receptor agonists delaying end-stage renal disease (ESRD) progression; it is the unsustainable capital intensity of clinic infrastructure.

Outset's Tablo system—coupled with the TabloDash data platform that captures 3 million telemetry points per treatment—aims to dismantle this centralized clinic dependence. Yet, operating with a -50.0% EBITDA margin, Outset is racing against its own cash burn to achieve critical mass in the home-hemodialysis (Home HD) market before funding constraints choke its CapEx.

The ultimate institutional moat now belongs to entities managing the patient outcome data, not just the consumable flow. FMC's deployment of AI via AskHUGO to accelerate HVHDF adoption proves that future accretive acquisitions in this space will target software architecture and VBC patient lives, rather than legacy membrane manufacturing capacity. The divergence is clear: hardware without software-driven risk-sharing is a depreciating asset.

Related Topics & Resources

* Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

* Video Link: Click this link to watch the YouTube video.

About HDIN Research

HDIN Research is a premier market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain auditing, and geopolitical risk assessment within the global healthcare and medical device sectors. (www.hdinresearch.com)

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*