SMIC Surpasses $9.36B Revenue as GlobalFoundries Battles 10.4% ASP Compression Amid 2025 Subsidy-Driven Capacity Glut

Date : 2026-04-01

Reading : 1813

In FY2025, top-tier foundries including SMIC and GlobalFoundries drove a K-shaped global recovery. SMIC aggressively scaled 12-inch capacities across China to secure $9.36 billion in revenue, while GlobalFoundries leveraged US subsidies to defend against localized overcapacity and severe geopolitical supply chain fragmentation.

Figure 2025 Global Foundry Benchmark: Scale, Moats, and the K-Shaped Recovery

Financial Health & Operational Moats: The Depreciation Distortion

Financial Health & Operational Moats: The Depreciation Distortion

A rigorous audit of 2025 annual filings reveals that the semiconductor foundry sector is masking deep structural shifts beneath government-subsidized cash flows. Top-line revenue growth across the major pure-play foundries—excluding DB HiTek—masks an industry-wide battle against severe margin compression.

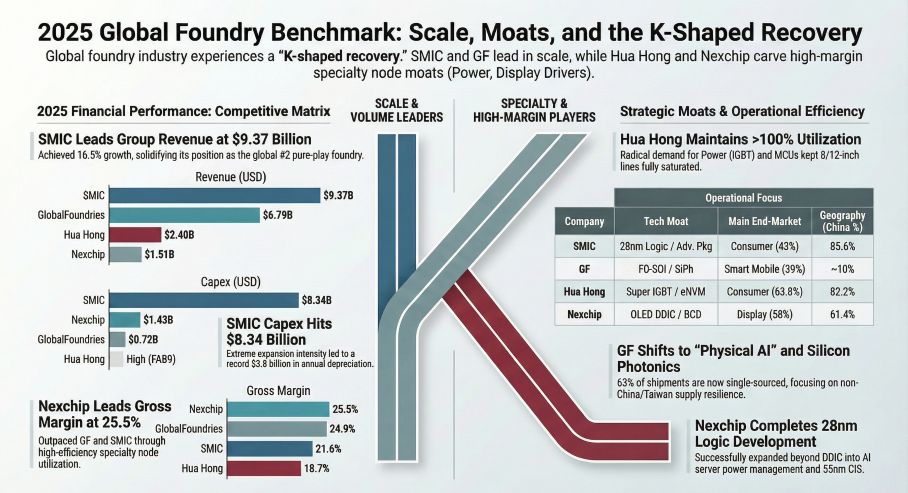

Semiconductor Manufacturing International Corp. (HKG: 0981) reported a robust 16.5% top-line expansion to $9.36 billion, underpinned by a 93.5% utilization rate. However, the true operational moat lies in its cash flow generation. SMIC recorded operating cash flow (CFO) of $2.79 billion against a net income of $701 million—a 3.98x coverage ratio. The delta is entirely driven by a massive $3.8 billion depreciation and amortization burden, representing over 40% of its revenue.

Conversely, Hua Hong Semiconductor (HKG: 1347) presents a starker depreciation profile. Its FAB9 (Wuxi) second-phase ramp-up generated a 20% revenue spike to $2.40 billion, yet net profit collapsed to a mere $52 million. This 13.45x CFO-to-Net-Income ratio indicates that while operational cash collection remains highly functional, the sheer weight of fixed-asset capital expenditures is temporarily crushing net margins. We expect management to implement aggressive cost-pass-through mechanisms into 2026 to offset this depreciation cliff, assuming consumer electronics demand holds.

At the other end of the spectrum, Nexchip (SHA: 688249) reported an exceptionally tight Days Inventory Outstanding (DIO) of 77.2 days, signaling successful inventory de-stocking within the OLED display driver IC (DDIC) market. Yet, close to 40% of its $98 million net profit stemmed from a one-off $39 million mask technology transfer. Stripping away non-recurring items exposes a far more fragile core profitability model reliant on high customer concentration (top five clients represent 55.69% of revenue).

Supply Chain Pivot: Weaponized CAPEX and "Guardrail" Economics

The 2025 filings confirm that capital allocation in the foundry space is no longer dictated purely by market demand; it is overwhelmingly subordinate to state-sponsored geoeconomics.

GlobalFoundries (NASDAQ: GFS) flatlined at $6.79 billion in revenue (up 0.6% YoY) despite a 10.4% volume increase, directly reflecting a 10.4% drop in Average Selling Prices (ASP). To insulate itself, GF relies heavily on its $1.5 billion US CHIPS Act award to double capacity at its Malta, New York, and Essex Junction, Vermont sites. However, analyzing GF's 10-K risk factors exposes the hidden cost of federal capital: structural rigidity. The CHIPS Act "guardrails" explicitly prohibit GF from expanding advanced capacity in China for a decade and strictly limit stock buybacks. This binds GF's global agility, locking the company out of the booming Chinese domestic EV supply chain and limiting its ability to pursue accretive acquisitions in restricted regions.

Meanwhile, facing severe US export controls on immersion DUV lithography, Chinese foundries are forced into accelerated vertical integration. SMIC unleashed an $8.34 billion CAPEX blitz to expand operations across Shanghai, Beijing, Tianjin, and Shenzhen. The localized supply chain is no longer a strategic option; it is a statutory survival mechanism.

Technology Nodes: The Shift Toward Physical AI and Power Management

With advanced logic locked behind extreme capital and regulatory barriers, second-tier foundries are carving out high-margin niches through specialty platforms.

GlobalFoundries is aggressively cornering the "Physical AI" and telecommunications infrastructure markets. By finalizing the integration of Advanced Micro Foundry (AMF), GF expanded its Silicon Photonics (SiPh) revenue by 29.1%. Paired with its proprietary FD-SOI (FDX™) technology, GF has engineered a moat where 63% of its wafer shipments are single-sourced, legally binding fabless designers to GF’s specific process design kits (PDKs).

Hua Hong is doubling down on automotive power discretes, successfully pushing its 1.6um Super IGBT and 40/55nm eFlash MCUs into mass production. This directly targets the EV drivetrain and inverter markets. DB HiTek mirrors this specialized approach, dominating the 8-inch pure-play space through UHV 900V and 120V BCD processes, ensuring long-term contracts in automotive LiDAR and industrial power management.

HDIN Institutional Perspective

The 2025 reporting cycle signals a dangerous paradox: rising utilization rates masking an impending structural glut in mature nodes. The industry's CAPEX race—funded by US CHIPS Act grants and Chinese sovereign tax offsets (e.g., the "five-year tax holiday" tied to <65nm production)—is artificially inflating global capacity.

Our editorial board assesses that by late 2026, the artificial floor created by these subsidies will buckle under the weight of localized overcapacity. Foundries that fail to secure Single-Sourced proprietary nodes (like GF's SiPh or Hua Hong's Super IGBT) will face existential pricing wars. The era of generic 28nm/40nm logic profitability is ending; the future belongs exclusively to foundries capable of executing bespoke, application-specific architectures immune to regional tariff barriers.

Related Topics & Downloads

* Click the PDF download link under 'Related Topics' to access the presentation of this report.

* Click this link to watch the YouTube video discussing the 2025 Foundry CAPEX cycle.

About HDIN Research

HDIN Research (www.hdinresearch.com) is a premier provider of institutional market intelligence, specializing in deep-tech supply chains, semiconductor financial forensics, and geopolitical macroeconomic strategy.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*

Figure 2025 Global Foundry Benchmark: Scale, Moats, and the K-Shaped Recovery

Financial Health & Operational Moats: The Depreciation DistortionA rigorous audit of 2025 annual filings reveals that the semiconductor foundry sector is masking deep structural shifts beneath government-subsidized cash flows. Top-line revenue growth across the major pure-play foundries—excluding DB HiTek—masks an industry-wide battle against severe margin compression.

Semiconductor Manufacturing International Corp. (HKG: 0981) reported a robust 16.5% top-line expansion to $9.36 billion, underpinned by a 93.5% utilization rate. However, the true operational moat lies in its cash flow generation. SMIC recorded operating cash flow (CFO) of $2.79 billion against a net income of $701 million—a 3.98x coverage ratio. The delta is entirely driven by a massive $3.8 billion depreciation and amortization burden, representing over 40% of its revenue.

Conversely, Hua Hong Semiconductor (HKG: 1347) presents a starker depreciation profile. Its FAB9 (Wuxi) second-phase ramp-up generated a 20% revenue spike to $2.40 billion, yet net profit collapsed to a mere $52 million. This 13.45x CFO-to-Net-Income ratio indicates that while operational cash collection remains highly functional, the sheer weight of fixed-asset capital expenditures is temporarily crushing net margins. We expect management to implement aggressive cost-pass-through mechanisms into 2026 to offset this depreciation cliff, assuming consumer electronics demand holds.

At the other end of the spectrum, Nexchip (SHA: 688249) reported an exceptionally tight Days Inventory Outstanding (DIO) of 77.2 days, signaling successful inventory de-stocking within the OLED display driver IC (DDIC) market. Yet, close to 40% of its $98 million net profit stemmed from a one-off $39 million mask technology transfer. Stripping away non-recurring items exposes a far more fragile core profitability model reliant on high customer concentration (top five clients represent 55.69% of revenue).

Supply Chain Pivot: Weaponized CAPEX and "Guardrail" Economics

The 2025 filings confirm that capital allocation in the foundry space is no longer dictated purely by market demand; it is overwhelmingly subordinate to state-sponsored geoeconomics.

GlobalFoundries (NASDAQ: GFS) flatlined at $6.79 billion in revenue (up 0.6% YoY) despite a 10.4% volume increase, directly reflecting a 10.4% drop in Average Selling Prices (ASP). To insulate itself, GF relies heavily on its $1.5 billion US CHIPS Act award to double capacity at its Malta, New York, and Essex Junction, Vermont sites. However, analyzing GF's 10-K risk factors exposes the hidden cost of federal capital: structural rigidity. The CHIPS Act "guardrails" explicitly prohibit GF from expanding advanced capacity in China for a decade and strictly limit stock buybacks. This binds GF's global agility, locking the company out of the booming Chinese domestic EV supply chain and limiting its ability to pursue accretive acquisitions in restricted regions.

Meanwhile, facing severe US export controls on immersion DUV lithography, Chinese foundries are forced into accelerated vertical integration. SMIC unleashed an $8.34 billion CAPEX blitz to expand operations across Shanghai, Beijing, Tianjin, and Shenzhen. The localized supply chain is no longer a strategic option; it is a statutory survival mechanism.

Technology Nodes: The Shift Toward Physical AI and Power Management

With advanced logic locked behind extreme capital and regulatory barriers, second-tier foundries are carving out high-margin niches through specialty platforms.

GlobalFoundries is aggressively cornering the "Physical AI" and telecommunications infrastructure markets. By finalizing the integration of Advanced Micro Foundry (AMF), GF expanded its Silicon Photonics (SiPh) revenue by 29.1%. Paired with its proprietary FD-SOI (FDX™) technology, GF has engineered a moat where 63% of its wafer shipments are single-sourced, legally binding fabless designers to GF’s specific process design kits (PDKs).

Hua Hong is doubling down on automotive power discretes, successfully pushing its 1.6um Super IGBT and 40/55nm eFlash MCUs into mass production. This directly targets the EV drivetrain and inverter markets. DB HiTek mirrors this specialized approach, dominating the 8-inch pure-play space through UHV 900V and 120V BCD processes, ensuring long-term contracts in automotive LiDAR and industrial power management.

HDIN Institutional Perspective

The 2025 reporting cycle signals a dangerous paradox: rising utilization rates masking an impending structural glut in mature nodes. The industry's CAPEX race—funded by US CHIPS Act grants and Chinese sovereign tax offsets (e.g., the "five-year tax holiday" tied to <65nm production)—is artificially inflating global capacity.

Our editorial board assesses that by late 2026, the artificial floor created by these subsidies will buckle under the weight of localized overcapacity. Foundries that fail to secure Single-Sourced proprietary nodes (like GF's SiPh or Hua Hong's Super IGBT) will face existential pricing wars. The era of generic 28nm/40nm logic profitability is ending; the future belongs exclusively to foundries capable of executing bespoke, application-specific architectures immune to regional tariff barriers.

Related Topics & Downloads

* Click the PDF download link under 'Related Topics' to access the presentation of this report.

* Click this link to watch the YouTube video discussing the 2025 Foundry CAPEX cycle.

About HDIN Research

HDIN Research (www.hdinresearch.com) is a premier provider of institutional market intelligence, specializing in deep-tech supply chains, semiconductor financial forensics, and geopolitical macroeconomic strategy.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*