Luckin Coffee Dominates Digital Supply Chain as Starbucks' Operating Margins Collapse to 7.9% in FY2025

Date : 2026-04-01

Reading : 177

In FY2025, global coffee titans Starbucks (NASDAQ: SBUX) and Luckin Coffee (OTC: LKNCY) face severe profitability divergence. Driven by inflationary headwinds and digital disruption, agile operators leveraging vertical integration are capturing market share, forcing legacy brands into defensive cost-pass-through mechanisms and radical asset restructuring.

Figure 2025 Global Coffee Industry Audit

Financial Health & Operational Moats: The Structural Decay of the "Third Place"

Financial Health & Operational Moats: The Structural Decay of the "Third Place"

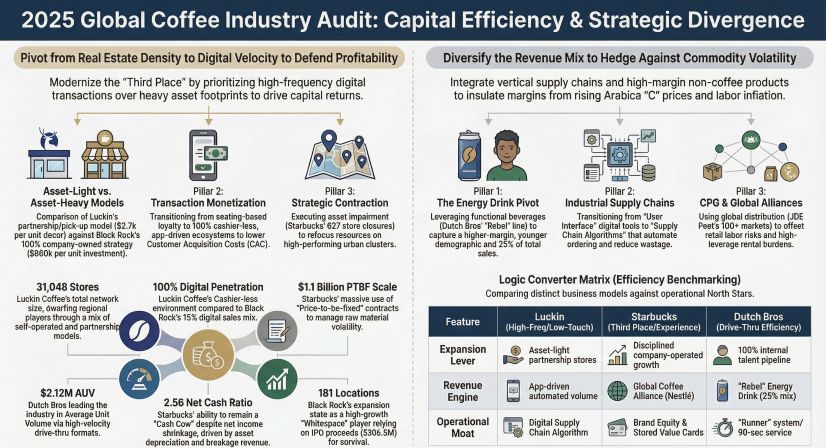

A granular audit of FY2025 corporate filings reveals a definitive bifurcation in capital efficiency. The era of high-capex, experience-driven coffee retail is buckling beneath the weight of labor inflation and changing consumer cadences.

Starbucks is trapped in a classic scale paradox. Despite a 2.8% top-line increase to $37.18 billion, the Seattle-based giant suffered severe margin compression, with operating margins plummeting 710 basis points from 15.0% to 7.4%. This decay was exacerbated by an $892 million impairment and restructuring charge tied to its "Back to Starbucks" turnaround mandate. The math is unforgiving: North American transaction volumes contracted by 4%, signaling that premium pricing without operational velocity is no longer a viable moat.

Conversely, Luckin Coffee operates with a ruthless, asset-light balance sheet. By transitioning 99.1% of its network to low-square-footage "pick-up" formats, Luckin achieved a 43.0% revenue surge to $6.85 billion. More critically, it maintained a 17.8% store-level operating margin across an immense footprint of 31,048 locations (inclusive of China Hong Kong). Luckin’s 100% digital cashier-less environment functionally eliminates frontline order-taking labor, shifting overhead entirely to throughput efficiency.

Meanwhile, Black Rock Coffee highlights the dangers of aggressive retail footprint expansion without cash flow discipline. Relying on a 100% corporate-owned model, Black Rock burns through a negative free cash flow of $33.1 million, choked by long-term lease liabilities comprising 37.7% of total assets. Management’s insistence on highlighting "store-level profit margins" while masking exorbitant corporate SG&A (20.6% of revenue) is a classic accounting distraction masking a highly fragile capital structure.

Supply Chain Pivot: EUDR Regulations and Intelligent CAPEX

Geopolitical fragmentation and ESG regulatory frameworks have transformed supply chain procurement from a back-office function to a primary driver of EPS volatility.

JDE Peet's (Euronext: JDEP) provides the starkest leading indicator for raw material inflation. The CPG giant explicitly modeled a 1.0% to 1.5% structural increase in raw material costs strictly attributed to the European Union Deforestation Regulation (EUDR) taking effect. For a company generating $11.2 billion in revenue, this represents a massive profitability headwind. While JDE Peet's attempts to cushion this via $9.05 million in active commodity derivative assets on the ICE and IFFE exchanges, the underlying reality is that regulatory compliance has permanently raised the sector's cost floor.

Starbucks utilizes a highly leveraged derivatives strategy to defend its margins, holding $1.1 billion in "Price-to-be-fixed" (PTBF) contracts. Yet, even this sophisticated financial engineering failed to prevent an 80-basis-point hit to operating margins from supply chain inflation in FY2025.

In stark contrast, Luckin's capital allocation targets physical vertical integration. The company deployed $365 million in CAPEX heavily weighted toward automated, smart roastery facilities in Kunshan, Pingnan, and Qingdao. By coupling these facilities with proprietary AI inventory algorithms, Luckin executes continuous inventory de-stocking at the store level, drastically reducing raw material wastage and shielding its gross margins from spot market volatility.

HDIN Institutional Perspective: Strategic Contraction vs. Capital Velocity

The FY2025 filings indicate that the sector has moved past organic unit growth; the next phase will be defined by strategic divestitures and capital velocity.

We view Starbucks’ decision to offload a 60% equity stake in its China operations to Boyu Capital as a profound geopolitical hedge. Navigating China's Personal Information Protection Law (PIPL) and fierce domestic price wars requires localized agility that a Seattle-based multinational structurally lacks. This joint venture is a tacit admission that Starbucks is transitioning from an operator to a brand-licensor in highly contested geographies.

Simultaneously, investors must scrutinize the quality of earnings in the high-growth drive-thru segment. Dutch Bros (NYSE: BROS) reported an impressive $2.12 million AUV and net income growth of 126%, fueled by high-margin Rebel energy drinks and the rollout of Tap Systems. However, our forensic audit notes a glaring discrepancy: Dutch Bros' accounts receivable surged by 73.6% against a top-line revenue growth of only 27.9%. In institutional equity research, this magnitude of divergence frequently flags aggressive revenue recognition or deteriorating credit quality among franchisees/partners.

Ultimately, the market will reward operators like JDE Peet's (recently navigating accretive acquisitions like Caribou) and Luckin, who view coffee not as a hospitality service, but as a high-frequency, digitized logistics operation.

Related Topics & Resources

* Click the PDF download link under 'Related Topics' to access the presentation of this report.

* Click this link to watch the YouTube video.

About HDIN Research

HDIN Research (www.hdinresearch.com) is a premier provider of institutional market intelligence, forensic financial auditing, and macroeconomic strategy. We deliver unfiltered, data-dense analysis for hedge funds, private equity firms, and sovereign wealth portfolios navigating complex global supply chains.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*

Figure 2025 Global Coffee Industry Audit

Financial Health & Operational Moats: The Structural Decay of the "Third Place"A granular audit of FY2025 corporate filings reveals a definitive bifurcation in capital efficiency. The era of high-capex, experience-driven coffee retail is buckling beneath the weight of labor inflation and changing consumer cadences.

Starbucks is trapped in a classic scale paradox. Despite a 2.8% top-line increase to $37.18 billion, the Seattle-based giant suffered severe margin compression, with operating margins plummeting 710 basis points from 15.0% to 7.4%. This decay was exacerbated by an $892 million impairment and restructuring charge tied to its "Back to Starbucks" turnaround mandate. The math is unforgiving: North American transaction volumes contracted by 4%, signaling that premium pricing without operational velocity is no longer a viable moat.

Conversely, Luckin Coffee operates with a ruthless, asset-light balance sheet. By transitioning 99.1% of its network to low-square-footage "pick-up" formats, Luckin achieved a 43.0% revenue surge to $6.85 billion. More critically, it maintained a 17.8% store-level operating margin across an immense footprint of 31,048 locations (inclusive of China Hong Kong). Luckin’s 100% digital cashier-less environment functionally eliminates frontline order-taking labor, shifting overhead entirely to throughput efficiency.

Meanwhile, Black Rock Coffee highlights the dangers of aggressive retail footprint expansion without cash flow discipline. Relying on a 100% corporate-owned model, Black Rock burns through a negative free cash flow of $33.1 million, choked by long-term lease liabilities comprising 37.7% of total assets. Management’s insistence on highlighting "store-level profit margins" while masking exorbitant corporate SG&A (20.6% of revenue) is a classic accounting distraction masking a highly fragile capital structure.

Supply Chain Pivot: EUDR Regulations and Intelligent CAPEX

Geopolitical fragmentation and ESG regulatory frameworks have transformed supply chain procurement from a back-office function to a primary driver of EPS volatility.

JDE Peet's (Euronext: JDEP) provides the starkest leading indicator for raw material inflation. The CPG giant explicitly modeled a 1.0% to 1.5% structural increase in raw material costs strictly attributed to the European Union Deforestation Regulation (EUDR) taking effect. For a company generating $11.2 billion in revenue, this represents a massive profitability headwind. While JDE Peet's attempts to cushion this via $9.05 million in active commodity derivative assets on the ICE and IFFE exchanges, the underlying reality is that regulatory compliance has permanently raised the sector's cost floor.

Starbucks utilizes a highly leveraged derivatives strategy to defend its margins, holding $1.1 billion in "Price-to-be-fixed" (PTBF) contracts. Yet, even this sophisticated financial engineering failed to prevent an 80-basis-point hit to operating margins from supply chain inflation in FY2025.

In stark contrast, Luckin's capital allocation targets physical vertical integration. The company deployed $365 million in CAPEX heavily weighted toward automated, smart roastery facilities in Kunshan, Pingnan, and Qingdao. By coupling these facilities with proprietary AI inventory algorithms, Luckin executes continuous inventory de-stocking at the store level, drastically reducing raw material wastage and shielding its gross margins from spot market volatility.

HDIN Institutional Perspective: Strategic Contraction vs. Capital Velocity

The FY2025 filings indicate that the sector has moved past organic unit growth; the next phase will be defined by strategic divestitures and capital velocity.

We view Starbucks’ decision to offload a 60% equity stake in its China operations to Boyu Capital as a profound geopolitical hedge. Navigating China's Personal Information Protection Law (PIPL) and fierce domestic price wars requires localized agility that a Seattle-based multinational structurally lacks. This joint venture is a tacit admission that Starbucks is transitioning from an operator to a brand-licensor in highly contested geographies.

Simultaneously, investors must scrutinize the quality of earnings in the high-growth drive-thru segment. Dutch Bros (NYSE: BROS) reported an impressive $2.12 million AUV and net income growth of 126%, fueled by high-margin Rebel energy drinks and the rollout of Tap Systems. However, our forensic audit notes a glaring discrepancy: Dutch Bros' accounts receivable surged by 73.6% against a top-line revenue growth of only 27.9%. In institutional equity research, this magnitude of divergence frequently flags aggressive revenue recognition or deteriorating credit quality among franchisees/partners.

Ultimately, the market will reward operators like JDE Peet's (recently navigating accretive acquisitions like Caribou) and Luckin, who view coffee not as a hospitality service, but as a high-frequency, digitized logistics operation.

Related Topics & Resources

* Click the PDF download link under 'Related Topics' to access the presentation of this report.

* Click this link to watch the YouTube video.

About HDIN Research

HDIN Research (www.hdinresearch.com) is a premier provider of institutional market intelligence, forensic financial auditing, and macroeconomic strategy. We deliver unfiltered, data-dense analysis for hedge funds, private equity firms, and sovereign wealth portfolios navigating complex global supply chains.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*