MicroCloud Hologram (NASDAQ:HOLO) Confronts Margin Compression as Holographic Tech Services Yield 23.02% Amid $256M Cash Hoard

Date : 2026-04-01

Reading : 73

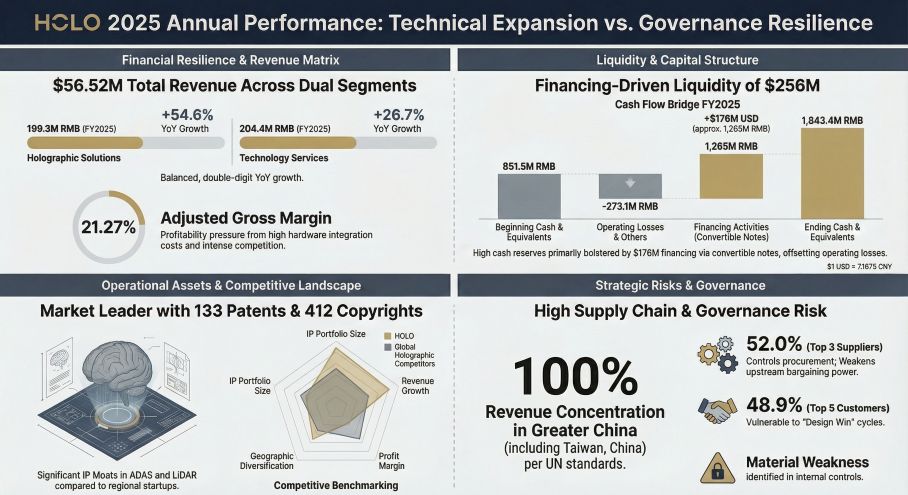

Shenzhen-based MicroCloud Hologram (NASDAQ:HOLO) reported $56.52M in 2025 revenue, driven by ADAS software and LiDAR integration. Yet, extreme customer concentration and aggressive pricing from automotive OEMs forced aggregate gross margins down to 21.27%, prompting a defensive reliance on dilutive financing rather than organic cash generation.

Figure HOLO 2025 Annual Performance: Technical Expansion vs Governance Resilience

Financial Health & Operational Moats: The Illusion of Platform Scalability

Financial Health & Operational Moats: The Illusion of Platform Scalability

MicroCloud Hologram’s 2025 Form 20-F reveals a company caught in a structural transition from a custom project-based engineering firm to a platform-based SDK provider—a pivot that is currently failing to deliver margin expansion. Total fiscal 2025 revenue reached $56.52M (up from 2024), but the underlying unit economics indicate severe deterioration in pricing power.

The company’s dual-engine model is misfiring on the profitability front:

* Holographic Solutions (Hardware/ADAS): Generating $27.73M in revenue, this segment yielded a meager 19.46% gross margin. The "turnkey" nature of embedding proprietary software into third-party LiDAR hardware leaves HOLO exposed to brutal cost structures, lacking the vertical integration necessary to defend against upstream component inflation.

* Holographic Technology Service (SDK/Ads): Once the high-margin growth narrative, this segment's gross margin collapsed to 23.02% in 2025, down violently from 48.4% in 2023. As customer acquisition costs via channel distributors spiked, the expected software margin premium evaporated.

More alarmingly, management instituted a 67.3% reduction in R&D expenditure, dropping it to a mere $7.93M. In a sector defined by rapid iteration toward solid-state LiDAR, starving the R&D pipeline jeopardizes the monetization lifecycle of their existing 133-patent moat. Furthermore, a 19.9% bad debt provision on accounts receivable signals aggressive early-stage revenue recognition under ASC 606, warning of potential future earnings quality decay.

Supply Chain Pivot: Squeezed Between Vendor Lock-in and Buyer Leverage

HOLO’s geographic and supply chain architecture remains intensely localized. Despite management's guidance hinting at global service capabilities, 100% of 2025 revenues were captured within the Greater China region (including Taiwan, China, Hong Kong, and Macau).

The supply chain geometry presents a textbook "double-squeeze":

* Downstream Pricing Vise: The top five customers dictate 48.9% of total revenue, with the lead client commanding 17.1%. As broader EV and auto markets engage in fierce price wars and aggressive inventory de-stocking, Tier-1 auto OEMs are exercising their leverage. HOLO lacks viable cost-pass-through mechanisms, forcing them to absorb the margin hits.

* Upstream Concentration: The top three suppliers account for 52.0% of procurement. Without multi-sourcing parity, HOLO cannot negotiate favorable raw material pricing for its integrated circuit boards and LiDAR components, permanently capping the gross margin upside of its Solutions division.

HDIN Institutional Perspective: Liquidity as a Mask for Structural Governance Deficits

From an institutional vantage point, HOLO exhibits the classic hallmarks of a "financing-driven" FPI (Foreign Private Issuer) rather than an operationally compounding asset. The headline figure of $256M in cash and equivalents on the 2025 balance sheet is optically strong but fundamentally dilutive, driven by $1.76M in net financing inflows (primarily convertible notes) rather than organic operating cash flow.

This liquidity buffer masks deep structural cracks. The company officially admitted to "material weaknesses" in its Internal Control over Financial Reporting (ICFR), specifically citing a deficit in US GAAP expertise. When coupled with the Nasdaq Rule 5615(a)(3) FPI exemptions—which bypass shareholder approval for major equity issuances—retail and institutional investors face acute dilution risks. The April 2025 1:40 reverse stock split to maintain Nasdaq minimum bid compliance underscores the market's pricing of these governance discounts.

Looking forward to 2026, HOLO's survival hinges on executing accretive acquisitions to diversify its revenue base away from auto OEMs into industrial robotics and smart city initiatives. Until the company proves it can monetize its digital twin technology without sacrificing margins to channel distributors, the stock remains a high-beta proxy for Chinese autonomous driving capex cycles, weighed down by substantial corporate governance overhang.

Strategic Actions & Source Material

* Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

* Video Link: Click this link to watch the YouTube video breaking down the supply chain dynamics.

About HDIN Research

HDIN Research (www.hdinresearch.com) is a premier provider of institutional-grade equity research, alternative data analytics, and strategic market intelligence. We specialize in decoding complex corporate filings, supply chain pivots, and macro-economic shifts to deliver actionable, alpha-generating insights for global investors.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*

Figure HOLO 2025 Annual Performance: Technical Expansion vs Governance Resilience

Financial Health & Operational Moats: The Illusion of Platform ScalabilityMicroCloud Hologram’s 2025 Form 20-F reveals a company caught in a structural transition from a custom project-based engineering firm to a platform-based SDK provider—a pivot that is currently failing to deliver margin expansion. Total fiscal 2025 revenue reached $56.52M (up from 2024), but the underlying unit economics indicate severe deterioration in pricing power.

The company’s dual-engine model is misfiring on the profitability front:

* Holographic Solutions (Hardware/ADAS): Generating $27.73M in revenue, this segment yielded a meager 19.46% gross margin. The "turnkey" nature of embedding proprietary software into third-party LiDAR hardware leaves HOLO exposed to brutal cost structures, lacking the vertical integration necessary to defend against upstream component inflation.

* Holographic Technology Service (SDK/Ads): Once the high-margin growth narrative, this segment's gross margin collapsed to 23.02% in 2025, down violently from 48.4% in 2023. As customer acquisition costs via channel distributors spiked, the expected software margin premium evaporated.

More alarmingly, management instituted a 67.3% reduction in R&D expenditure, dropping it to a mere $7.93M. In a sector defined by rapid iteration toward solid-state LiDAR, starving the R&D pipeline jeopardizes the monetization lifecycle of their existing 133-patent moat. Furthermore, a 19.9% bad debt provision on accounts receivable signals aggressive early-stage revenue recognition under ASC 606, warning of potential future earnings quality decay.

Supply Chain Pivot: Squeezed Between Vendor Lock-in and Buyer Leverage

HOLO’s geographic and supply chain architecture remains intensely localized. Despite management's guidance hinting at global service capabilities, 100% of 2025 revenues were captured within the Greater China region (including Taiwan, China, Hong Kong, and Macau).

The supply chain geometry presents a textbook "double-squeeze":

* Downstream Pricing Vise: The top five customers dictate 48.9% of total revenue, with the lead client commanding 17.1%. As broader EV and auto markets engage in fierce price wars and aggressive inventory de-stocking, Tier-1 auto OEMs are exercising their leverage. HOLO lacks viable cost-pass-through mechanisms, forcing them to absorb the margin hits.

* Upstream Concentration: The top three suppliers account for 52.0% of procurement. Without multi-sourcing parity, HOLO cannot negotiate favorable raw material pricing for its integrated circuit boards and LiDAR components, permanently capping the gross margin upside of its Solutions division.

HDIN Institutional Perspective: Liquidity as a Mask for Structural Governance Deficits

From an institutional vantage point, HOLO exhibits the classic hallmarks of a "financing-driven" FPI (Foreign Private Issuer) rather than an operationally compounding asset. The headline figure of $256M in cash and equivalents on the 2025 balance sheet is optically strong but fundamentally dilutive, driven by $1.76M in net financing inflows (primarily convertible notes) rather than organic operating cash flow.

This liquidity buffer masks deep structural cracks. The company officially admitted to "material weaknesses" in its Internal Control over Financial Reporting (ICFR), specifically citing a deficit in US GAAP expertise. When coupled with the Nasdaq Rule 5615(a)(3) FPI exemptions—which bypass shareholder approval for major equity issuances—retail and institutional investors face acute dilution risks. The April 2025 1:40 reverse stock split to maintain Nasdaq minimum bid compliance underscores the market's pricing of these governance discounts.

Looking forward to 2026, HOLO's survival hinges on executing accretive acquisitions to diversify its revenue base away from auto OEMs into industrial robotics and smart city initiatives. Until the company proves it can monetize its digital twin technology without sacrificing margins to channel distributors, the stock remains a high-beta proxy for Chinese autonomous driving capex cycles, weighed down by substantial corporate governance overhang.

Strategic Actions & Source Material

* Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

* Video Link: Click this link to watch the YouTube video breaking down the supply chain dynamics.

About HDIN Research

HDIN Research (www.hdinresearch.com) is a premier provider of institutional-grade equity research, alternative data analytics, and strategic market intelligence. We specialize in decoding complex corporate filings, supply chain pivots, and macro-economic shifts to deliver actionable, alpha-generating insights for global investors.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*