Mindray Accelerates Global High-End Ultrasound Disruption as Gross Margins Hit 60.3% in FY2025

Date : 2026-04-02

Reading : 703

Shenzhen-based Mindray (SZSE: 300760) is aggressively dismantling Western imaging oligopolies in 2025. By weaponizing a 60.3% gross margin and localized supply chains against tariff headwinds, the manufacturer is forcing GE HealthCare and Siemens Healthineers into margin-crushing defensive postures across global premium hospital networks.

Financial Health & Operational Moats: The Software-Defined Premium

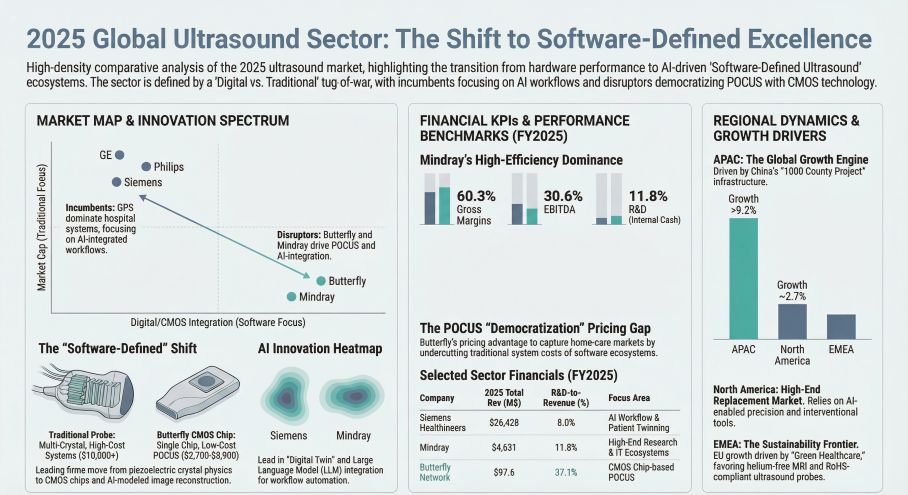

The global medical imaging sector has violently pivoted from a hardware specifications arms race to a software-defined, ecosystem-driven battleground. According to FY2025 corporate filings, capital expenditures are universally skewing toward AI-integrated clinical decision support. However, the financial translation of these R&D outlays reveals severe disparities in capital allocation efficiency.

Mindray’s (SZSE: 300760) financial posture exemplifies vertical integration done right. Generating $1.13 billion in net profit with an EBITDA margin of 30.6%, the company is entirely self-funding its 11.8% R&D expenditure ($546.6 million). By launching the Resona A20 and the "He-Yuan" ultrasound AI model, Mindray has successfully penetrated eight of the top ten Integrated Delivery Networks (IDNs) in the U.S., effectively breaking the monopolistic grip of the GPS (GE, Philips, Siemens) cartel in premium research hospitals.

Conversely, Butterfly Network (NYSE: BFLY) highlights the lethal cost of hardware democratization. Despite achieving an industry-leading revenue-per-employee metric ($443,600) via its shift toward a SaaS-heavy model (software and services now constitute 35% of revenue), the company’s structural cash burn remains critical. With an accumulated deficit reaching $879.2 million and a net loss of $77.1 million in 2025, Butterfly's CMOS "Ultrasound-on-Chip" technology may be clinically revolutionary, but its financial viability demands immediate accretive acquisitions or aggressive subscription scaling to avoid insolvency.

Meanwhile, Wandong Medical (SHSE: 600055) is flashing bright red on the audit dashboard. The company reported an 11.64% drop in top-line revenue alongside an 85.71% surge in administrative expenses, driving a $31.7 million net loss. More alarmingly, Wandong is choking on 235 days of Days Inventory Outstanding (DIO), with digital radiography (DR) inventory ballooning by 936%. This inventory de-stocking failure, tied to prolonged Volume-Based Procurement (VBP) delivery cycles in China, signals impending impairment charges.

Supply Chain Pivot: Geopolitical De-Risking and ‘Local-for-Local’ Execution

In 2025, the "efficiency-first" globalization doctrine is dead; "resilience-first" is the new operational mandate. Faced with fractured trade corridors and rising protectionism, OEMs are architecting highly localized manufacturing matrices to implement effective cost-pass-through mechanisms and shield gross margins.

Mindray leads this operational decoupling. The company has aggressively rolled out its "Local-for-Local" footprint, initiating localized manufacturing in 11 of 14 targeted countries, achieving a near-100% localization rate for its U.S. commercial operations to neutralize Section 301 tariff friction. Similarly, Edan Instruments (SZSE: 300206) inaugurated its U.S. overseas manufacturing center in 2025, deploying modular device architectures to slash post-sale maintenance logistics and bypass cross-border freight volatility.

On the opposite end of the risk spectrum lies Butterfly Network. Filings explicitly state that their core CMOS technology is entirely reliant on Taiwan Semiconductor Manufacturing Company (TSMC) in Taiwan, China, acting as a single-source foundry. This non-exclusive contract not only exposes Butterfly to catastrophic geopolitical and seismic disruptions but also inflicts heavy cash flow damage, as the firm is contractually obligated to buy back unused raw wafers. To hedge against this single-point failure, Butterfly is intentionally holding inflated levels of core component inventory, actively sacrificing liquidity for supply chain certainty.

Philips (NYSE: PHG) and GE HealthCare (NYSE: GEHC) are actively combating these same macro headwinds. GEHC noted a $245 million hit to operating profits due to bilateral tariffs, forcing a massive regionalization of its supply chain. Philips is countering freight inflation via dual-sourcing and selective regional component integration to defend its 46.7% D&T segment gross margin.

Figure 2025 Global Ultrasound Sector: The Shift to Software-Defined Excellence

HDIN Institutional Perspective: Impairment Bombs and M&A Horizons

HDIN Institutional Perspective: Impairment Bombs and M&A Horizons

HDIN Research views the 2026 fiscal horizon as a period of brutal consolidation, driven by tightening hospital CAPEX and value-based care (VBC) mandates. The balance sheets of legacy Western giants carry hidden vulnerabilities that the market is currently mispricing.

Siemens Healthineers (ETR: SHL) is operating with a balance sheet heavily weighted by M&A-driven intangibles, with goodwill constituting a staggering 60.4% of its non-current assets. In an environment where Chinese public hospital procurement is increasingly ring-fenced by VBP policies, and global hospital systems are delaying equipment upgrades, Siemens faces significant margin compression. If the anticipated revenue synergies from its "Elevating" strategy fail to materialize, investors should brace for massive goodwill impairment write-downs.

In stark contrast, Mindray’s pristine balance sheet (27.43% debt-to-asset ratio) and massive operating cash flow ($1.41 billion) position it as the sector’s apex predator. Following its successful absorption of DiaSys and APT Medical, we project Mindray will execute further accretive acquisitions in the high-value consumables or AI-algorithm space by 2026. The true battlefront is no longer piezoelectric crystal frequency; it is the race to monetize longitudinal clinical data and dominate the surgical suite via interventional imaging.

Related Resources

* Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

* Video Link: Click this link to watch the YouTube video.

About HDIN Research

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in deep-dive financial forensics and supply chain penetration within the medical device, semiconductor, and industrial technology sectors. Visit us at www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*

Financial Health & Operational Moats: The Software-Defined Premium

The global medical imaging sector has violently pivoted from a hardware specifications arms race to a software-defined, ecosystem-driven battleground. According to FY2025 corporate filings, capital expenditures are universally skewing toward AI-integrated clinical decision support. However, the financial translation of these R&D outlays reveals severe disparities in capital allocation efficiency.

Mindray’s (SZSE: 300760) financial posture exemplifies vertical integration done right. Generating $1.13 billion in net profit with an EBITDA margin of 30.6%, the company is entirely self-funding its 11.8% R&D expenditure ($546.6 million). By launching the Resona A20 and the "He-Yuan" ultrasound AI model, Mindray has successfully penetrated eight of the top ten Integrated Delivery Networks (IDNs) in the U.S., effectively breaking the monopolistic grip of the GPS (GE, Philips, Siemens) cartel in premium research hospitals.

Conversely, Butterfly Network (NYSE: BFLY) highlights the lethal cost of hardware democratization. Despite achieving an industry-leading revenue-per-employee metric ($443,600) via its shift toward a SaaS-heavy model (software and services now constitute 35% of revenue), the company’s structural cash burn remains critical. With an accumulated deficit reaching $879.2 million and a net loss of $77.1 million in 2025, Butterfly's CMOS "Ultrasound-on-Chip" technology may be clinically revolutionary, but its financial viability demands immediate accretive acquisitions or aggressive subscription scaling to avoid insolvency.

Meanwhile, Wandong Medical (SHSE: 600055) is flashing bright red on the audit dashboard. The company reported an 11.64% drop in top-line revenue alongside an 85.71% surge in administrative expenses, driving a $31.7 million net loss. More alarmingly, Wandong is choking on 235 days of Days Inventory Outstanding (DIO), with digital radiography (DR) inventory ballooning by 936%. This inventory de-stocking failure, tied to prolonged Volume-Based Procurement (VBP) delivery cycles in China, signals impending impairment charges.

Supply Chain Pivot: Geopolitical De-Risking and ‘Local-for-Local’ Execution

In 2025, the "efficiency-first" globalization doctrine is dead; "resilience-first" is the new operational mandate. Faced with fractured trade corridors and rising protectionism, OEMs are architecting highly localized manufacturing matrices to implement effective cost-pass-through mechanisms and shield gross margins.

Mindray leads this operational decoupling. The company has aggressively rolled out its "Local-for-Local" footprint, initiating localized manufacturing in 11 of 14 targeted countries, achieving a near-100% localization rate for its U.S. commercial operations to neutralize Section 301 tariff friction. Similarly, Edan Instruments (SZSE: 300206) inaugurated its U.S. overseas manufacturing center in 2025, deploying modular device architectures to slash post-sale maintenance logistics and bypass cross-border freight volatility.

On the opposite end of the risk spectrum lies Butterfly Network. Filings explicitly state that their core CMOS technology is entirely reliant on Taiwan Semiconductor Manufacturing Company (TSMC) in Taiwan, China, acting as a single-source foundry. This non-exclusive contract not only exposes Butterfly to catastrophic geopolitical and seismic disruptions but also inflicts heavy cash flow damage, as the firm is contractually obligated to buy back unused raw wafers. To hedge against this single-point failure, Butterfly is intentionally holding inflated levels of core component inventory, actively sacrificing liquidity for supply chain certainty.

Philips (NYSE: PHG) and GE HealthCare (NYSE: GEHC) are actively combating these same macro headwinds. GEHC noted a $245 million hit to operating profits due to bilateral tariffs, forcing a massive regionalization of its supply chain. Philips is countering freight inflation via dual-sourcing and selective regional component integration to defend its 46.7% D&T segment gross margin.

Figure 2025 Global Ultrasound Sector: The Shift to Software-Defined Excellence

HDIN Institutional Perspective: Impairment Bombs and M&A HorizonsHDIN Research views the 2026 fiscal horizon as a period of brutal consolidation, driven by tightening hospital CAPEX and value-based care (VBC) mandates. The balance sheets of legacy Western giants carry hidden vulnerabilities that the market is currently mispricing.

Siemens Healthineers (ETR: SHL) is operating with a balance sheet heavily weighted by M&A-driven intangibles, with goodwill constituting a staggering 60.4% of its non-current assets. In an environment where Chinese public hospital procurement is increasingly ring-fenced by VBP policies, and global hospital systems are delaying equipment upgrades, Siemens faces significant margin compression. If the anticipated revenue synergies from its "Elevating" strategy fail to materialize, investors should brace for massive goodwill impairment write-downs.

In stark contrast, Mindray’s pristine balance sheet (27.43% debt-to-asset ratio) and massive operating cash flow ($1.41 billion) position it as the sector’s apex predator. Following its successful absorption of DiaSys and APT Medical, we project Mindray will execute further accretive acquisitions in the high-value consumables or AI-algorithm space by 2026. The true battlefront is no longer piezoelectric crystal frequency; it is the race to monetize longitudinal clinical data and dominate the surgical suite via interventional imaging.

Related Resources

* Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

* Video Link: Click this link to watch the YouTube video.

About HDIN Research

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in deep-dive financial forensics and supply chain penetration within the medical device, semiconductor, and industrial technology sectors. Visit us at www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*