Keysight Software Pivot Secures 62.1% Margins as Rigol’s ASIC Breakthrough Triggers T&M Supply Chain Realignment

Date : 2026-04-03

Reading : 321

In FY2025, global test and measurement leaders—including Keysight, Rigol, and Siglent—realigned operations across the U.S., China, and Malaysia. Driven by AI data center expansion and acute EV infrastructure slowdowns, firms executed aggressive software M&A and Southeast Asian capacity shifts to mitigate margin compression and bypass shifting tariff structures.

Financial Health & Operational Moats: The Software Premium vs. Hardware Catch-Up

The 2025 fiscal filings reveal a stark divergence in capital allocation frameworks. Top-tier legacy players are abandoning the physical hardware dogfight, utilizing accretive acquisitions to secure protocol-layer monopolies.

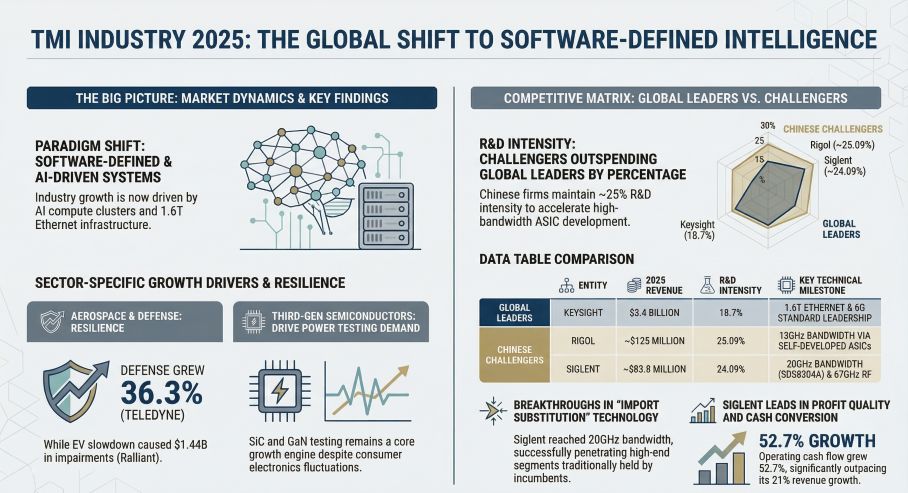

Keysight Technologies (NYSE: KEYS) reported $5.375 billion in top-line revenue with a commanding 62.1% gross margin. Rather than defending lower-band frequency markets, Keysight deployed $1.007 billion in R&D (18.7% intensity) toward 1.6Tb/sec Ethernet and 6G physical layer testing. More critically, its $1.415 billion acquisition of Spirent and the buyout of Synopsys’ Optical Solutions Group signal a terminal shift: Keysight is transitioning from a box-seller to an AI-cluster simulation gatekeeper, locking hyperscalers into high-margin recurring software revenue.

Conversely, the Chinese dual-oligopoly is executing an aggressive vertical integration strategy to break Western bandwidth embargoes. Rigol Technologies (SHA: 688337) successfully commercialized its "Cassiopeia" ASIC platform, driving its digital oscilloscope bandwidth to 13GHz. While Rigol posted a 16.04% revenue growth ($125.25 million), the firm suffered acute margin compression, with core gross margins contracting 4.14% to 55.62%. This compression reflects the high initial CapEx payload of semiconductor self-reliance and the dilution from educational bulk-tender pricing.

Siglent Technologies (SHA: 688138) opted for a premium-tier skimming strategy. By launching the SDS8204A 20GHz oscilloscope and 50GHz VNAs, high-end product sales surged 57.14%. This insulated Siglent from the pricing floor, resulting in superior financial health: a 61.48% gross margin and an exceptional $25.09 million in operating cash flow (+52.76% YoY).

Figure TMI INDUSTRY 2025: THE GLOBAL SHIFT TO SOFTWARE-DEFINED INTELLIGENCE

Supply Chain Pivot: The Southeast Asian Cost-Pass-Through Mechanism

Supply Chain Pivot: The Southeast Asian Cost-Pass-Through Mechanism

Geopolitical friction has forced an irreversible structural shift in the global T&M supply chain. The U.S. Section 301 tariffs and reciprocal trade barriers have rendered bilateral export models mathematically unviable.

In response, both Rigol and Siglent have executed a "China + 1" localization mandate. Rigol directed $8.50 million in CapEx toward its Penang, Malaysia manufacturing hub, which is currently enduring a costly capacity ramp-up phase. Siglent’s corresponding Penang facility officially went online in April 2025.

Standard market models interpret these moves as simple capacity expansion. In reality, these Southeast Asian facilities act as critical cost-pass-through mechanisms. By routing final assembly through Malaysia, Chinese T&M firms bypass U.S. import penalties, protecting their pricing parity against domestic American competitors. However, until these facilities achieve scale, expect localized inventory de-stocking turbulence and elevated freight costs to drag on quarterly earnings.

HDIN Institutional Perspective: Capital Allocation Errors and Sector Divergence

Reviewing the 10-K disclosures through a macroeconomic lens exposes a violent sector rotation. The capital market's honeymoon phase with Advanced Mobility (EV) testing has cratered, replaced entirely by AI infrastructure CapEx.

The collateral damage is evident in Ralliant (NYSE: RLI). The former Fortive spin-off recognized a catastrophic $1.44 billion non-cash goodwill impairment in Q4 2025 related to its EA Elektro-Automatik unit. This impairment is a direct downstream consequence of delayed EV adoption curves, drastically elongating the payback period on its high-power bidirectional EV testing equipment. Compounded by a $32.7 million interest burden (5.5% effective rate) on its debt, Ralliant exemplifies the terminal risk of over-leveraging into cyclical hardware trends.

Simultaneously, Teledyne (NYSE: TDY) and AMETEK (NYSE: AME) are playing a high-wire M&A game. Teledyne carries $8.688 billion in goodwill after acquiring Qioptiq, while AMETEK dropped $933.2 million cash for Kern Microtechnik and FARO Technologies. While defense electronics (up 36.3% for Teledyne) mask current balance sheet bloat, any macroeconomic contraction will expose these firms to the exact impairment guillotine Ralliant just suffered.

The 2026 Street Outlook: Hardware parameters are no longer the ultimate moat. Investors must rotate equity exposure toward T&M entities exhibiting software revenue stickiness and immune-grade supply chains. Rigol’s 25.09% R&D intensity will either yield a monopolistic ASIC dividend in 2026 or burn its remaining cash runway. Meanwhile, Keysight’s transformation into an AI interconnect software firm makes its current multiple historically defensible.

Related Topics & Resources

* Click the PDF download link under 'Related Topics' to access the presentation of this report.

* Click this link to watch the YouTube video.

About HDIN Research

HDIN Research (www.hdinresearch.com) is a premier provider of institutional-grade market intelligence, specializing in deep-tech, semiconductor, and industrial supply chain forensic analysis.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*

Financial Health & Operational Moats: The Software Premium vs. Hardware Catch-Up

The 2025 fiscal filings reveal a stark divergence in capital allocation frameworks. Top-tier legacy players are abandoning the physical hardware dogfight, utilizing accretive acquisitions to secure protocol-layer monopolies.

Keysight Technologies (NYSE: KEYS) reported $5.375 billion in top-line revenue with a commanding 62.1% gross margin. Rather than defending lower-band frequency markets, Keysight deployed $1.007 billion in R&D (18.7% intensity) toward 1.6Tb/sec Ethernet and 6G physical layer testing. More critically, its $1.415 billion acquisition of Spirent and the buyout of Synopsys’ Optical Solutions Group signal a terminal shift: Keysight is transitioning from a box-seller to an AI-cluster simulation gatekeeper, locking hyperscalers into high-margin recurring software revenue.

Conversely, the Chinese dual-oligopoly is executing an aggressive vertical integration strategy to break Western bandwidth embargoes. Rigol Technologies (SHA: 688337) successfully commercialized its "Cassiopeia" ASIC platform, driving its digital oscilloscope bandwidth to 13GHz. While Rigol posted a 16.04% revenue growth ($125.25 million), the firm suffered acute margin compression, with core gross margins contracting 4.14% to 55.62%. This compression reflects the high initial CapEx payload of semiconductor self-reliance and the dilution from educational bulk-tender pricing.

Siglent Technologies (SHA: 688138) opted for a premium-tier skimming strategy. By launching the SDS8204A 20GHz oscilloscope and 50GHz VNAs, high-end product sales surged 57.14%. This insulated Siglent from the pricing floor, resulting in superior financial health: a 61.48% gross margin and an exceptional $25.09 million in operating cash flow (+52.76% YoY).

Figure TMI INDUSTRY 2025: THE GLOBAL SHIFT TO SOFTWARE-DEFINED INTELLIGENCE

Supply Chain Pivot: The Southeast Asian Cost-Pass-Through MechanismGeopolitical friction has forced an irreversible structural shift in the global T&M supply chain. The U.S. Section 301 tariffs and reciprocal trade barriers have rendered bilateral export models mathematically unviable.

In response, both Rigol and Siglent have executed a "China + 1" localization mandate. Rigol directed $8.50 million in CapEx toward its Penang, Malaysia manufacturing hub, which is currently enduring a costly capacity ramp-up phase. Siglent’s corresponding Penang facility officially went online in April 2025.

Standard market models interpret these moves as simple capacity expansion. In reality, these Southeast Asian facilities act as critical cost-pass-through mechanisms. By routing final assembly through Malaysia, Chinese T&M firms bypass U.S. import penalties, protecting their pricing parity against domestic American competitors. However, until these facilities achieve scale, expect localized inventory de-stocking turbulence and elevated freight costs to drag on quarterly earnings.

HDIN Institutional Perspective: Capital Allocation Errors and Sector Divergence

Reviewing the 10-K disclosures through a macroeconomic lens exposes a violent sector rotation. The capital market's honeymoon phase with Advanced Mobility (EV) testing has cratered, replaced entirely by AI infrastructure CapEx.

The collateral damage is evident in Ralliant (NYSE: RLI). The former Fortive spin-off recognized a catastrophic $1.44 billion non-cash goodwill impairment in Q4 2025 related to its EA Elektro-Automatik unit. This impairment is a direct downstream consequence of delayed EV adoption curves, drastically elongating the payback period on its high-power bidirectional EV testing equipment. Compounded by a $32.7 million interest burden (5.5% effective rate) on its debt, Ralliant exemplifies the terminal risk of over-leveraging into cyclical hardware trends.

Simultaneously, Teledyne (NYSE: TDY) and AMETEK (NYSE: AME) are playing a high-wire M&A game. Teledyne carries $8.688 billion in goodwill after acquiring Qioptiq, while AMETEK dropped $933.2 million cash for Kern Microtechnik and FARO Technologies. While defense electronics (up 36.3% for Teledyne) mask current balance sheet bloat, any macroeconomic contraction will expose these firms to the exact impairment guillotine Ralliant just suffered.

The 2026 Street Outlook: Hardware parameters are no longer the ultimate moat. Investors must rotate equity exposure toward T&M entities exhibiting software revenue stickiness and immune-grade supply chains. Rigol’s 25.09% R&D intensity will either yield a monopolistic ASIC dividend in 2026 or burn its remaining cash runway. Meanwhile, Keysight’s transformation into an AI interconnect software firm makes its current multiple historically defensible.

Related Topics & Resources

* Click the PDF download link under 'Related Topics' to access the presentation of this report.

* Click this link to watch the YouTube video.

About HDIN Research

HDIN Research (www.hdinresearch.com) is a premier provider of institutional-grade market intelligence, specializing in deep-tech, semiconductor, and industrial supply chain forensic analysis.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*