Trinomab Faces 10.7-Month Liquidity Runway as TNM002 NRDL Execution Triggers Margin Compression in FY2026

Date : 2026-04-06

Reading : 188

Trinomab’s 2026 transition to a commercial-stage biopharma is threatened by a critical 10.7-month liquidity cliff. As its flagship TNM002 faces NRDL-mandated price cuts in China, surging debt and CDE regulatory friction regarding TNM001’s data extrapolation risk derailing the company's $216 million IPO and 2029 breakeven target.

Figure TRINOMAB 2025: THE STRATEGIC LEAP FROM R&D TO COMMERCIALIZATION

Financial Health & Operational Moats: The 10.7-Month Liquidity Cliff

Financial Health & Operational Moats: The 10.7-Month Liquidity Cliff

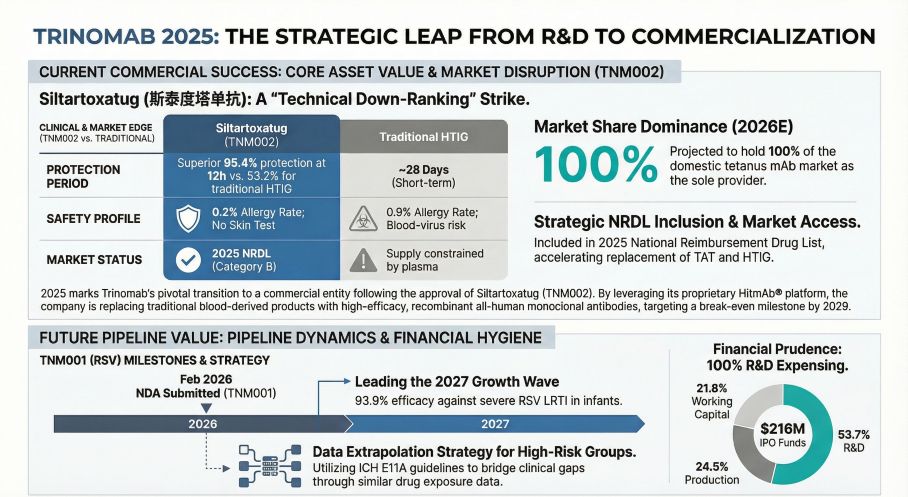

Trinomab is currently trapped in a tight liquidity bottleneck, operating with a cash bleed that fundamentally outpaces its commercial ramp-up. Based on our audit of the FY2025 prospectus, the company recorded a net loss of $83.66 million against a dwindling cash reserve of $71.70 million. Assuming flat operating expenses and zero capital injections, the corporate runway expires in exactly 10.7 months.

This balance sheet fragility is exacerbated by a $31.75 million short-term non-current liability cliff maturing within 12 months. Furthermore, Trinomab is suffering severe margin compression. FY2025 gross margins languished at 43.51%—an anomaly for the biologics sector—driven directly by $2.15 million in idle capacity costs aggressively hitting the cost of goods sold (COGS). While the inclusion of its first-in-class tetanus monoclonal antibody, TNM002, in the 2025 National Reimbursement Drug List (NRDL) guarantees structural volume access, the mandated 70% reimbursement ratio dictates steep unit-price concessions. This "price-for-volume" exchange threatens to prolong the timeline to cross the breakeven threshold, especially since 2025 revenues for TNM002 stalled at a mere $7.12 million (159,000 vials).

Regulatory Friction & The TNM001 "Extrapolation" Gamble

The pipeline’s secondary growth engine, TNM001 (RSV mAb), presents a binary regulatory catalyst for 2027. While the Phase III TNM001-301 trial successfully hit primary endpoints for non-high-risk infants, the TNM001-302 trial targeting the high-risk demographic missed statistical significance (P=0.1654).

Instead of initiating a cost-prohibitive salvage trial, management is deploying a high-stakes "data extrapolation" strategy referencing the ICH E11A guidelines, banking on similar drug exposure metrics (21.2 μg/mL vs. 21.0 μg/mL at day 150). If the Center for Drug Evaluation (CDE) rejects this pediatric extrapolation, TNM001’s addressable market will be structurally handicapped. Our DCF models indicate an outright rejection in the high-risk cohort would trigger a 20% to 30% downward revision in free cash flow projections for the 2027-2032 cycle.

Supply Chain Pivot: Capital Expenditure Allocation and Capacity Absorption

To circumvent margin decay, Trinomab intends to deploy $53 million (24.5% of its $216 million IPO proceeds) into upgrading its manufacturing base. This CAPEX targets the construction of the GMP-compliant DS3 facility (adding 140kg of drug substance capacity) and the DP3 formulation line (scaling to 4 million Pre-Filled Syringes).

Strategically, the shift toward a PFS lifecycle management strategy aims to defend unit economics against looming Volume-Based Procurement (VBP) risks. With domestic competitors like Zhixiang Jintai (GR2001) already at the NDA stage, a three-player market configuration will almost certainly trigger national VBP integration. We project VBP inclusion would enforce an up to 90% price erosion, making vertical integration and ultra-high titer yields (currently ~7g/L for TNM002 on the HitmAb® platform) the absolute baseline for survival.

HDIN Institutional Perspective: A Canary in the Biopharma Coal Mine

Trinomab represents a macro read-through for China's pre-revenue biotechs attempting the perilous leap to commercial biopharma. The company’s net assets have cratered from $99.10 million in FY2023 to $14.42 million by FY2025.

More critically, cross-border clinical aspirations are colliding with geopolitical realities. FDA Fast Track designation for TNM002 requires a localized US RCT, demanding $50 million to $100 million in offshore CAPEX. Concurrently, data export compliance under China’s Human Genetic Resources regulations introduces massive operational drag. If the IPO fails or stalls, it will trigger Series C equity buyback clauses executed by the actual controllers, potentially catalyzing a hard default. Institutional investors must track Q1/Q2 2026 hospital procurement cycle velocities for TNM002 as the definitive leading indicator of corporate solvency.

Presentation download:

*Click the PDF download link under 'Related Topics' to access the presentation of this report.*

*Click this link to watch the YouTube video breaking down Trinomab's Phase 3 clinical data extrapolation risk.*

About HDIN Research:

HDIN Research is a premier financial intelligence and strategic advisory firm delivering institutional-grade market analysis. We specialize in penetrating corporate filings to extract asymmetric insights for asset managers and equity desks worldwide. (www.hdinresearch.com)

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*

Figure TRINOMAB 2025: THE STRATEGIC LEAP FROM R&D TO COMMERCIALIZATION

Financial Health & Operational Moats: The 10.7-Month Liquidity CliffTrinomab is currently trapped in a tight liquidity bottleneck, operating with a cash bleed that fundamentally outpaces its commercial ramp-up. Based on our audit of the FY2025 prospectus, the company recorded a net loss of $83.66 million against a dwindling cash reserve of $71.70 million. Assuming flat operating expenses and zero capital injections, the corporate runway expires in exactly 10.7 months.

This balance sheet fragility is exacerbated by a $31.75 million short-term non-current liability cliff maturing within 12 months. Furthermore, Trinomab is suffering severe margin compression. FY2025 gross margins languished at 43.51%—an anomaly for the biologics sector—driven directly by $2.15 million in idle capacity costs aggressively hitting the cost of goods sold (COGS). While the inclusion of its first-in-class tetanus monoclonal antibody, TNM002, in the 2025 National Reimbursement Drug List (NRDL) guarantees structural volume access, the mandated 70% reimbursement ratio dictates steep unit-price concessions. This "price-for-volume" exchange threatens to prolong the timeline to cross the breakeven threshold, especially since 2025 revenues for TNM002 stalled at a mere $7.12 million (159,000 vials).

Regulatory Friction & The TNM001 "Extrapolation" Gamble

The pipeline’s secondary growth engine, TNM001 (RSV mAb), presents a binary regulatory catalyst for 2027. While the Phase III TNM001-301 trial successfully hit primary endpoints for non-high-risk infants, the TNM001-302 trial targeting the high-risk demographic missed statistical significance (P=0.1654).

Instead of initiating a cost-prohibitive salvage trial, management is deploying a high-stakes "data extrapolation" strategy referencing the ICH E11A guidelines, banking on similar drug exposure metrics (21.2 μg/mL vs. 21.0 μg/mL at day 150). If the Center for Drug Evaluation (CDE) rejects this pediatric extrapolation, TNM001’s addressable market will be structurally handicapped. Our DCF models indicate an outright rejection in the high-risk cohort would trigger a 20% to 30% downward revision in free cash flow projections for the 2027-2032 cycle.

Supply Chain Pivot: Capital Expenditure Allocation and Capacity Absorption

To circumvent margin decay, Trinomab intends to deploy $53 million (24.5% of its $216 million IPO proceeds) into upgrading its manufacturing base. This CAPEX targets the construction of the GMP-compliant DS3 facility (adding 140kg of drug substance capacity) and the DP3 formulation line (scaling to 4 million Pre-Filled Syringes).

Strategically, the shift toward a PFS lifecycle management strategy aims to defend unit economics against looming Volume-Based Procurement (VBP) risks. With domestic competitors like Zhixiang Jintai (GR2001) already at the NDA stage, a three-player market configuration will almost certainly trigger national VBP integration. We project VBP inclusion would enforce an up to 90% price erosion, making vertical integration and ultra-high titer yields (currently ~7g/L for TNM002 on the HitmAb® platform) the absolute baseline for survival.

HDIN Institutional Perspective: A Canary in the Biopharma Coal Mine

Trinomab represents a macro read-through for China's pre-revenue biotechs attempting the perilous leap to commercial biopharma. The company’s net assets have cratered from $99.10 million in FY2023 to $14.42 million by FY2025.

More critically, cross-border clinical aspirations are colliding with geopolitical realities. FDA Fast Track designation for TNM002 requires a localized US RCT, demanding $50 million to $100 million in offshore CAPEX. Concurrently, data export compliance under China’s Human Genetic Resources regulations introduces massive operational drag. If the IPO fails or stalls, it will trigger Series C equity buyback clauses executed by the actual controllers, potentially catalyzing a hard default. Institutional investors must track Q1/Q2 2026 hospital procurement cycle velocities for TNM002 as the definitive leading indicator of corporate solvency.

Presentation download:

*Click the PDF download link under 'Related Topics' to access the presentation of this report.*

*Click this link to watch the YouTube video breaking down Trinomab's Phase 3 clinical data extrapolation risk.*

About HDIN Research:

HDIN Research is a premier financial intelligence and strategic advisory firm delivering institutional-grade market analysis. We specialize in penetrating corporate filings to extract asymmetric insights for asset managers and equity desks worldwide. (www.hdinresearch.com)

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*