Arrow Electronics Accelerates Cloud Integration as APAC Distribution Margins Compress to 4.68% in FY2025

Date : 2026-04-02

Reading : 259

In FY2025, global electronic component distributors—led by Arrow (NYSE: ARW) and Avnet (Nasdaq: AVT)—aggressively pivoted toward high-margin enterprise computing architectures across Western markets, offsetting profound margin compression and legacy inventory de-stocking that have trapped APAC-centric players in severe liquidity and compliance bottlenecks.

Figure 2025 Global Semiconductor Distribution: Market Tiers & 2026 Strategic Outlook

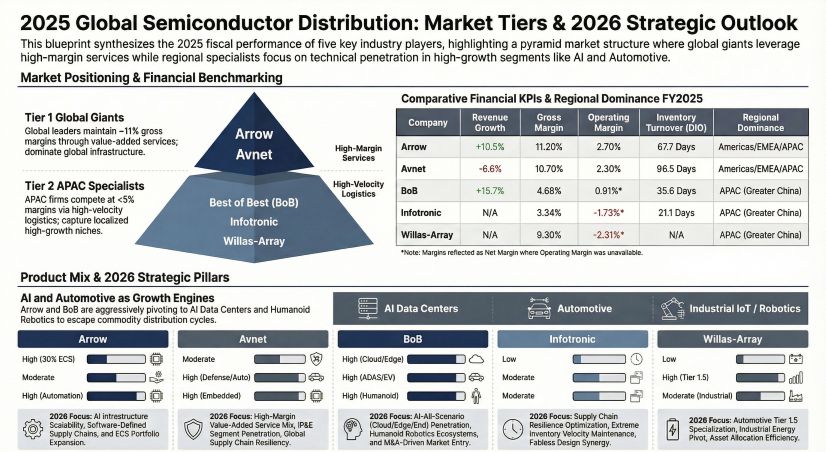

Financial Health & Operational Moats: The Great Bifurcation

Financial Health & Operational Moats: The Great Bifurcation

An audit of FY2025 10-K and annual filings reveals a brutal two-tiered reality in the global semiconductor distribution channel. The strategic moat no longer lies in warehousing volume, but in software-defined engineering integration.

Arrow Electronics (NYSE: ARW) has successfully insulated its balance sheet from cyclical hardware volatility. By driving its Enterprise Computing Solutions (ECS) division to 30% of total revenue ($30.85 billion), Arrow delivered a robust 11.2% gross margin. This 17.8% YoY growth in ECS—anchored by data center infrastructure and ArrowSphere cloud services—proves that embedding engineering value is the only viable defense against hardware commoditization. Similarly, Avnet (Nasdaq: AVT) sustained a 10.7% gross margin by leaning on its Farnell unit, capturing extreme premiums in low-volume, R&D-stage fulfillment.

Conversely, APAC regional distributors are bleeding out in the volume trenches, suffering severe margin compression as they act as shock absorbers for upstream foundries. Best of Best (BOB, SZSE: 001298) reported a 152.79% surge in net profit ($10.60 million) on $1.16 billion in revenue, but a forensic look at its cash flow reveals a classic working capital trap. BOB’s Operating Cash Flow (OCF) collapsed to -$55.08 million. This "paper wealth" signals that top-line growth is being force-fed through dangerously relaxed credit terms, leaving the firm highly vulnerable to downstream defaults.

The structural fragility is most acute at Infotronic (SZSE: 000670). Despite generating $660.6 million in revenue, the firm posted a net loss of $11.45 million, driven by a catastrophic 97.53% debt-to-asset ratio. Furthermore, Infotronic was forced to recognize a ¥38.89 million ($5.41 million) goodwill impairment related to its Shenzhen Huaxinke and World Style units, underscoring the failure of past acquisitions to generate synergistic cash flows during cyclical troughs.

Supply Chain Pivot: Geopolitical Realignment and Localization

The geographical footprint of component distribution is undergoing a violent restructuring, catalyzed by US Department of Commerce BIS "Entity List" restrictions and escalating tariff architectures. In response, supply chains are fracturing into regional silos.

For domestic Chinese players, survival hinges on deep vertical integration within the "Greater China" ecosystem. Best of Best has actively maneuvered into the domestic substitution trade, successfully penetrating the white goods sector with localized MCU replacements. Meanwhile, Willas-Array (HKEX: 0854) has systematically derisked its legacy industrial exposure by pivoting aggressively into Automotive Electronics, which now constitutes 30.2% of its $341.85 million revenue base. Through embedding Field Application Engineers (FAEs) directly with Tier 1 and Tier 2 EV suppliers, these localized entities are attempting to build defensive moats that global giants cannot easily replicate due to geopolitical friction.

HDIN Institutional Perspective: Masking the L-Shaped Trough

From an institutional vantage point, the FY2025 data confirms the semiconductor distribution market is scraping across an L-shaped bottom. AI server demand (specifically for logic chips and HBM) is camouflaging the underlying rot in legacy consumer electronics.

Investors must exercise extreme caution regarding accounting optical illusions engineered during this phase of the cycle. Willas-Array’s reported 9.3% gross margin is largely a mirage; adjusting for a HKD 46.3 million inventory provision reversal, core operating margin rests at a far weaker 7.3%.

Furthermore, historical cost-pass-through mechanisms have completely broken down for Tier-2 distributors. With upstream giants monopolizing pricing power, regional distributors lack the leverage to pass inflation or tariff costs to end-users. Moving into 2026, we expect a wave of accretive acquisitions as distressed, hyper-leveraged regional players (like Infotronic) are absorbed by better-capitalized entities seeking to acquire turnkey AI and robotics engineering teams on the cheap.

Strategic Actions & Downloads

* Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

* Video Link: Click this link to watch the YouTube video breaking down the FY2025 cash flow anomalies.

About HDIN Research

HDIN Research (www.hdinresearch.com) is a premier provider of institutional-grade market intelligence, specializing in forensic financial analysis, supply chain architecture, and geopolitical risk assessment within the global technology and semiconductor sectors.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*

Figure 2025 Global Semiconductor Distribution: Market Tiers & 2026 Strategic Outlook

Financial Health & Operational Moats: The Great BifurcationAn audit of FY2025 10-K and annual filings reveals a brutal two-tiered reality in the global semiconductor distribution channel. The strategic moat no longer lies in warehousing volume, but in software-defined engineering integration.

Arrow Electronics (NYSE: ARW) has successfully insulated its balance sheet from cyclical hardware volatility. By driving its Enterprise Computing Solutions (ECS) division to 30% of total revenue ($30.85 billion), Arrow delivered a robust 11.2% gross margin. This 17.8% YoY growth in ECS—anchored by data center infrastructure and ArrowSphere cloud services—proves that embedding engineering value is the only viable defense against hardware commoditization. Similarly, Avnet (Nasdaq: AVT) sustained a 10.7% gross margin by leaning on its Farnell unit, capturing extreme premiums in low-volume, R&D-stage fulfillment.

Conversely, APAC regional distributors are bleeding out in the volume trenches, suffering severe margin compression as they act as shock absorbers for upstream foundries. Best of Best (BOB, SZSE: 001298) reported a 152.79% surge in net profit ($10.60 million) on $1.16 billion in revenue, but a forensic look at its cash flow reveals a classic working capital trap. BOB’s Operating Cash Flow (OCF) collapsed to -$55.08 million. This "paper wealth" signals that top-line growth is being force-fed through dangerously relaxed credit terms, leaving the firm highly vulnerable to downstream defaults.

The structural fragility is most acute at Infotronic (SZSE: 000670). Despite generating $660.6 million in revenue, the firm posted a net loss of $11.45 million, driven by a catastrophic 97.53% debt-to-asset ratio. Furthermore, Infotronic was forced to recognize a ¥38.89 million ($5.41 million) goodwill impairment related to its Shenzhen Huaxinke and World Style units, underscoring the failure of past acquisitions to generate synergistic cash flows during cyclical troughs.

Supply Chain Pivot: Geopolitical Realignment and Localization

The geographical footprint of component distribution is undergoing a violent restructuring, catalyzed by US Department of Commerce BIS "Entity List" restrictions and escalating tariff architectures. In response, supply chains are fracturing into regional silos.

For domestic Chinese players, survival hinges on deep vertical integration within the "Greater China" ecosystem. Best of Best has actively maneuvered into the domestic substitution trade, successfully penetrating the white goods sector with localized MCU replacements. Meanwhile, Willas-Array (HKEX: 0854) has systematically derisked its legacy industrial exposure by pivoting aggressively into Automotive Electronics, which now constitutes 30.2% of its $341.85 million revenue base. Through embedding Field Application Engineers (FAEs) directly with Tier 1 and Tier 2 EV suppliers, these localized entities are attempting to build defensive moats that global giants cannot easily replicate due to geopolitical friction.

HDIN Institutional Perspective: Masking the L-Shaped Trough

From an institutional vantage point, the FY2025 data confirms the semiconductor distribution market is scraping across an L-shaped bottom. AI server demand (specifically for logic chips and HBM) is camouflaging the underlying rot in legacy consumer electronics.

Investors must exercise extreme caution regarding accounting optical illusions engineered during this phase of the cycle. Willas-Array’s reported 9.3% gross margin is largely a mirage; adjusting for a HKD 46.3 million inventory provision reversal, core operating margin rests at a far weaker 7.3%.

Furthermore, historical cost-pass-through mechanisms have completely broken down for Tier-2 distributors. With upstream giants monopolizing pricing power, regional distributors lack the leverage to pass inflation or tariff costs to end-users. Moving into 2026, we expect a wave of accretive acquisitions as distressed, hyper-leveraged regional players (like Infotronic) are absorbed by better-capitalized entities seeking to acquire turnkey AI and robotics engineering teams on the cheap.

Strategic Actions & Downloads

* Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

* Video Link: Click this link to watch the YouTube video breaking down the FY2025 cash flow anomalies.

About HDIN Research

HDIN Research (www.hdinresearch.com) is a premier provider of institutional-grade market intelligence, specializing in forensic financial analysis, supply chain architecture, and geopolitical risk assessment within the global technology and semiconductor sectors.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*