Fine Motion Accelerates Capacity Expansion as Domestic RV Reducer Market Share Hits 24.98%

Date : 2026-04-03

Reading : 666

Zhejiang Fine Motion (spinoff of SZSE: 002472) is restructuring the global robotics supply chain via a $195.86 million IPO in China. This 2026 capital injection targets a Yuhuan base expansion to 460,000 units, breaking Nabtesco's monopoly amidst intense margin compression from domestic Tier-1 OEMs.

1. Financial Health & Operational Moats

Margin Compression and the High-Payload Defense

Fine Motion’s underlying financial architecture reveals a textbook case of upstream vulnerability transitioning into product-mix resilience. In 2024, aggressive cost-pass-through mechanisms from downstream integrators—specifically margin-squeezed robotics leaders like Estun and Efort—drove Fine Motion's RV reducer average selling price down by 9.89%. This exogenous shock resulted in acute margin compression, slashing gross margins from a 2023 high of 42.47% to 35.36%.

However, the 2025 prospectus data indicates a stabilization. By pivoting toward high-payload, high-rigidity RV reducers, the company engineered a margin recovery to 36.57%. A critical operational moat lies in their emerging harmonic drive segment, which generated $4.69 million (7.72% of total revenue) in 2025 but commanded a superior gross margin of 41.75%.

Liquidity Squeeze: The Receivables Turnover Paradox

Despite top-line resilience ($60.93 million total estimated 2025 revenue), the balance sheet flags a structural deterioration in bargaining power. Receivables turnover has aggressively decelerated from 2.85x in 2023 to 1.55x in 2025. With a 93.30% year-over-year spike in accounts receivable at the end of 2024—vastly outpacing the 10.27% revenue growth—it is evident Fine Motion is extending highly accommodative credit terms to defend its market share against both domestic peer Zhongdalide and Japanese incumbents.

Figure Fine Motion: Engineering the Precision Revolution in Global Robotics

2. Supply Chain Pivot

2. Supply Chain Pivot

The Yuhuan Base CAPEX and Vertical Integration

Operating at a severely constrained 108.14% capacity utilization in 2025, Fine Motion’s $195.86 million IPO is less about market entry and entirely about eliminating a critical production bottleneck. The lion's share of the raise—$153.18 million—is allocated to the Yuhuan manufacturing base (26,215.89 sq. meters). This targeted CAPEX will add 320,000 sets of RV reducers to the pipeline, effectively tripling total annual capacity to 460,000 units by the end of the 24-month build cycle.

De-risking the Feedstock and Breaking Monopolies

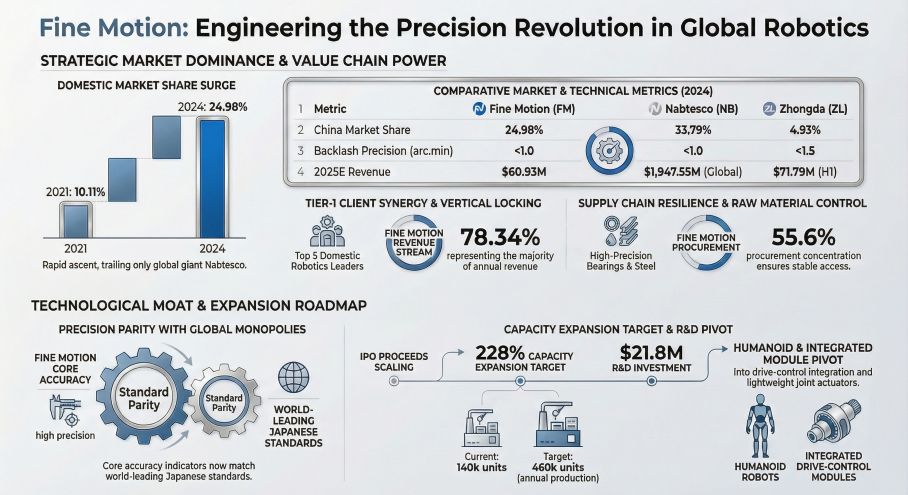

The company’s market share trajectory represents a structural pivot in the global robotics supply chain. Nabtesco’s historical grip on the Chinese market has eroded from 51.77% in 2021 to 33.79% in 2024, directly mirrored by Fine Motion’s ascent to 24.98%. However, raw material supply chain risks remain palpable. Fine Motion relies heavily on external vendors for high-precision bearings and specialized steel, with its top supplier accounting for $4.79 million (21.00% of procurement) in 2025. This localized dependency exposes the firm to macro-commodity fluctuations that their current pricing power cannot easily absorb.

3. HDIN Institutional Perspective

Fine Motion is currently navigating the "deep water" zone of import substitution. The engineering pedigree of its executive suite—heavily drawn from parent company Shuanghuan Transmission [SZSE: 002472]—has undeniably secured technological parity with Japanese peers, boasting internal precision tolerances tighter than 0.7 arc-minutes.

Yet, from an institutional vantage point, the firm's extreme customer concentration is a systemic vulnerability. With 78.34% of 2025 revenue tethered to its Top 5 clients—and a staggering 48.56% consolidated with a single Tier-1 domestic robotics leader—Fine Motion functions more as an outsourced manufacturing arm for its key client than an independent, diversified component supplier.

Furthermore, the strategic allocation of $21.81 million toward a mechatronics R&D center indicates management’s anticipation of a secular technological shift. As the industry flirts with direct-drive motors and integrated joint modules for humanoid robots, Fine Motion's pivot from standalone RV reducers to electro-mechanical integrated actuators is not just accretive—it is an existential requirement to prevent their current $56.09 million RV cash cow from becoming obsolete over the next hardware cycle. Additionally, reliance on state subsidies—which constituted 25.30% of total profits in 2025 ($3.75 million)—highlights a fragile earnings quality that must be organically replaced by the harmonic reducer commercialization expected in 2026.

Related Topics & Downloads

* Click the PDF download link under 'Related Topics' to access the presentation of this report.

* Click this link to watch the YouTube video.

About HDIN Research

HDIN Research is a premier intelligence and advisory firm dedicated to institutional-grade analysis of global industrial, technological, and macroeconomic supply chains. For more deep-dive financial forensics and strategy reports, visit www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*

1. Financial Health & Operational Moats

Margin Compression and the High-Payload Defense

Fine Motion’s underlying financial architecture reveals a textbook case of upstream vulnerability transitioning into product-mix resilience. In 2024, aggressive cost-pass-through mechanisms from downstream integrators—specifically margin-squeezed robotics leaders like Estun and Efort—drove Fine Motion's RV reducer average selling price down by 9.89%. This exogenous shock resulted in acute margin compression, slashing gross margins from a 2023 high of 42.47% to 35.36%.

However, the 2025 prospectus data indicates a stabilization. By pivoting toward high-payload, high-rigidity RV reducers, the company engineered a margin recovery to 36.57%. A critical operational moat lies in their emerging harmonic drive segment, which generated $4.69 million (7.72% of total revenue) in 2025 but commanded a superior gross margin of 41.75%.

Liquidity Squeeze: The Receivables Turnover Paradox

Despite top-line resilience ($60.93 million total estimated 2025 revenue), the balance sheet flags a structural deterioration in bargaining power. Receivables turnover has aggressively decelerated from 2.85x in 2023 to 1.55x in 2025. With a 93.30% year-over-year spike in accounts receivable at the end of 2024—vastly outpacing the 10.27% revenue growth—it is evident Fine Motion is extending highly accommodative credit terms to defend its market share against both domestic peer Zhongdalide and Japanese incumbents.

Figure Fine Motion: Engineering the Precision Revolution in Global Robotics

2. Supply Chain PivotThe Yuhuan Base CAPEX and Vertical Integration

Operating at a severely constrained 108.14% capacity utilization in 2025, Fine Motion’s $195.86 million IPO is less about market entry and entirely about eliminating a critical production bottleneck. The lion's share of the raise—$153.18 million—is allocated to the Yuhuan manufacturing base (26,215.89 sq. meters). This targeted CAPEX will add 320,000 sets of RV reducers to the pipeline, effectively tripling total annual capacity to 460,000 units by the end of the 24-month build cycle.

De-risking the Feedstock and Breaking Monopolies

The company’s market share trajectory represents a structural pivot in the global robotics supply chain. Nabtesco’s historical grip on the Chinese market has eroded from 51.77% in 2021 to 33.79% in 2024, directly mirrored by Fine Motion’s ascent to 24.98%. However, raw material supply chain risks remain palpable. Fine Motion relies heavily on external vendors for high-precision bearings and specialized steel, with its top supplier accounting for $4.79 million (21.00% of procurement) in 2025. This localized dependency exposes the firm to macro-commodity fluctuations that their current pricing power cannot easily absorb.

3. HDIN Institutional Perspective

Fine Motion is currently navigating the "deep water" zone of import substitution. The engineering pedigree of its executive suite—heavily drawn from parent company Shuanghuan Transmission [SZSE: 002472]—has undeniably secured technological parity with Japanese peers, boasting internal precision tolerances tighter than 0.7 arc-minutes.

Yet, from an institutional vantage point, the firm's extreme customer concentration is a systemic vulnerability. With 78.34% of 2025 revenue tethered to its Top 5 clients—and a staggering 48.56% consolidated with a single Tier-1 domestic robotics leader—Fine Motion functions more as an outsourced manufacturing arm for its key client than an independent, diversified component supplier.

Furthermore, the strategic allocation of $21.81 million toward a mechatronics R&D center indicates management’s anticipation of a secular technological shift. As the industry flirts with direct-drive motors and integrated joint modules for humanoid robots, Fine Motion's pivot from standalone RV reducers to electro-mechanical integrated actuators is not just accretive—it is an existential requirement to prevent their current $56.09 million RV cash cow from becoming obsolete over the next hardware cycle. Additionally, reliance on state subsidies—which constituted 25.30% of total profits in 2025 ($3.75 million)—highlights a fragile earnings quality that must be organically replaced by the harmonic reducer commercialization expected in 2026.

Related Topics & Downloads

* Click the PDF download link under 'Related Topics' to access the presentation of this report.

* Click this link to watch the YouTube video.

About HDIN Research

HDIN Research is a premier intelligence and advisory firm dedicated to institutional-grade analysis of global industrial, technological, and macroeconomic supply chains. For more deep-dive financial forensics and strategy reports, visit www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*