iRay Technology Accelerates Vertical Integration as Varex Absorbs $93.9M Impairment Shock in FY2025

Date : 2026-04-03

Reading : 163

In FY2025, global FPD manufacturers pivoted aggressively toward full-imaging ecosystem integration to counter tariff-driven margin compression. As Varex Imaging absorbed massive geopolitical impairments in China, Asian rivals like iRay Technology and Vieworks deployed regional CAPEX into CZT and CMOS manufacturing hubs to secure localized supply chains.

Financial Health & Operational Moats: The Cost of Geopolitical Drag

The 2025 fiscal year exposed a brutal divergence in capital efficiency across the Flat Panel Detector (FPD) ecosystem. The traditional a-Si (amorphous silicon) medical DR market has officially entered a cyclical trough, forcing a structural bifurcation between legacy hardware suppliers and full-stack innovators.

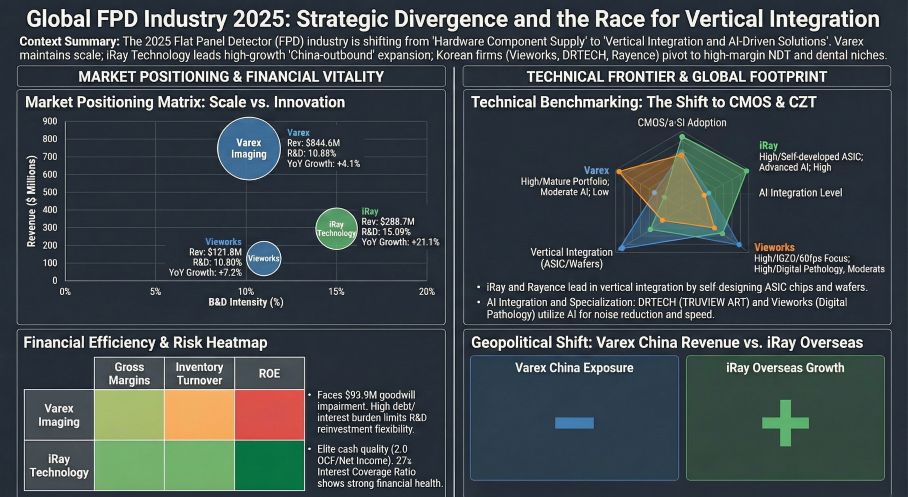

Varex Imaging (NASDAQ: VREX) serves as the primary cautionary tale. Despite top-line revenues of $844.6 million, the company’s balance sheet cracked under severe margin compression. Varex recorded a $93.9 million goodwill impairment, explicitly tied to its medical reporting unit's exposure to Chinese geopolitical headwinds. More alarmingly, rather than executing healthy inventory de-stocking, Varex saw inventory levels swell by $46.5 million to a bloated $330 million (a sluggish 1.79x turnover). Management framed this as strategic buffering against tariff shocks, but with $35.5 million in interest expenses devouring operating cash flow, Varex’s leverage ratio severely limits its R&D runway for next-generation photon-counting technologies.

Conversely, iRay Technology (SHA: 688301) engineered a masterclass in capital allocation. By maintaining a 15.09% R&D-to-revenue ratio ($47.26 million), iRay shielded itself from raw material price wars. This capital generated a 21.13% revenue surge to $288.67 million. Crucially, iRay operates with an Operating Cash Flow to Net Income ratio of 2.0—a pristine indicator of earnings quality that standardizes their ability to fund aggressive vertical integration without relying on toxic debt.

Figure Global FPD Industry 2025: Strategic Divergence and the Race for Vertical Integration

Supply Chain Pivot: Escaping the MOFCOM Crosshairs

Supply Chain Pivot: Escaping the MOFCOM Crosshairs

The invisible hand dictating 2025’s FPD supply chain was regulatory friction, specifically the EU’s MDR compliance delays and the looming threat of the Chinese Ministry of Commerce (MOFCOM) anti-dumping probe into imported CT tubes.

To survive, manufacturers abandoned the globalized export model in favor of localized redundancy. Varex's vulnerability to US-China tariffs forced it into defensive local sourcing, lacking robust cost-pass-through mechanisms to insulate gross margins from semiconductor price hikes.

Asian players moved offensively. iRay Technology recognized that independent detector suppliers would be squeezed out by domestic procurement mandates. Consequently, iRay deployed $217 million (1.56 billion RMB) into its Haining Phase II CAPEX project, specifically targeting the localized production of CT tubes and high-voltage generators. Simultaneously, iRay committed $250 million (1.8 billion RMB) to its Hefei Base. This is not merely a capacity expansion; it is a profound pivot into silicon-based OLED microdisplays (exceeding 4000 PPI), directly inserting iRay into the AI-wearable supply chain and bypassing healthcare procurement bottlenecks entirely.

In South Korea, Vieworks (KOSDAQ: 100120) executed a parallel defensive maneuver. Recognizing that AI-driven semiconductor reallocation was inflating raw material costs for medical detectors, Vieworks leaned heavily into its industrial NDT (Non-Destructive Testing) portfolio. By capitalizing on the booming HBM (High Bandwidth Memory) semiconductor inspection market, Vieworks maintained $121.78 million in revenue, securing high-margin industrial contracts to offset medical pricing headwinds.

HDIN Institutional Perspective: A M&A Supercycle on the Horizon

At HDIN Research, our reading of the 2025 filings suggests the FPD sector has crossed the Rubicon. The liquidation of Rayence’s (KOSDAQ: 228850) China subsidiary and its subsequent $3.73 million net loss proves that mid-tier players lacking proprietary ASIC or scintillator manufacturing capabilities will not survive the current macro environment.

We anticipate the industry is transitioning from an organic growth phase into a consolidation era. Well-capitalized entities like iRay and Vieworks are uniquely positioned to execute accretive acquisitions, specifically targeting distressed niche developers possessing intellectual property in CZT (Cadmium Zinc Telluride) photon-counting algorithms or flexible substrate manufacturing (an area pioneered by DRTECH). Varex’s massive installed base remains a formidable moat, but unless it can restructure its debt and localize production faster than MOFCOM policy shifts, it risks becoming a structural donor of market share to vertically integrated challengers.

Presentation download:

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research:

HDIN Research is a premier market intelligence and strategic advisory firm specializing in advanced med-tech, semiconductor supply chains, and industrial automation. We decode complex corporate filings and macroeconomic shifts into actionable Alpha for institutional investors and corporate strategists. Visit us at www.hdinresearch.com.

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.

Financial Health & Operational Moats: The Cost of Geopolitical Drag

The 2025 fiscal year exposed a brutal divergence in capital efficiency across the Flat Panel Detector (FPD) ecosystem. The traditional a-Si (amorphous silicon) medical DR market has officially entered a cyclical trough, forcing a structural bifurcation between legacy hardware suppliers and full-stack innovators.

Varex Imaging (NASDAQ: VREX) serves as the primary cautionary tale. Despite top-line revenues of $844.6 million, the company’s balance sheet cracked under severe margin compression. Varex recorded a $93.9 million goodwill impairment, explicitly tied to its medical reporting unit's exposure to Chinese geopolitical headwinds. More alarmingly, rather than executing healthy inventory de-stocking, Varex saw inventory levels swell by $46.5 million to a bloated $330 million (a sluggish 1.79x turnover). Management framed this as strategic buffering against tariff shocks, but with $35.5 million in interest expenses devouring operating cash flow, Varex’s leverage ratio severely limits its R&D runway for next-generation photon-counting technologies.

Conversely, iRay Technology (SHA: 688301) engineered a masterclass in capital allocation. By maintaining a 15.09% R&D-to-revenue ratio ($47.26 million), iRay shielded itself from raw material price wars. This capital generated a 21.13% revenue surge to $288.67 million. Crucially, iRay operates with an Operating Cash Flow to Net Income ratio of 2.0—a pristine indicator of earnings quality that standardizes their ability to fund aggressive vertical integration without relying on toxic debt.

Figure Global FPD Industry 2025: Strategic Divergence and the Race for Vertical Integration

Supply Chain Pivot: Escaping the MOFCOM CrosshairsThe invisible hand dictating 2025’s FPD supply chain was regulatory friction, specifically the EU’s MDR compliance delays and the looming threat of the Chinese Ministry of Commerce (MOFCOM) anti-dumping probe into imported CT tubes.

To survive, manufacturers abandoned the globalized export model in favor of localized redundancy. Varex's vulnerability to US-China tariffs forced it into defensive local sourcing, lacking robust cost-pass-through mechanisms to insulate gross margins from semiconductor price hikes.

Asian players moved offensively. iRay Technology recognized that independent detector suppliers would be squeezed out by domestic procurement mandates. Consequently, iRay deployed $217 million (1.56 billion RMB) into its Haining Phase II CAPEX project, specifically targeting the localized production of CT tubes and high-voltage generators. Simultaneously, iRay committed $250 million (1.8 billion RMB) to its Hefei Base. This is not merely a capacity expansion; it is a profound pivot into silicon-based OLED microdisplays (exceeding 4000 PPI), directly inserting iRay into the AI-wearable supply chain and bypassing healthcare procurement bottlenecks entirely.

In South Korea, Vieworks (KOSDAQ: 100120) executed a parallel defensive maneuver. Recognizing that AI-driven semiconductor reallocation was inflating raw material costs for medical detectors, Vieworks leaned heavily into its industrial NDT (Non-Destructive Testing) portfolio. By capitalizing on the booming HBM (High Bandwidth Memory) semiconductor inspection market, Vieworks maintained $121.78 million in revenue, securing high-margin industrial contracts to offset medical pricing headwinds.

HDIN Institutional Perspective: A M&A Supercycle on the Horizon

At HDIN Research, our reading of the 2025 filings suggests the FPD sector has crossed the Rubicon. The liquidation of Rayence’s (KOSDAQ: 228850) China subsidiary and its subsequent $3.73 million net loss proves that mid-tier players lacking proprietary ASIC or scintillator manufacturing capabilities will not survive the current macro environment.

We anticipate the industry is transitioning from an organic growth phase into a consolidation era. Well-capitalized entities like iRay and Vieworks are uniquely positioned to execute accretive acquisitions, specifically targeting distressed niche developers possessing intellectual property in CZT (Cadmium Zinc Telluride) photon-counting algorithms or flexible substrate manufacturing (an area pioneered by DRTECH). Varex’s massive installed base remains a formidable moat, but unless it can restructure its debt and localize production faster than MOFCOM policy shifts, it risks becoming a structural donor of market share to vertically integrated challengers.

Presentation download:

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research:

HDIN Research is a premier market intelligence and strategic advisory firm specializing in advanced med-tech, semiconductor supply chains, and industrial automation. We decode complex corporate filings and macroeconomic shifts into actionable Alpha for institutional investors and corporate strategists. Visit us at www.hdinresearch.com.

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.