Consumer Battery Giants See Diverging Margins: CosMX and EVE Energy Accelerate Solid-State R&D Amid 57% Inventory Spikes

Date : 2026-04-06

Reading : 226

In FY2025, global battery giants including EVE Energy and CosMX executed massive supply chain pivots to Mexico and Hungary, battling margin compression from 171% cobalt price spikes. Driven by Edge AI hardware demands, top-tier players are accelerating solid-state R&D to bypass EU carbon regulations and secure North American IRA subsidies.

Financial Health & Operational Moats: The Illusion of High Earnings Quality

While the consumer battery sector displays ostensibly pristine cash flows—with EVE Energy (SZSE: 300014) and CosMX (SHSE: 688772) posting operating cash flow to net profit (OCF/NP) ratios of 1.81 and 4.42 respectively—a forensic audit of FY2025 filings reveals severe structural vulnerabilities. The industry is currently masking an acute liquidity "tight balance" under the guise of scale expansion.

CosMX is flashing red on liquidity metrics. With a debt-to-asset ratio expanding to 68.19% and a dangerously low quick ratio of 0.54, its short-term debt obligations ($309 million) eclipse available cash reserves. This aggressive leverage posture is fundamentally misaligned with its heavy reliance on the highly cyclical IT hardware market, rendering the company vulnerable if demand for AI PCs fails to offset margin compression.

Conversely, EVE Energy faces a pronounced inventory de-stocking risk. The company’s inventory book value surged 57% to $1.146 billion, doubling its 26% revenue growth rate. As cobalt prices experienced a vicious 171.66% upward reversion to roughly $55,400/MT by late 2025, delayed cost-pass-through mechanisms dictate that EVE will face formidable inventory impairment charges in FY2026 if downstream demand cools.

Meanwhile, retail-focused Anfu Tech (SHSE: 603031) sits on a demographic time bomb. Despite commanding a 50.71% gross margin via absolute channel dominance in China, its $404 million goodwill—comprising 40% of total assets—remains a toxic hangover from the Nanfu Battery acquisition. Stagnant revenue growth (2.94%) juxtaposed against looser credit terms (accounts receivable up 8.15%) indicates channel-stuffing fatigue, escalating the probability of an accretive acquisition turning into a massive writedown.

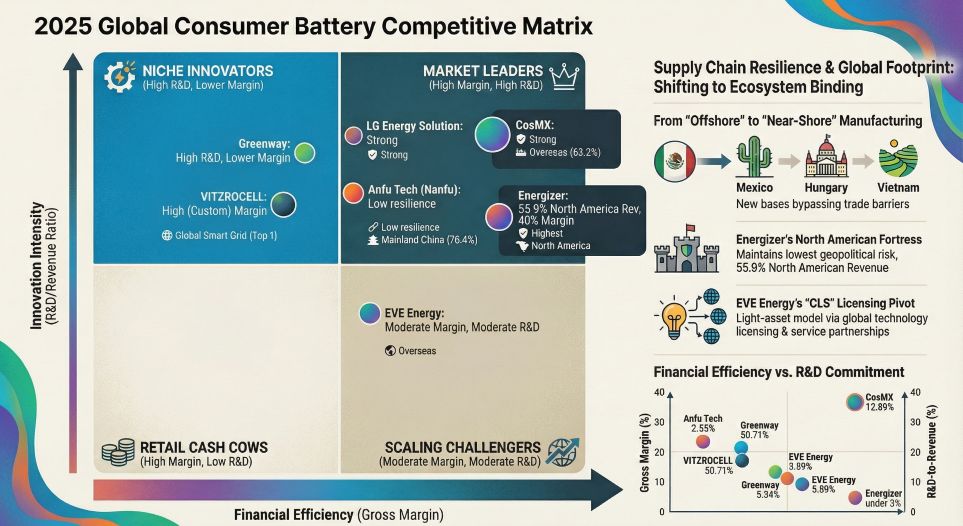

Supply Chain Pivot: Near-Shoring and the "Compliance Premium"

Geopolitical fragmentation has forced the industry out of its centralized manufacturing complacency. The narrative in FY2025 shifted definitively from "capacity out-migration" to "compliance-driven localization." The EU Battery Directive’s Digital Battery Passport and the US Inflation Reduction Act (IRA) have erected formidable non-tariff barriers, dictating a violent restructuring of global CAPEX.

LG Energy Solution (KRX: 373220) remains the apex predator of policy defense. Allocating a staggering $7.37 billion in CAPEX, primarily directed at US soil (Michigan, Ohio), LGES has successfully monopolized the compliance premium. By contrast, Chinese tier-one players are executing evasive near-shoring maneuvers. CosMX’s deployment of PACK assembly lines in Mexico serves as a strategic wedge into the North American IT supply chain, deliberately bypassing direct tariff hostilities while achieving a 43.42% self-supply rate in battery packs.

EVE Energy has abandoned standard export models altogether, pivoting to a capital-light "Cooperative Licensing & Service" (CLS) framework. By exporting production topology rather than physical cells—exemplified by the ACT joint venture in North America and its new Hungarian facility adjacent to BMW—EVE is effectively neutralizing the impact of China's impending 2027 export tax rebate cancellation. This vertical integration of service protocols rather than mere manufacturing output represents a critical evolutionary leap in circumventing US-Sino trade friction.

Figure 2025 Global Consumer Battery Competitive Matrix

HDIN Institutional Perspective: The AI Hardware Supercycle and Solid-State Inflection

HDIN Institutional Perspective: The AI Hardware Supercycle and Solid-State Inflection

The consumer battery sector is trapped in a transitional trough between legacy IT saturation and the Edge AI hardware supercycle. The integration of on-device LLMs (AI PCs and AI Phones) is not merely driving volume; it is forcing a thermodynamic reckoning. The deployment of Apple Intelligence and local AI architectures requires unprecedented pulse-discharge capabilities and extreme thermal management.

Here, CosMX has entrenched a formidable moat, achieving a commercialized silicon anode density of 900Wh/L. However, the ultimate endgame lies in solid-state commercialization. Both EVE Energy (with its Longquan No.2 10Ah solid-state rollout) and LGES have aggressively transitioned from R&D defense to disruptive disruption, pushing pilot lines into low-volume production.

We assess that players lacking direct exposure to either High-Silicon or Solid-State chemistry, such as Energizer (NYSE: ENR) with its anemic 1.1% R&D intensity, will face catastrophic market share erosion as consumer electronics manufacturers mandate next-generation thermal profiles. The divergence is clear: companies that successfully navigate the near-shoring CAPEX burden while simultaneously funding AI-compliant chemistry will capture the FY2026 upgrade cycle. Those relying purely on legacy distribution networks will be relegated to the low-margin, commoditized tail-end of the market.

Presentation download:

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research:

HDIN Research is a premier strategic advisory and equity intelligence firm bridging the gap between raw corporate disclosures and macroeconomic trends. We provide institutional investors with unvarnished, data-driven analysis on supply chain pivots, capital expenditures, and geopolitical regulatory impacts. Visit www.hdinresearch.com for more insights.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*

Financial Health & Operational Moats: The Illusion of High Earnings Quality

While the consumer battery sector displays ostensibly pristine cash flows—with EVE Energy (SZSE: 300014) and CosMX (SHSE: 688772) posting operating cash flow to net profit (OCF/NP) ratios of 1.81 and 4.42 respectively—a forensic audit of FY2025 filings reveals severe structural vulnerabilities. The industry is currently masking an acute liquidity "tight balance" under the guise of scale expansion.

CosMX is flashing red on liquidity metrics. With a debt-to-asset ratio expanding to 68.19% and a dangerously low quick ratio of 0.54, its short-term debt obligations ($309 million) eclipse available cash reserves. This aggressive leverage posture is fundamentally misaligned with its heavy reliance on the highly cyclical IT hardware market, rendering the company vulnerable if demand for AI PCs fails to offset margin compression.

Conversely, EVE Energy faces a pronounced inventory de-stocking risk. The company’s inventory book value surged 57% to $1.146 billion, doubling its 26% revenue growth rate. As cobalt prices experienced a vicious 171.66% upward reversion to roughly $55,400/MT by late 2025, delayed cost-pass-through mechanisms dictate that EVE will face formidable inventory impairment charges in FY2026 if downstream demand cools.

Meanwhile, retail-focused Anfu Tech (SHSE: 603031) sits on a demographic time bomb. Despite commanding a 50.71% gross margin via absolute channel dominance in China, its $404 million goodwill—comprising 40% of total assets—remains a toxic hangover from the Nanfu Battery acquisition. Stagnant revenue growth (2.94%) juxtaposed against looser credit terms (accounts receivable up 8.15%) indicates channel-stuffing fatigue, escalating the probability of an accretive acquisition turning into a massive writedown.

Supply Chain Pivot: Near-Shoring and the "Compliance Premium"

Geopolitical fragmentation has forced the industry out of its centralized manufacturing complacency. The narrative in FY2025 shifted definitively from "capacity out-migration" to "compliance-driven localization." The EU Battery Directive’s Digital Battery Passport and the US Inflation Reduction Act (IRA) have erected formidable non-tariff barriers, dictating a violent restructuring of global CAPEX.

LG Energy Solution (KRX: 373220) remains the apex predator of policy defense. Allocating a staggering $7.37 billion in CAPEX, primarily directed at US soil (Michigan, Ohio), LGES has successfully monopolized the compliance premium. By contrast, Chinese tier-one players are executing evasive near-shoring maneuvers. CosMX’s deployment of PACK assembly lines in Mexico serves as a strategic wedge into the North American IT supply chain, deliberately bypassing direct tariff hostilities while achieving a 43.42% self-supply rate in battery packs.

EVE Energy has abandoned standard export models altogether, pivoting to a capital-light "Cooperative Licensing & Service" (CLS) framework. By exporting production topology rather than physical cells—exemplified by the ACT joint venture in North America and its new Hungarian facility adjacent to BMW—EVE is effectively neutralizing the impact of China's impending 2027 export tax rebate cancellation. This vertical integration of service protocols rather than mere manufacturing output represents a critical evolutionary leap in circumventing US-Sino trade friction.

Figure 2025 Global Consumer Battery Competitive Matrix

HDIN Institutional Perspective: The AI Hardware Supercycle and Solid-State InflectionThe consumer battery sector is trapped in a transitional trough between legacy IT saturation and the Edge AI hardware supercycle. The integration of on-device LLMs (AI PCs and AI Phones) is not merely driving volume; it is forcing a thermodynamic reckoning. The deployment of Apple Intelligence and local AI architectures requires unprecedented pulse-discharge capabilities and extreme thermal management.

Here, CosMX has entrenched a formidable moat, achieving a commercialized silicon anode density of 900Wh/L. However, the ultimate endgame lies in solid-state commercialization. Both EVE Energy (with its Longquan No.2 10Ah solid-state rollout) and LGES have aggressively transitioned from R&D defense to disruptive disruption, pushing pilot lines into low-volume production.

We assess that players lacking direct exposure to either High-Silicon or Solid-State chemistry, such as Energizer (NYSE: ENR) with its anemic 1.1% R&D intensity, will face catastrophic market share erosion as consumer electronics manufacturers mandate next-generation thermal profiles. The divergence is clear: companies that successfully navigate the near-shoring CAPEX burden while simultaneously funding AI-compliant chemistry will capture the FY2026 upgrade cycle. Those relying purely on legacy distribution networks will be relegated to the low-margin, commoditized tail-end of the market.

Presentation download:

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research:

HDIN Research is a premier strategic advisory and equity intelligence firm bridging the gap between raw corporate disclosures and macroeconomic trends. We provide institutional investors with unvarnished, data-driven analysis on supply chain pivots, capital expenditures, and geopolitical regulatory impacts. Visit www.hdinresearch.com for more insights.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*