Dragonfly Energy Targets Vertical Integration as OEM Segment Surges 33.8% Amid Severe OCF Compression

Date : 2026-04-07

Reading : 93

Dragonfly Energy (NASDAQ: DFLI) executed a critical OEM revenue pivot in its FY2025 10-K, leveraging its 390,240 sq. ft. Reno, Nevada facility to offset consumer inventory de-stocking. However, a $8.9M structural cost realignment and aggressive debt restructuring are required to buy runway for its delayed 2027 dry-electrode commercialization amid acute cash burn.

Financial Health & Operational Moats: The Illusion of Margin Expansion

At first glance, Dragonfly Energy’s FY2025 financial optics present a paradox. Consolidated revenue recovered by 15.8% to $58.63 million, and gross margins expanded meaningfully from 23.0% to 26.7%. Yet, operating cash flow (OCF) deteriorated to -$25.97 million, and net losses widened drastically to $69.94 million.

This financial divergence requires dissection. The margin expansion is not a byproduct of pricing power in battery cells—unit sales volume remained virtually flat, growing a mere 1.6% (43,129 units). Instead, the margin accretion is driven by a strategic product-mix pivot toward high-margin system accessories (inverters, alternators) and an accretive brand licensing agreement with Stryten Energy, which recognized an initial $1 million of a projected $30 million, 7-year cash flow stream.

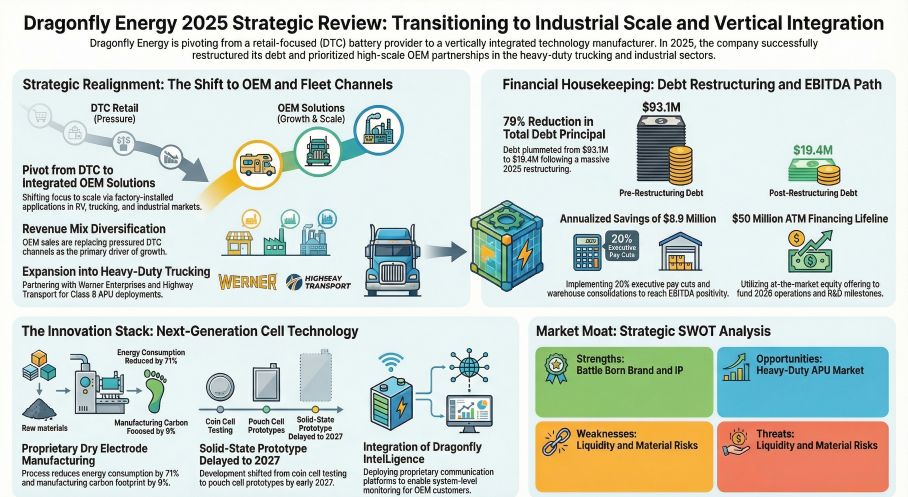

The optical collapse in net income is largely an accounting artifact, triggered by a $31.84 million non-cash debt extinguishment loss tied to the company's "Sixth Amendment" restructuring. By aggressively paying down $45 million in principal and converting $25 million into Series B Preferred Stock, DFLI successfully sanitized its balance sheet. However, the operational moat remains fragile. Bound by strict covenants capping annual CAPEX at $5 million, DFLI is currently reliant on a $50 million At-The-Market (ATM) facility to sustain operations, highlighting severe liquidity constraints.

Figure Dragonfly Energy 2025 Strategic Review: Transitioning to industrial Scale and Vertical Integration

Supply Chain Pivot: The Cost of Geopolitical Vulnerability

Supply Chain Pivot: The Cost of Geopolitical Vulnerability

Dragonfly’s transition from an aftermarket retail brand (DTC revenues dropped 8.5% YoY) to an industrial-grade OEM supplier (OEM revenues surged 33.8%, capturing 63.0% of the total mix) is anchored by exclusive integration deals with heavyweights like THOR Industries and Keystone RV.

Yet, beneath this revenue shift lies a critical supply chain bottleneck. DFLI currently operates as a pack assembler, entirely dependent on two Chinese LFP cell suppliers and a single Chinese BMS manufacturer. This feedstock concentration exposes the company to severe geopolitical risk and margin compression via tariff volatility, evidenced by a recent $1.58 million U.S. Customs shortfall.

To execute true vertical integration and capture the lucrative Advanced Manufacturing Production Credit under the IRA, DFLI is scaling its Reno, Nevada hub. The endgame is its proprietary Dry Electrode manufacturing process—a disruptive physics play that eliminates toxic NMP solvents, reduces energy consumption by 71%, and cuts manufacturing footprint by 22%. However, capital constraints have forced management to delay the deployment of large-scale spray drying equipment and solid-state pouch cell prototypes until early 2027, leaving the company structurally exposed to Asian supply chains for the next 24 months.

HDIN Institutional Perspective: A Wartime "Survival Mode"

From an institutional vantage point, Dragonfly Energy is a microcosm of the broader cyclical trough affecting mid-cap clean energy pure-plays. The company's strategic pivot toward heavy-duty applications (Class 8 APUs) and industrial off-grid storage signals a defensive maneuver against prolonged inventory de-stocking in consumer discretionary markets.

Governance indicators flash "wartime" survival mode. The consolidation of the CFO role under CEO Dr. Denis Phares, coupled with a March 2026 mandate swapping 20% of executive cash compensation for equity options (struck at $2.99, well above the current sub-$2.00 trading level), signals a management team aggressively preserving liquidity. The 1-for-10 reverse stock split and a $8.9 million annualized OPEX cut (including warehousing consolidation and headcount reductions) are necessary amputations to achieve target EBITDA breakeven by late FY2026.

DFLI’s dry electrode technology remains a potent non-standardized competitive weapon capable of fundamentally altering the $/kWh physics of LFP and solid-state batteries. But technology does not guarantee solvency. The company is trading equity for time. Investors must monitor the execution of the $50M ATM dilution against the Q2 2026 automated BMS line rollout—the precise inflection point where unit labor cost-pass-through mechanisms will dictate if DFLI survives to see its 2027 solid-state ambitions materialized.

Presentation download:

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research is a premier market intelligence firm dedicated to deconstructing complex corporate filings and macroeconomic shifts into actionable strategic insights. Discover more at www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*

Financial Health & Operational Moats: The Illusion of Margin Expansion

At first glance, Dragonfly Energy’s FY2025 financial optics present a paradox. Consolidated revenue recovered by 15.8% to $58.63 million, and gross margins expanded meaningfully from 23.0% to 26.7%. Yet, operating cash flow (OCF) deteriorated to -$25.97 million, and net losses widened drastically to $69.94 million.

This financial divergence requires dissection. The margin expansion is not a byproduct of pricing power in battery cells—unit sales volume remained virtually flat, growing a mere 1.6% (43,129 units). Instead, the margin accretion is driven by a strategic product-mix pivot toward high-margin system accessories (inverters, alternators) and an accretive brand licensing agreement with Stryten Energy, which recognized an initial $1 million of a projected $30 million, 7-year cash flow stream.

The optical collapse in net income is largely an accounting artifact, triggered by a $31.84 million non-cash debt extinguishment loss tied to the company's "Sixth Amendment" restructuring. By aggressively paying down $45 million in principal and converting $25 million into Series B Preferred Stock, DFLI successfully sanitized its balance sheet. However, the operational moat remains fragile. Bound by strict covenants capping annual CAPEX at $5 million, DFLI is currently reliant on a $50 million At-The-Market (ATM) facility to sustain operations, highlighting severe liquidity constraints.

Figure Dragonfly Energy 2025 Strategic Review: Transitioning to industrial Scale and Vertical Integration

Supply Chain Pivot: The Cost of Geopolitical VulnerabilityDragonfly’s transition from an aftermarket retail brand (DTC revenues dropped 8.5% YoY) to an industrial-grade OEM supplier (OEM revenues surged 33.8%, capturing 63.0% of the total mix) is anchored by exclusive integration deals with heavyweights like THOR Industries and Keystone RV.

Yet, beneath this revenue shift lies a critical supply chain bottleneck. DFLI currently operates as a pack assembler, entirely dependent on two Chinese LFP cell suppliers and a single Chinese BMS manufacturer. This feedstock concentration exposes the company to severe geopolitical risk and margin compression via tariff volatility, evidenced by a recent $1.58 million U.S. Customs shortfall.

To execute true vertical integration and capture the lucrative Advanced Manufacturing Production Credit under the IRA, DFLI is scaling its Reno, Nevada hub. The endgame is its proprietary Dry Electrode manufacturing process—a disruptive physics play that eliminates toxic NMP solvents, reduces energy consumption by 71%, and cuts manufacturing footprint by 22%. However, capital constraints have forced management to delay the deployment of large-scale spray drying equipment and solid-state pouch cell prototypes until early 2027, leaving the company structurally exposed to Asian supply chains for the next 24 months.

HDIN Institutional Perspective: A Wartime "Survival Mode"

From an institutional vantage point, Dragonfly Energy is a microcosm of the broader cyclical trough affecting mid-cap clean energy pure-plays. The company's strategic pivot toward heavy-duty applications (Class 8 APUs) and industrial off-grid storage signals a defensive maneuver against prolonged inventory de-stocking in consumer discretionary markets.

Governance indicators flash "wartime" survival mode. The consolidation of the CFO role under CEO Dr. Denis Phares, coupled with a March 2026 mandate swapping 20% of executive cash compensation for equity options (struck at $2.99, well above the current sub-$2.00 trading level), signals a management team aggressively preserving liquidity. The 1-for-10 reverse stock split and a $8.9 million annualized OPEX cut (including warehousing consolidation and headcount reductions) are necessary amputations to achieve target EBITDA breakeven by late FY2026.

DFLI’s dry electrode technology remains a potent non-standardized competitive weapon capable of fundamentally altering the $/kWh physics of LFP and solid-state batteries. But technology does not guarantee solvency. The company is trading equity for time. Investors must monitor the execution of the $50M ATM dilution against the Q2 2026 automated BMS line rollout—the precise inflection point where unit labor cost-pass-through mechanisms will dictate if DFLI survives to see its 2027 solid-state ambitions materialized.

Presentation download:

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research is a premier market intelligence firm dedicated to deconstructing complex corporate filings and macroeconomic shifts into actionable strategic insights. Discover more at www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*