Interactive Strength (NASDAQ: TRNR) Executes Aggressive Connected Fitness Consolidation as FY2025 Revenue Surges 114% Amid Going Concern Warnings

Date : 2026-04-07

Reading : 185

Interactive Strength Inc. (NASDAQ: TRNR) is pivoting from a hardware manufacturer to an M&A consolidator of distressed fitness assets following its FY2025 10-K audit. Operating across European and US B2B channels, the firm is utilizing target acquisitions to survive severe liquidity constraints and offset a $16.6M working capital deficit.

Financial Health & Operational Moats: The M&A Mirage

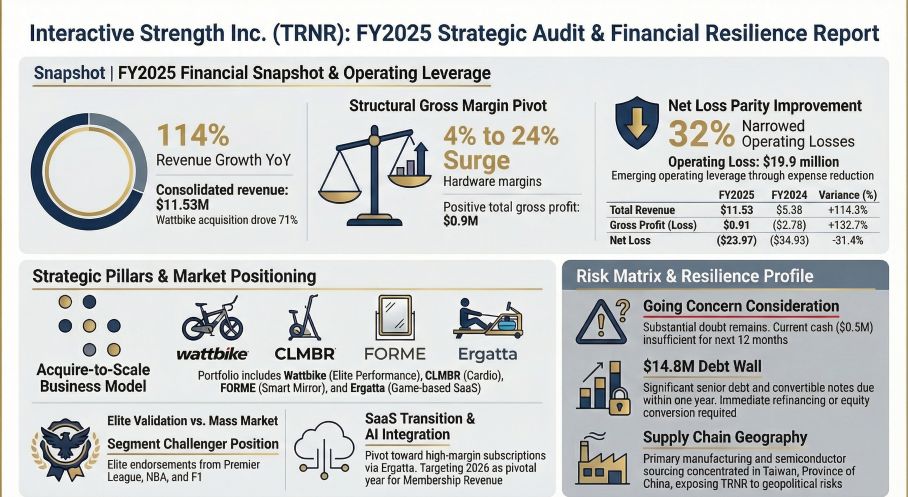

Interactive Strength is engineering a high-wire financial transition, masking organic decay with top-line injections from accretive acquisitions. FY2025 total revenue reached $11.53 million (+114% YoY), a figure almost entirely manufactured by the July 2025 integration of Wattbike, which accounted for a disproportionate 71% ($8.2 million) of the consolidated top line.

While this M&A maneuver successfully engineered a gross margin expansion from a catastrophic -51.6% to 8.0%, the underlying SaaS fundamentals remain deeply toxic. The subscription segment (Membership and Training) continues to hemorrhage capital, posting a -108% gross margin. This suggests that TRNR’s Customer Acquisition Cost (CAC) to Lifetime Value (LTV) ratio is fundamentally broken. Every new digital subscriber currently accelerates operating losses due to unscalable software hosting and content amortization costs.

Crucially, the corporate balance sheet operates under severe distress. A $6.4 million legal settlement from Sportstech in March 2026 and an aggressive $5.9 million debt-to-equity conversion blitz in early Q1 2026 are acting as the primary life-support mechanisms. To fund this M&A survival tactic, management executed a brutal 58% cut to R&D (down to $2.9 million). This capitulation in organic intellectual property development signals an abandonment of the "tech-first" narrative, repositioning TRNR as a pure-play asset harvester dependent on B2B channels like Woodway USA to move physical inventory.

Figure Interactive Strength Inc (TRNR): F2025 Strategic Audit & Financial Resilience Report

Supply Chain Pivot: The Geopolitical Choke Point

Supply Chain Pivot: The Geopolitical Choke Point

TRNR’s operational architecture operates on a high-beta, asset-light model that is dangerously exposed to regional concentration risk. The company’s manufacturing operations, critical components, and primary third-party foundries are almost exclusively tethered to Taiwan, China.

With FY2025 inventory levels sitting at $7.33 million—translating to an anemic inventory turnover rate of roughly 1.51x—the firm is highly vulnerable to systemic inventory de-stocking delays. TRNR lacks the purchasing scale to demand favorable cost-pass-through mechanisms from its semiconductor and hardware suppliers. Consequently, without the insulation of vertical integration, any geopolitical friction or macro-level supply chain bottleneck in the APAC region will trigger immediate margin compression, neutralizing the fragile 24% hardware gross margin newly established by the Wattbike portfolio.

HDIN Institutional Perspective: A Distressed Debt Vehicle in Disguise

Standard algorithmic analyses view TRNR’s March 2026 Ergatta acquisition and Wattbike integration as standard ecosystem expansions. Our editorial board takes a contrarian view: Interactive Strength is no longer a connected fitness company; it is effectively a distressed debt vehicle utilizing extreme financial engineering to maintain Nasdaq compliance.

Management’s strategic discipline is highly questionable, evidenced by the catastrophic capital misallocation involving digital assets. In a misguided attempt to secure alternative financing, TRNR engaged in highly speculative FET token collateralization, resulting in a staggering $27.7 million fair value impairment loss. This financial black hole, combined with toxic senior secured convertible notes bearing 12-15% interest rates and 10% Original Issue Discounts (OID), reveals a corporate entity completely locked out of traditional credit markets.

The relentless cadence of reverse stock splits—culminating in a 1:10 consolidation in February 2026—serves as a mechanical manipulation to delay delisting rather than a reflection of fundamental value. Unless the Ergatta integration immediately yields a positive SaaS margin inflection within the next two quarters, TRNR’s $14.8 million incoming "debt wall" will force a terminal restructuring.

Related Resources

* Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

* Analyst Briefing: Click this link to watch the YouTube video.

About HDIN Research

HDIN Research is a premier global market intelligence firm specializing in forensic financial analysis, supply chain auditing, and macroeconomic strategy. Visit us at www.hdinresearch.com to access our institutional-grade data terminals.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*

Financial Health & Operational Moats: The M&A Mirage

Interactive Strength is engineering a high-wire financial transition, masking organic decay with top-line injections from accretive acquisitions. FY2025 total revenue reached $11.53 million (+114% YoY), a figure almost entirely manufactured by the July 2025 integration of Wattbike, which accounted for a disproportionate 71% ($8.2 million) of the consolidated top line.

While this M&A maneuver successfully engineered a gross margin expansion from a catastrophic -51.6% to 8.0%, the underlying SaaS fundamentals remain deeply toxic. The subscription segment (Membership and Training) continues to hemorrhage capital, posting a -108% gross margin. This suggests that TRNR’s Customer Acquisition Cost (CAC) to Lifetime Value (LTV) ratio is fundamentally broken. Every new digital subscriber currently accelerates operating losses due to unscalable software hosting and content amortization costs.

Crucially, the corporate balance sheet operates under severe distress. A $6.4 million legal settlement from Sportstech in March 2026 and an aggressive $5.9 million debt-to-equity conversion blitz in early Q1 2026 are acting as the primary life-support mechanisms. To fund this M&A survival tactic, management executed a brutal 58% cut to R&D (down to $2.9 million). This capitulation in organic intellectual property development signals an abandonment of the "tech-first" narrative, repositioning TRNR as a pure-play asset harvester dependent on B2B channels like Woodway USA to move physical inventory.

Figure Interactive Strength Inc (TRNR): F2025 Strategic Audit & Financial Resilience Report

Supply Chain Pivot: The Geopolitical Choke PointTRNR’s operational architecture operates on a high-beta, asset-light model that is dangerously exposed to regional concentration risk. The company’s manufacturing operations, critical components, and primary third-party foundries are almost exclusively tethered to Taiwan, China.

With FY2025 inventory levels sitting at $7.33 million—translating to an anemic inventory turnover rate of roughly 1.51x—the firm is highly vulnerable to systemic inventory de-stocking delays. TRNR lacks the purchasing scale to demand favorable cost-pass-through mechanisms from its semiconductor and hardware suppliers. Consequently, without the insulation of vertical integration, any geopolitical friction or macro-level supply chain bottleneck in the APAC region will trigger immediate margin compression, neutralizing the fragile 24% hardware gross margin newly established by the Wattbike portfolio.

HDIN Institutional Perspective: A Distressed Debt Vehicle in Disguise

Standard algorithmic analyses view TRNR’s March 2026 Ergatta acquisition and Wattbike integration as standard ecosystem expansions. Our editorial board takes a contrarian view: Interactive Strength is no longer a connected fitness company; it is effectively a distressed debt vehicle utilizing extreme financial engineering to maintain Nasdaq compliance.

Management’s strategic discipline is highly questionable, evidenced by the catastrophic capital misallocation involving digital assets. In a misguided attempt to secure alternative financing, TRNR engaged in highly speculative FET token collateralization, resulting in a staggering $27.7 million fair value impairment loss. This financial black hole, combined with toxic senior secured convertible notes bearing 12-15% interest rates and 10% Original Issue Discounts (OID), reveals a corporate entity completely locked out of traditional credit markets.

The relentless cadence of reverse stock splits—culminating in a 1:10 consolidation in February 2026—serves as a mechanical manipulation to delay delisting rather than a reflection of fundamental value. Unless the Ergatta integration immediately yields a positive SaaS margin inflection within the next two quarters, TRNR’s $14.8 million incoming "debt wall" will force a terminal restructuring.

Related Resources

* Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

* Analyst Briefing: Click this link to watch the YouTube video.

About HDIN Research

HDIN Research is a premier global market intelligence firm specializing in forensic financial analysis, supply chain auditing, and macroeconomic strategy. Visit us at www.hdinresearch.com to access our institutional-grade data terminals.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*