Global Stationery Giants See Diverging Margins: M&G and Acme United Capitalize on B2B Pivots Amid ACCO Brands' 8.5% Revenue Contraction

Date : 2026-04-03

Reading : 171

In FY2025, global stationery majors—including M&G, PILOT, and ACCO Brands—executed aggressive supply chain realignments. Amid US tariff pressures and digitization, M&G’s $2.09B B2B pivot and Acme United's medical expansion drove profit divergence, signaling a definitive sector shift away from paper-based legacy assets.

Financial Health & Operational Moats: The End of Pure-Play Office Supply

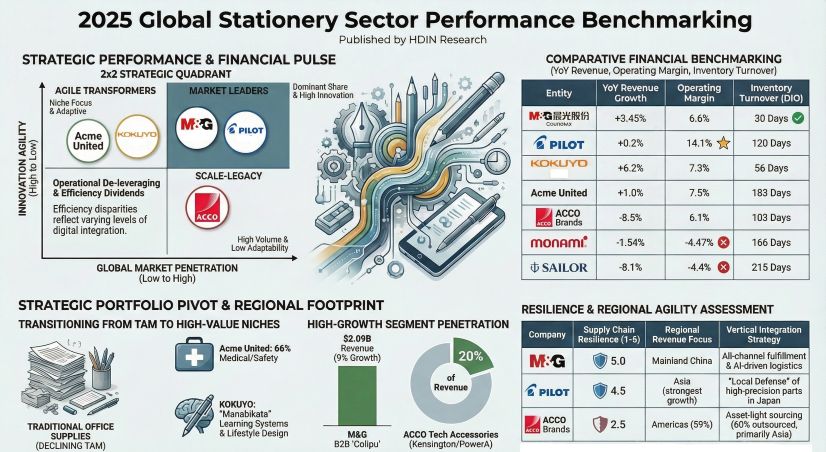

The FY2025 audit cycle reveals a brutal bifurcation in the global stationery sector: companies clinging to traditional paper-based portfolios are suffering severe margin compression, while those executing accretive acquisitions into B2B and specialized niches are generating outsized free cash flow.

Shanghai M&G Stationery Inc. (SHSE: 603899) posted a commanding 14.56% ROE against $3.48 billion in total revenue. More critical than top-line growth is M&G’s negative Cash Conversion Cycle (CCC) of -10 days, driven by a Days Payable Outstanding (DPO) of 107 days. This is not a mere accounting quirk; it signals absolute pricing power over downstream suppliers and highly agile inventory management (DIO of 30 days). M&G’s $2.09 billion Colipu B2B platform now acts as the primary volume engine, insulating the firm from domestic consumer headwinds.

Conversely, ACCO Brands (NYSE: ACCO) exemplifies the structural decay of traditional paper assets. Burdened by a 70.5% debt ratio and an anemic interest coverage ratio of 2.54x, ACCO’s 8.5% revenue contraction to $1.52 billion exposes severe financial fragility. The company's $165 million non-cash impairment charge across its North American reporting units underscores the systemic devaluation of legacy commercial office supplies.

Acme United (NYSE: ACU) provides the textbook blueprint for escaping the sector's low-margin gravity. By reducing reliance on Westcott cutting tools and pushing First Aid & Safety segments to 66% of total revenue via accretive acquisitions (e.g., Elite First Aid, My Medic), ACU expanded its gross margin to an industry-leading 39.4%. The company effectively transformed itself from a discretionary school supplier into an OSHA-compliant healthcare logistics provider.

Figure 2025 Clobal Stationery Sector Performance Benchmarking

Supply Chain Pivot: Tariff Mitigation and the "China+1" Reality

Supply Chain Pivot: Tariff Mitigation and the "China+1" Reality

Macroeconomic volatility and sustained US tariff pressures have forced a rapid unwinding of centralized global procurement. The FY2025 data highlights a race toward regional vertical integration and strategic near-shoring to protect cost-pass-through mechanisms.

Southeast Asian Consolidation: KOKUYO Co., Ltd. (TYO: 7953) bypassed the economic stagnation of the Chinese commercial real estate and furniture markets by moving to acquire Vietnam's Thien Long Group (TLG). This M&A maneuver instantly secures a localized manufacturing footprint and downstream distribution network within the high-growth ASEAN block.

North American Onshoring & Divestitures: To stem bleeding from logistics costs and tariff exposure, ACCO Brands liquidated its Sidney, New York, and Barcelona manufacturing facilities, prioritizing footprint rationalization. In contrast, Acme United deployed targeted regional CAPEX, acquiring a 77,000-square-foot facility in Mt. Pleasant, Tennessee, for $6 million to onshore the production of Spill Magic and stabilize its tier-one medical supply chain.

Domestic Automated Fortification: PILOT Corporation (TYO: 7846) opted for intense domestic capitalization. The firm deployed $184 million (27.5 billion JPY) in CAPEX toward its Hiratsuka and Isesaki plants in Japan. By fully automating ballpoint pen production while simultaneously consolidating its PPIN subsidiary in India, PILOT maintains strict IP control over its high-margin FriXion ink formulas while localizing final assembly in emerging markets.

HDIN Institutional Perspective: The Structural Trough of the "Writing Instrument"

The 2025 financial disclosures confirm that the traditional stationery market has peaked. Growth now strictly requires cannibalizing adjacent sectors or possessing absolute supply chain dominance.

PILOT’s quiet pivot into micro-porous ceramics for semiconductor equipment—leveraging its precision ballpoint machining technology—represents the highest form of cross-industry vertical integration. This materials-science moat secures premium margins far beyond the reach of consumer retail.

Meanwhile, mid-tier manufacturers lacking pricing power are facing existential crises. The Sailor Pen Co., Ltd. (TYO: 7992) serves as the canary in the coal mine. Operating with a 75.7% debt ratio and an abysmal -21.0% ROE, Sailor's core moat—the 21K gold nib—has become a fatal liability amid surging gold feedstock volatility. The inability to enact cost-pass-through mechanisms against a backdrop of shrinking domestic demand has triggered an auditor's "going concern" warning.

Investors must ruthlessly filter out equities heavily weighted in paper-based business essentials, as these are highly vulnerable to prolonged inventory de-stocking cycles. Capital allocation should pivot toward firms demonstrating multi-channel B2B fulfillment architectures and strategic exposure to non-cyclical compliance categories.

Access the Full Intelligence Suite

* Click the PDF download link under 'Related Topics' to access the presentation of this report.

* Click this link to watch the YouTube video.

About HDIN Research

HDIN Research is a premier market intelligence and strategic advisory firm delivering institutional-grade analysis on global supply chain configurations, cyclical sector rotations, and macroeconomic policy impacts. (www.hdinresearch.com)

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.

Financial Health & Operational Moats: The End of Pure-Play Office Supply

The FY2025 audit cycle reveals a brutal bifurcation in the global stationery sector: companies clinging to traditional paper-based portfolios are suffering severe margin compression, while those executing accretive acquisitions into B2B and specialized niches are generating outsized free cash flow.

Shanghai M&G Stationery Inc. (SHSE: 603899) posted a commanding 14.56% ROE against $3.48 billion in total revenue. More critical than top-line growth is M&G’s negative Cash Conversion Cycle (CCC) of -10 days, driven by a Days Payable Outstanding (DPO) of 107 days. This is not a mere accounting quirk; it signals absolute pricing power over downstream suppliers and highly agile inventory management (DIO of 30 days). M&G’s $2.09 billion Colipu B2B platform now acts as the primary volume engine, insulating the firm from domestic consumer headwinds.

Conversely, ACCO Brands (NYSE: ACCO) exemplifies the structural decay of traditional paper assets. Burdened by a 70.5% debt ratio and an anemic interest coverage ratio of 2.54x, ACCO’s 8.5% revenue contraction to $1.52 billion exposes severe financial fragility. The company's $165 million non-cash impairment charge across its North American reporting units underscores the systemic devaluation of legacy commercial office supplies.

Acme United (NYSE: ACU) provides the textbook blueprint for escaping the sector's low-margin gravity. By reducing reliance on Westcott cutting tools and pushing First Aid & Safety segments to 66% of total revenue via accretive acquisitions (e.g., Elite First Aid, My Medic), ACU expanded its gross margin to an industry-leading 39.4%. The company effectively transformed itself from a discretionary school supplier into an OSHA-compliant healthcare logistics provider.

Figure 2025 Clobal Stationery Sector Performance Benchmarking

Supply Chain Pivot: Tariff Mitigation and the "China+1" RealityMacroeconomic volatility and sustained US tariff pressures have forced a rapid unwinding of centralized global procurement. The FY2025 data highlights a race toward regional vertical integration and strategic near-shoring to protect cost-pass-through mechanisms.

Southeast Asian Consolidation: KOKUYO Co., Ltd. (TYO: 7953) bypassed the economic stagnation of the Chinese commercial real estate and furniture markets by moving to acquire Vietnam's Thien Long Group (TLG). This M&A maneuver instantly secures a localized manufacturing footprint and downstream distribution network within the high-growth ASEAN block.

North American Onshoring & Divestitures: To stem bleeding from logistics costs and tariff exposure, ACCO Brands liquidated its Sidney, New York, and Barcelona manufacturing facilities, prioritizing footprint rationalization. In contrast, Acme United deployed targeted regional CAPEX, acquiring a 77,000-square-foot facility in Mt. Pleasant, Tennessee, for $6 million to onshore the production of Spill Magic and stabilize its tier-one medical supply chain.

Domestic Automated Fortification: PILOT Corporation (TYO: 7846) opted for intense domestic capitalization. The firm deployed $184 million (27.5 billion JPY) in CAPEX toward its Hiratsuka and Isesaki plants in Japan. By fully automating ballpoint pen production while simultaneously consolidating its PPIN subsidiary in India, PILOT maintains strict IP control over its high-margin FriXion ink formulas while localizing final assembly in emerging markets.

HDIN Institutional Perspective: The Structural Trough of the "Writing Instrument"

The 2025 financial disclosures confirm that the traditional stationery market has peaked. Growth now strictly requires cannibalizing adjacent sectors or possessing absolute supply chain dominance.

PILOT’s quiet pivot into micro-porous ceramics for semiconductor equipment—leveraging its precision ballpoint machining technology—represents the highest form of cross-industry vertical integration. This materials-science moat secures premium margins far beyond the reach of consumer retail.

Meanwhile, mid-tier manufacturers lacking pricing power are facing existential crises. The Sailor Pen Co., Ltd. (TYO: 7992) serves as the canary in the coal mine. Operating with a 75.7% debt ratio and an abysmal -21.0% ROE, Sailor's core moat—the 21K gold nib—has become a fatal liability amid surging gold feedstock volatility. The inability to enact cost-pass-through mechanisms against a backdrop of shrinking domestic demand has triggered an auditor's "going concern" warning.

Investors must ruthlessly filter out equities heavily weighted in paper-based business essentials, as these are highly vulnerable to prolonged inventory de-stocking cycles. Capital allocation should pivot toward firms demonstrating multi-channel B2B fulfillment architectures and strategic exposure to non-cyclical compliance categories.

Access the Full Intelligence Suite

* Click the PDF download link under 'Related Topics' to access the presentation of this report.

* Click this link to watch the YouTube video.

About HDIN Research

HDIN Research is a premier market intelligence and strategic advisory firm delivering institutional-grade analysis on global supply chain configurations, cyclical sector rotations, and macroeconomic policy impacts. (www.hdinresearch.com)

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.