Xanadu Targets Photonic Quantum Commercialization as Post-SPAC Liquidity Surges to $282M in FY2026 Audit

Date : 2026-04-07

Reading : 94

Toronto-based Xanadu (NASDAQ: XNDU) secured $282.8M in post-SPAC capital and a $28.6M Canadian SIF grant in Q1 2026, cross-listing on Nasdaq to fund its high-burn photonic hardware roadmap. This aggressive liquidity play effectively extends its pre-commercial cash runway to 2030, bypassing legacy superconducting constraints.

Financial Health & Operational Moats: The Cost of Quantum Supremacy

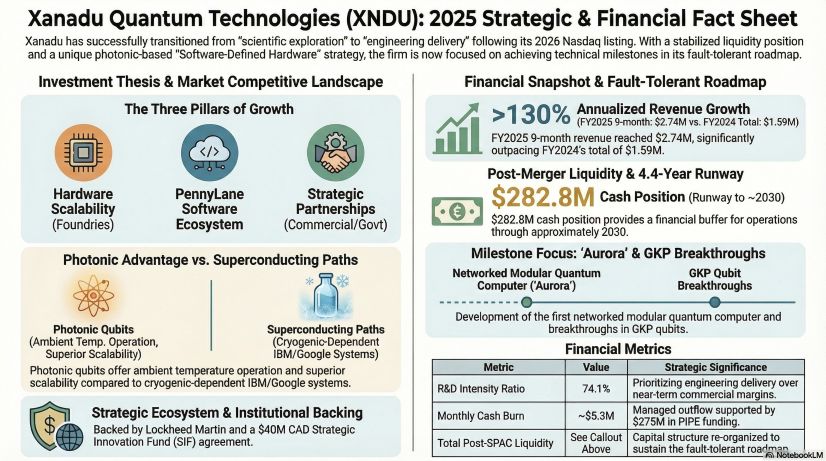

Based on Xanadu’s recent 20-F shell company disclosures following its merger with Crane Harbor Acquisition Corp., the firm is navigating a hyper-dilutive but necessary capital phase. For the first nine months of FY2025, revenue hit $2.74M—an annualized growth trajectory exceeding 130%, yet immaterial when weighed against an aggressive $38.32M in R&D expenditure (representing 74.1% of total OPEX).

Unlike legacy semiconductor foundries currently battling cyclical margin compression and aggressive inventory de-stocking down the supply chain, Xanadu operates in a pre-commercial deep-tech vacuum. The company lacks near-term cost-pass-through mechanisms to offset its $5.38M monthly cash burn. However, the $275M PIPE financing—anchored by OMERS (15.4% voting power) and Bessemer Venture Partners (8.8%)—provides a definitive 4.4-year runway.

The "So What" for institutional investors: Xanadu is utilizing a dual-class share structure (CEO Christian Weedbrook holding 17.9% voting power via Class A shares) to insulate its engineering roadmap from short-term market volatility. Furthermore, analysts must heavily discount the GAAP net income noise caused by the 1.1M Earn-out Shares classified as liabilities; their fair-value mark-to-market fluctuations will distort true operating cash flow metrics as the stock tests the $12.50 and $15.00 trigger thresholds.

Figure Xanadu Quantum Technologies (XNDU) 2025: Strategic & Financial Fact Sheet

Supply Chain Pivot: The Foundry-Compatible Moat

Supply Chain Pivot: The Foundry-Compatible Moat

The core narrative driving Xanadu’s valuation is a structural divergence from the cryogenic-dependent superconducting architectures championed by IBM and Google. By leveraging a photonic quantum pathway, Xanadu aims to achieve fault tolerance at room temperature.

More critically, this architecture relies on existing CMOS semiconductor facilities rather than bespoke fabrication. Operating out of its 777 Bay Street, Toronto laboratories, Xanadu is highly concentrated geographically. Over the next 24 months, we anticipate management will need to execute accretive acquisitions to drive the vertical integration of specialized electro-optic components, securing its hardware supply chain against geopolitical fragmentation.

The presence of the Lockheed Martin Master Retirement Trust on the capitalization table is not merely a financial endorsement; it is a hard proxy for the aerospace and defense sector's urgent mandate to simulate fluid dynamics and hedge against "Q-Day" cryptographic threats using scalable, foundry-ready photonic hardware.

HDIN Institutional Perspective: Sovereign Debt as a 2028 Catalyst

KPMG’s "going concern" emphasis on Old Xanadu’s historical financials has been temporarily neutralized by the SPAC liquidity event, but a structural ticking clock remains. Xanadu's relationship with the Canadian Ministry of Innovation via the CAD 40M ($28.63M) Strategic Innovation Fund (SIF) is a double-edged sword. While it provides non-dilutive R&D capital, the 20-year repayment schedule strictly triggers in April 2028.

We view 2028 as the definitive inflection point for the global quantum sector. By this deadline, Xanadu must transition its PennyLane software ecosystem—currently a loss-leading developer acquisition tool—into a high-margin enterprise SaaS revenue engine. If the quantum hardware delivery cycle is delayed, the lack of recurring revenue will force a secondary market capital raise under significantly tighter macroeconomic conditions. Xanadu’s survival dictates that it must secure quantum supremacy benchmarks prior to this debt-servicing cliff, transitioning from sovereign-subsidized research to sovereign-critical infrastructure.

Presentation Download & Video Access

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research (www.hdinresearch.com) is a premier provider of institutional-grade market intelligence, specializing in deep-tech, semiconductor, and quantum computing financial analysis. Our proprietary methodologies bridge the gap between complex engineering roadmaps and capital market valuations.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*

Financial Health & Operational Moats: The Cost of Quantum Supremacy

Based on Xanadu’s recent 20-F shell company disclosures following its merger with Crane Harbor Acquisition Corp., the firm is navigating a hyper-dilutive but necessary capital phase. For the first nine months of FY2025, revenue hit $2.74M—an annualized growth trajectory exceeding 130%, yet immaterial when weighed against an aggressive $38.32M in R&D expenditure (representing 74.1% of total OPEX).

Unlike legacy semiconductor foundries currently battling cyclical margin compression and aggressive inventory de-stocking down the supply chain, Xanadu operates in a pre-commercial deep-tech vacuum. The company lacks near-term cost-pass-through mechanisms to offset its $5.38M monthly cash burn. However, the $275M PIPE financing—anchored by OMERS (15.4% voting power) and Bessemer Venture Partners (8.8%)—provides a definitive 4.4-year runway.

The "So What" for institutional investors: Xanadu is utilizing a dual-class share structure (CEO Christian Weedbrook holding 17.9% voting power via Class A shares) to insulate its engineering roadmap from short-term market volatility. Furthermore, analysts must heavily discount the GAAP net income noise caused by the 1.1M Earn-out Shares classified as liabilities; their fair-value mark-to-market fluctuations will distort true operating cash flow metrics as the stock tests the $12.50 and $15.00 trigger thresholds.

Figure Xanadu Quantum Technologies (XNDU) 2025: Strategic & Financial Fact Sheet

Supply Chain Pivot: The Foundry-Compatible MoatThe core narrative driving Xanadu’s valuation is a structural divergence from the cryogenic-dependent superconducting architectures championed by IBM and Google. By leveraging a photonic quantum pathway, Xanadu aims to achieve fault tolerance at room temperature.

More critically, this architecture relies on existing CMOS semiconductor facilities rather than bespoke fabrication. Operating out of its 777 Bay Street, Toronto laboratories, Xanadu is highly concentrated geographically. Over the next 24 months, we anticipate management will need to execute accretive acquisitions to drive the vertical integration of specialized electro-optic components, securing its hardware supply chain against geopolitical fragmentation.

The presence of the Lockheed Martin Master Retirement Trust on the capitalization table is not merely a financial endorsement; it is a hard proxy for the aerospace and defense sector's urgent mandate to simulate fluid dynamics and hedge against "Q-Day" cryptographic threats using scalable, foundry-ready photonic hardware.

HDIN Institutional Perspective: Sovereign Debt as a 2028 Catalyst

KPMG’s "going concern" emphasis on Old Xanadu’s historical financials has been temporarily neutralized by the SPAC liquidity event, but a structural ticking clock remains. Xanadu's relationship with the Canadian Ministry of Innovation via the CAD 40M ($28.63M) Strategic Innovation Fund (SIF) is a double-edged sword. While it provides non-dilutive R&D capital, the 20-year repayment schedule strictly triggers in April 2028.

We view 2028 as the definitive inflection point for the global quantum sector. By this deadline, Xanadu must transition its PennyLane software ecosystem—currently a loss-leading developer acquisition tool—into a high-margin enterprise SaaS revenue engine. If the quantum hardware delivery cycle is delayed, the lack of recurring revenue will force a secondary market capital raise under significantly tighter macroeconomic conditions. Xanadu’s survival dictates that it must secure quantum supremacy benchmarks prior to this debt-servicing cliff, transitioning from sovereign-subsidized research to sovereign-critical infrastructure.

Presentation Download & Video Access

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research (www.hdinresearch.com) is a premier provider of institutional-grade market intelligence, specializing in deep-tech, semiconductor, and quantum computing financial analysis. Our proprietary methodologies bridge the gap between complex engineering roadmaps and capital market valuations.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*