Global Biosimilar Giants See Diverging Margins: Celltrion and Alvotech Average 18% Revenue Growth Amid High-Yield Debt and SC Pipeline Pivots

Date : 2026-04-06

Reading : 265

In FY2025, global biosimilar leaders Celltrion, Samsung Bioepis, and Alvotech disclosed severe margin divergence across US and European markets. Driven by IRA pricing pressures, firms are deploying CapEx into subcutaneous (SC) formulations and US-based CDMO acquisitions to secure 2026 commercial moats and hedge against escalating feedstock volatility.

Financial Health & Operational Moats: The Cost of Commercialization

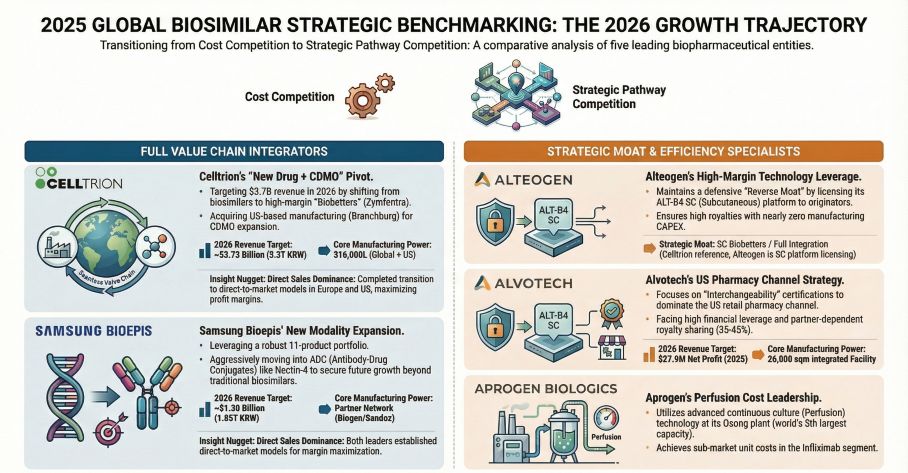

An audit of 2025 corporate filings reveals a stark bifurcation in the biosimilar sector: the terminal profitability of vertical integration versus the fragile leverage of partner-dependent commercialization.

Alvotech (NASDAQ: ALVO) posted a sector-leading 19.7% top-line growth, reaching $586 million and its first net profit of $27.92 million. However, a deeper forensic view exposes severe earnings quality risks. The company’s operational cash flow (OCF) remains negative, heavily distorted by milestone accounting—with 52.9% of revenues stemming from non-cash license payments. Straddled with a $1.29 billion debt load (heavily indexed to SOFR + 6.0% and 12.5% fixed tranches), Alvotech’s adjusted EBITDA of $137.2 million barely provides a 1.0x to 1.1x interest coverage ratio. If European terminal sales fail to accelerate into 2026, the company faces an imminent liquidity squeeze by its 2027 maturity wall.

Conversely, Celltrion (KRX: 068270) has successfully absorbed its healthcare distribution arm, booking $2.92 billion in revenue (+17% YoY). The firm's balance sheet boasts $787 million in cash and equivalents. By shifting from a partner-reliant model to direct US sales for high-margin assets like the Zymfentra (SC Infliximab) biobetter, Celltrion is maximizing unit economics and bypassing the margin compression typical of wholesale distribution layers.

Alteogen (KOSDAQ: 191170) presents a radical departure from traditional asset-heavy manufacturing. Operating as a pure-play technology exporter with a staggering 28.15% R&D intensity, Alteogen booked $117.4 million (78.5% of total revenue) purely from ALT-B4 platform licensing fees. Yet, an anomalous 582% year-over-year surge in work-in-process inventory (to 6.53 billion KRW) signals a precarious transitional phase as the company scales physical commercial outputs alongside its intellectual property.

Figure 2025 GLOBAL BIOSIMILAR STRATEGIC BENCHMARKING

Supply Chain Pivot: Geopolitical CapEx and Yield Optimization

Supply Chain Pivot: Geopolitical CapEx and Yield Optimization

Capital expenditure is rapidly realigning to front-run geopolitical friction and biological manufacturing bottlenecks. Celltrion executed a highly strategic $30.22 million acquisition of a 66,000-liter drug substance facility in Branchburg, New Jersey. This physical US footprint is a direct hedge against the impending *Biosecure Act*, positioning Celltrion not only to secure domestic supply lines but also to unlock accretive US-based CDMO revenues by 2026.

Simultaneously, Aprogen (KOSPI: 003060) is attempting to engineer a cost-pass-through advantage via continuous manufacturing. Its Osong facility, rated as the world’s fifth-largest antibody plant, utilizes proprietary perfusion technology to push annual throughput past 3,000 kg. While currently operating at a net loss with $52 million in revenue, Aprogen’s aggressive yield optimization strategy aims to survive the deflationary pricing wars in commoditized molecules like Trastuzumab and Adalimumab.

HDIN Institutional Perspective: 2026 Strategic Divergence

The structural shift outlined in the 2025 10-K and 20-F equivalents confirms the era of pure-play generic biosimilars is effectively dead. Market viability now requires structural moats against Pharmacy Benefit Manager (PBM) rebate traps and Medicare negotiations under the IRA.

1. The "Interchangeability" Moat: Samsung Bioepis and Alvotech are leveraging FDA interchangeability status to aggressively penetrate the retail pharmacy channel. This legislative mechanism forces automatic substitution at the pharmacy counter, functionally overriding physician-level brand loyalty for blockbuster targets like Stelara and Humira.

2. Escaping the Thicket via Novel Modalities: Samsung Bioepis is preemptively rotating CapEx toward next-generation Antibody-Drug Conjugates (ADCs), specifically advancing Nectin-4 and EGFR-HER3 pipelines. This indicates peak margin extraction in legacy biosimilars is approaching a cyclical trough, forcing top-tier players to hunt for novel therapeutic premiums.

3. The 2026 Inflection Point: Celltrion has issued the Street's most aggressive FY2026 guidance, targeting $3.72 billion (5.3 trillion KRW) fueled by an arsenal of five new drug launches. We assess Celltrion's vertically integrated, direct-sales machinery offers the highest probability of execution. In contrast, while Alvotech's pipeline is robust, its over-reliance on external commercial partners (e.g., Teva) limits its pricing agility in a rapidly commoditizing US market.

Presentation Download & Video Access

Click the PDF download link under "Related Topics" to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research is a premier market intelligence and strategic advisory firm specializing in institutional-grade analysis of global equities, deep-tech supply chains, and macroeconomic cycles. Discover more analytical edge at www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*

Financial Health & Operational Moats: The Cost of Commercialization

An audit of 2025 corporate filings reveals a stark bifurcation in the biosimilar sector: the terminal profitability of vertical integration versus the fragile leverage of partner-dependent commercialization.

Alvotech (NASDAQ: ALVO) posted a sector-leading 19.7% top-line growth, reaching $586 million and its first net profit of $27.92 million. However, a deeper forensic view exposes severe earnings quality risks. The company’s operational cash flow (OCF) remains negative, heavily distorted by milestone accounting—with 52.9% of revenues stemming from non-cash license payments. Straddled with a $1.29 billion debt load (heavily indexed to SOFR + 6.0% and 12.5% fixed tranches), Alvotech’s adjusted EBITDA of $137.2 million barely provides a 1.0x to 1.1x interest coverage ratio. If European terminal sales fail to accelerate into 2026, the company faces an imminent liquidity squeeze by its 2027 maturity wall.

Conversely, Celltrion (KRX: 068270) has successfully absorbed its healthcare distribution arm, booking $2.92 billion in revenue (+17% YoY). The firm's balance sheet boasts $787 million in cash and equivalents. By shifting from a partner-reliant model to direct US sales for high-margin assets like the Zymfentra (SC Infliximab) biobetter, Celltrion is maximizing unit economics and bypassing the margin compression typical of wholesale distribution layers.

Alteogen (KOSDAQ: 191170) presents a radical departure from traditional asset-heavy manufacturing. Operating as a pure-play technology exporter with a staggering 28.15% R&D intensity, Alteogen booked $117.4 million (78.5% of total revenue) purely from ALT-B4 platform licensing fees. Yet, an anomalous 582% year-over-year surge in work-in-process inventory (to 6.53 billion KRW) signals a precarious transitional phase as the company scales physical commercial outputs alongside its intellectual property.

Figure 2025 GLOBAL BIOSIMILAR STRATEGIC BENCHMARKING

Supply Chain Pivot: Geopolitical CapEx and Yield OptimizationCapital expenditure is rapidly realigning to front-run geopolitical friction and biological manufacturing bottlenecks. Celltrion executed a highly strategic $30.22 million acquisition of a 66,000-liter drug substance facility in Branchburg, New Jersey. This physical US footprint is a direct hedge against the impending *Biosecure Act*, positioning Celltrion not only to secure domestic supply lines but also to unlock accretive US-based CDMO revenues by 2026.

Simultaneously, Aprogen (KOSPI: 003060) is attempting to engineer a cost-pass-through advantage via continuous manufacturing. Its Osong facility, rated as the world’s fifth-largest antibody plant, utilizes proprietary perfusion technology to push annual throughput past 3,000 kg. While currently operating at a net loss with $52 million in revenue, Aprogen’s aggressive yield optimization strategy aims to survive the deflationary pricing wars in commoditized molecules like Trastuzumab and Adalimumab.

HDIN Institutional Perspective: 2026 Strategic Divergence

The structural shift outlined in the 2025 10-K and 20-F equivalents confirms the era of pure-play generic biosimilars is effectively dead. Market viability now requires structural moats against Pharmacy Benefit Manager (PBM) rebate traps and Medicare negotiations under the IRA.

1. The "Interchangeability" Moat: Samsung Bioepis and Alvotech are leveraging FDA interchangeability status to aggressively penetrate the retail pharmacy channel. This legislative mechanism forces automatic substitution at the pharmacy counter, functionally overriding physician-level brand loyalty for blockbuster targets like Stelara and Humira.

2. Escaping the Thicket via Novel Modalities: Samsung Bioepis is preemptively rotating CapEx toward next-generation Antibody-Drug Conjugates (ADCs), specifically advancing Nectin-4 and EGFR-HER3 pipelines. This indicates peak margin extraction in legacy biosimilars is approaching a cyclical trough, forcing top-tier players to hunt for novel therapeutic premiums.

3. The 2026 Inflection Point: Celltrion has issued the Street's most aggressive FY2026 guidance, targeting $3.72 billion (5.3 trillion KRW) fueled by an arsenal of five new drug launches. We assess Celltrion's vertically integrated, direct-sales machinery offers the highest probability of execution. In contrast, while Alvotech's pipeline is robust, its over-reliance on external commercial partners (e.g., Teva) limits its pricing agility in a rapidly commoditizing US market.

Presentation Download & Video Access

Click the PDF download link under "Related Topics" to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research is a premier market intelligence and strategic advisory firm specializing in institutional-grade analysis of global equities, deep-tech supply chains, and macroeconomic cycles. Discover more analytical edge at www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*