XREAL Pivots to AI Spatial Computing as Google Partnership Drives 30.8% FY2025 Revenue Growth and Structural Margin Expansion

Date : 2026-04-06

Reading : 684

XREAL accelerates its IPO trajectory in FY2025, pivoting from hardware OEM to an AI spatial computing platform. Driven by vertical integration at its Wuxi optical plant and an accretive Google partnership, the global AR leader posted $71.79 million in revenue, expanding gross margins to 35.2% ahead of a critical 2026 product cycle.

Financial Health & Operational Moats: Vertical Integration Drives Structural Margin Expansion

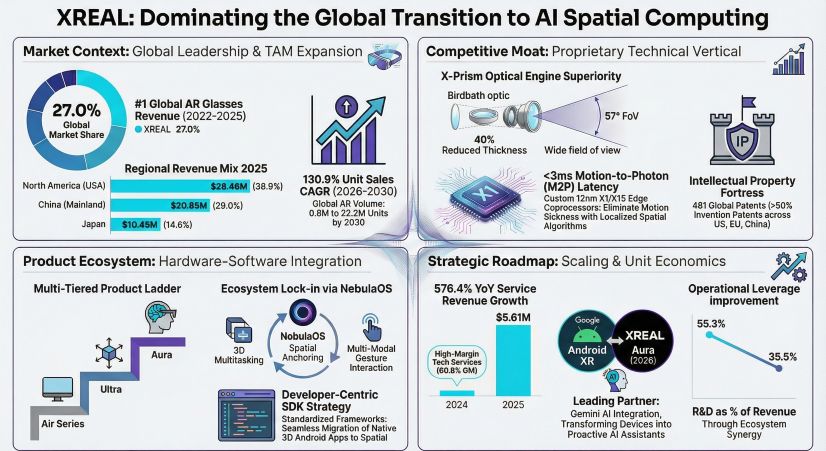

A forensic audit of XREAL’s FY2025 prospectus reveals a fundamental shift in its unit economics. Revenue grew 30.8% year-over-year to $71.79 million, but the true institutional signal lies in the structural gross margin expansion—surging from 18.8% in 2023 to 35.2% in 2025. This margin trajectory is not a byproduct of aggressive pricing, but a direct result of relentless vertical integration and BOM (Bill of Materials) optimization.

The phase-out of the low-margin Air series (ASP $230) in favor of the flagship One series (ASP $445) facilitated severe margin uplift. By deploying its proprietary 12nm X1 edge co-processor and X-Prism optical engine, XREAL mitigated the cost-pass-through mechanisms typically dictated by third-party silicon vendors.

Furthermore, R&D operating leverage is materializing. While absolute R&D spend remains robust at $25.45 million, its ratio to revenue compressed from 55.3% in 2023 to 35.5% in 2025. Beyond hardware, XREAL is monetizing its technical moat through enterprise B2B channels. Custom development services for heavy-hitters like Google (Project Aura) and NIO (NIO Air) generated $5.61 million in FY2025—a 576.4% YoY surge—commanding an outsized 60.8% gross margin.

However, liquidity requires scrutiny. The balance sheet reflects a daunting $421.0 million net liability, though this is primarily an accounting anomaly tied to convertible redeemable preferred stock, which will automatically convert to equity post-IPO. The more pressing metric is the -$28.31 million in operating cash flow. XREAL must leverage its IPO proceeds to bridge the cash burn until its subscription-based software ecosystem matures.

Figure XREAL: Dominating the Global Transition to Al Spatial Computing

Supply Chain Pivot: Wuxi CAPEX Realignment and Geopolitical De-Risking

XREAL is executing a textbook "dumbbell" manufacturing strategy to balance IP protection with capital efficiency. The company retains high-margin, ultra-precision manufacturing in-house while outsourcing commoditized assembly.

The epicenter of this supply chain pivot is the proprietary Wuxi optical facility. Currently operating at 70.1% utilization with a design capacity of 21.6K units, the slight dip in efficiency is a deliberate CAPEX realignment. XREAL is installing localized 100-class cleanrooms to absorb the anticipated 2026 volume shock from Project Aura. Long-term CAPEX guidance points to a staggering 810K unit capacity by 2031. Low-margin final assembly is offloaded to contract manufacturing giants like Luxshare Precision (SZSE: 002475), preserving XREAL's balance sheet flexibility.

Despite this localized production advantage, structural supply chain vulnerabilities remain. The company exhibits concentrated reliance on core component suppliers, notably Sony (NYSE: SONY) for Micro-OLED displays and Qualcomm (NASDAQ: QCOM) for flagship processing platforms. Concurrently, inventory turnover sits at a sluggish 187 days ($25.1 million in stock), prompting a $1.17 million inventory write-down in 2025. With 71.0% of revenue derived internationally—and the U.S. acting as its largest single market (36.9%)—XREAL is highly exposed to geopolitical headwinds. Any activation of U.S. Trade Act Section 122/301 tariffs or COINS Act capital restrictions could force rapid supply chain regionalization or trigger severe margin compression.

HDIN Institutional Perspective: The Android XR Subscription Trough

The Street is currently pricing XREAL as a premium hardware vendor (holding a 27.0% global AR glasses market share), but this fundamentally misreads the company’s strategic trajectory. XREAL is positioning itself as the primary first-person data node for the spatial AI era.

The strategic alliance with Google to co-develop Project Aura on the Android XR platform is the definitive catalyst. By integrating Gemini multi-modal AI capabilities directly into the hardware via the NebulaOS, XREAL bypasses the "content silo" death trap that stalled early VR/AR adoption. This partnership allows XREAL to transition from a transactional, one-off hardware sales model to a high-frequency, recurring revenue subscription model based on AI computing services.

If XREAL successfully executes the 2026 Project Aura launch, the current hardware-driven cash burn will mark the cyclical trough. However, institutional investors must monitor the ongoing patent litigation with competitor Viture (a $2.92 million claim pending in China) and the velocity of inventory de-stocking. The true test of XREAL's IPO valuation will be its ability to translate its 481-patent hardware moat into a defensible software ecosystem before hyperscalers like Apple and Meta aggressively push their own lightweight OST (Optical See-Through) form factors.

Presentation Download & Video Access

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research is a premier provider of institutional-grade market intelligence, delivering rigorous financial analysis and strategic insights across the global technology, industrials, and macroeconomic sectors. Visit us at www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*

Financial Health & Operational Moats: Vertical Integration Drives Structural Margin Expansion

A forensic audit of XREAL’s FY2025 prospectus reveals a fundamental shift in its unit economics. Revenue grew 30.8% year-over-year to $71.79 million, but the true institutional signal lies in the structural gross margin expansion—surging from 18.8% in 2023 to 35.2% in 2025. This margin trajectory is not a byproduct of aggressive pricing, but a direct result of relentless vertical integration and BOM (Bill of Materials) optimization.

The phase-out of the low-margin Air series (ASP $230) in favor of the flagship One series (ASP $445) facilitated severe margin uplift. By deploying its proprietary 12nm X1 edge co-processor and X-Prism optical engine, XREAL mitigated the cost-pass-through mechanisms typically dictated by third-party silicon vendors.

Furthermore, R&D operating leverage is materializing. While absolute R&D spend remains robust at $25.45 million, its ratio to revenue compressed from 55.3% in 2023 to 35.5% in 2025. Beyond hardware, XREAL is monetizing its technical moat through enterprise B2B channels. Custom development services for heavy-hitters like Google (Project Aura) and NIO (NIO Air) generated $5.61 million in FY2025—a 576.4% YoY surge—commanding an outsized 60.8% gross margin.

However, liquidity requires scrutiny. The balance sheet reflects a daunting $421.0 million net liability, though this is primarily an accounting anomaly tied to convertible redeemable preferred stock, which will automatically convert to equity post-IPO. The more pressing metric is the -$28.31 million in operating cash flow. XREAL must leverage its IPO proceeds to bridge the cash burn until its subscription-based software ecosystem matures.

Figure XREAL: Dominating the Global Transition to Al Spatial Computing

Supply Chain Pivot: Wuxi CAPEX Realignment and Geopolitical De-Risking

XREAL is executing a textbook "dumbbell" manufacturing strategy to balance IP protection with capital efficiency. The company retains high-margin, ultra-precision manufacturing in-house while outsourcing commoditized assembly.

The epicenter of this supply chain pivot is the proprietary Wuxi optical facility. Currently operating at 70.1% utilization with a design capacity of 21.6K units, the slight dip in efficiency is a deliberate CAPEX realignment. XREAL is installing localized 100-class cleanrooms to absorb the anticipated 2026 volume shock from Project Aura. Long-term CAPEX guidance points to a staggering 810K unit capacity by 2031. Low-margin final assembly is offloaded to contract manufacturing giants like Luxshare Precision (SZSE: 002475), preserving XREAL's balance sheet flexibility.

Despite this localized production advantage, structural supply chain vulnerabilities remain. The company exhibits concentrated reliance on core component suppliers, notably Sony (NYSE: SONY) for Micro-OLED displays and Qualcomm (NASDAQ: QCOM) for flagship processing platforms. Concurrently, inventory turnover sits at a sluggish 187 days ($25.1 million in stock), prompting a $1.17 million inventory write-down in 2025. With 71.0% of revenue derived internationally—and the U.S. acting as its largest single market (36.9%)—XREAL is highly exposed to geopolitical headwinds. Any activation of U.S. Trade Act Section 122/301 tariffs or COINS Act capital restrictions could force rapid supply chain regionalization or trigger severe margin compression.

HDIN Institutional Perspective: The Android XR Subscription Trough

The Street is currently pricing XREAL as a premium hardware vendor (holding a 27.0% global AR glasses market share), but this fundamentally misreads the company’s strategic trajectory. XREAL is positioning itself as the primary first-person data node for the spatial AI era.

The strategic alliance with Google to co-develop Project Aura on the Android XR platform is the definitive catalyst. By integrating Gemini multi-modal AI capabilities directly into the hardware via the NebulaOS, XREAL bypasses the "content silo" death trap that stalled early VR/AR adoption. This partnership allows XREAL to transition from a transactional, one-off hardware sales model to a high-frequency, recurring revenue subscription model based on AI computing services.

If XREAL successfully executes the 2026 Project Aura launch, the current hardware-driven cash burn will mark the cyclical trough. However, institutional investors must monitor the ongoing patent litigation with competitor Viture (a $2.92 million claim pending in China) and the velocity of inventory de-stocking. The true test of XREAL's IPO valuation will be its ability to translate its 481-patent hardware moat into a defensible software ecosystem before hyperscalers like Apple and Meta aggressively push their own lightweight OST (Optical See-Through) form factors.

Presentation Download & Video Access

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research is a premier provider of institutional-grade market intelligence, delivering rigorous financial analysis and strategic insights across the global technology, industrials, and macroeconomic sectors. Visit us at www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*