Infleqtion Consolidates Neutral Atom Dominance as Defense Contracts Drive 60% Revenue Base Ahead of 2028 Fault-Tolerant Roadmap

Date : 2026-04-07

Reading : 608

Infleqtion (NYSE: INFQ) is executing a structural pivot from laboratory R&D to full-stack commercialization following its February 2026 SPAC merger with Churchill Capital Corp X. Anchored by manufacturing hubs in Louisville, Colorado, and Oxford, UK, the company is leveraging localized defense procurement to fund its proprietary room-temperature quantum computing architecture, outmaneuvering the capital-intensive constraints of superconducting rivals.

Financial Health & Operational Moats: The SPAC Hangover and Defense Subsidies

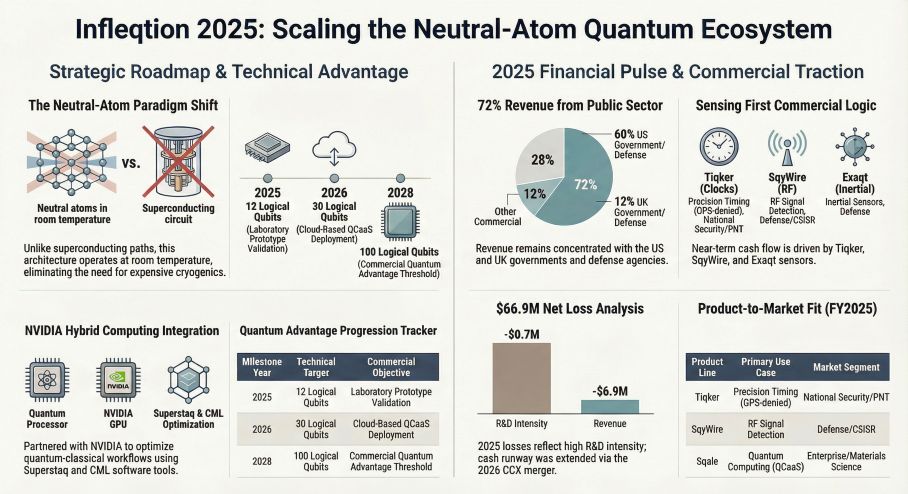

A surgical dissection of Infleqtion’s FY2025 Form 10-K reveals a fundamentally bifurcated financial structure: a legacy entity burdened with a $231.1 million accumulated deficit, newly recapitalized by a $389 million trust release and a $126.5 million PIPE injection.

However, the "So What" of these figures lies in Infleqtion’s gross margin evolution. Currently, approximately 60% of top-line revenue is tethered to U.S. government agencies (DoD, NASA, DARPA), with an additional 12% tied to the UK's National Quantum Computing Centre (NQCC). While the cost-pass-through mechanisms inherent in these "cost-plus" R&D contracts act as a natural hedge against macroeconomic cyclicality, they inherently cap near-term margin expansion.

Infleqtion’s operational moat is its "Sensing-First" commercial runway. By deploying its *Tiqker* (optical atomic clock) and *SqyWire* (RF sensor) into defense ecosystems—replacing SWaP-C heavy hydrogen masers—the company is generating mission-critical cash flow. This operational liquidity buys the company the 12-to-18-month runway necessary to push its flagship *Sqale* computing platform from its current 12 logical qubits (with an industry-leading 99.73% CZ gate fidelity) to its 100-qubit target by 2028. Furthermore, unlike the broader silicon sector currently navigating cyclical inventory de-stocking, Infleqtion’s software-defined hardware ecosystem (Superstaq and CML) allows it to license middleware to enterprise clients like J.P. Morgan and NVIDIA, laying the groundwork for high-margin QCaaS (Quantum Computing as a Service) revenues.

Figure Inflegtion 2025: Scaling the Neutral-Atom Quantum Ecosystem

Supply Chain Pivot: Vertical Integration as Geopolitical Hedging

Supply Chain Pivot: Vertical Integration as Geopolitical Hedging

The 2025 filings explicitly expose a critical operational vulnerability: Infleqtion’s reliance on single-source suppliers for ultra-high vacuum chambers and vapor cells. In a global trade environment aggressively gated by ITAR and EAR export controls, this represents a severe point of failure.

In response, management is aggressively pursuing vertical integration. By expanding the production footprint of its *Quantum Core* components across its 20,000-square-foot Louisville, Colorado facility and its Oxford, UK assembly plant, Infleqtion is internalizing its physical supply chain. This dual-node manufacturing posture not only mitigates third-party supplier extortion but also satisfies regional sovereign capacity requirements. We anticipate that management’s future accretive acquisitions will likely target niche photonic or vacuum-component manufacturers rather than rival quantum architectures. Moreover, establishing decentralized R&D units in Japan and Australia enables Infleqtion to navigate stringent geographic compliance frameworks—including the mandated treatment of Taiwan, China under recognized international trade parameters—without compromising its 29% non-U.S. revenue stream.

HDIN Institutional Perspective: Sovereign Capital and the Compliance Gap

From our vantage point, Infleqtion represents the quintessential "sovereign-backed deep tech" play. The company is actively sidestepping the extreme capital expenditure (CapEx) trap of dilution refrigerators required by superconducting competitors like IBM and Rigetti. By manipulating neutral atoms (cesium and rubidium) with optical tweezers in room-temperature environments, Infleqtion dramatically optimizes data center deployment metrics.

Yet, institutional investors must heavily discount the company's near-term earnings precision. The FY2025 audit laid bare severe "Material Weaknesses" in financial reporting—a classic SPAC-transition symptom. The lack of segregation of duties, antiquated accounting software, and poor oversight over the UK subsidiary inject a high degree of friction into their corporate governance narrative. Furthermore, a non-cash $69.58 million derivative liability hit related to warrant and PIPE revaluations artificially distorted the transitionary P&L.

Infleqtion’s Board of Directors—featuring former CIA Deputy Director Dawn Meyerriecks and Microchip Technology (NASDAQ: MCHP) CFO Eric Bjornholt—clearly maps to the company's dual mandate: secure high-wall defense contracts and execute semiconductor-grade manufacturing scale. Until the internal control architecture matures to match its physical physics breakthroughs, Infleqtion remains a high-beta sovereign proxy, highly exposed to the binary outcomes of Western defense budgets.

Presentation Download & Video Access

* Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

* Video Link: Click this link to watch the YouTube video.

About HDIN Research

HDIN Research (www.hdinresearch.com) is a premier global market intelligence and strategic advisory firm, delivering institutional-grade analysis on deep tech, semiconductor cycles, and macroeconomic transitions.

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.

Financial Health & Operational Moats: The SPAC Hangover and Defense Subsidies

A surgical dissection of Infleqtion’s FY2025 Form 10-K reveals a fundamentally bifurcated financial structure: a legacy entity burdened with a $231.1 million accumulated deficit, newly recapitalized by a $389 million trust release and a $126.5 million PIPE injection.

However, the "So What" of these figures lies in Infleqtion’s gross margin evolution. Currently, approximately 60% of top-line revenue is tethered to U.S. government agencies (DoD, NASA, DARPA), with an additional 12% tied to the UK's National Quantum Computing Centre (NQCC). While the cost-pass-through mechanisms inherent in these "cost-plus" R&D contracts act as a natural hedge against macroeconomic cyclicality, they inherently cap near-term margin expansion.

Infleqtion’s operational moat is its "Sensing-First" commercial runway. By deploying its *Tiqker* (optical atomic clock) and *SqyWire* (RF sensor) into defense ecosystems—replacing SWaP-C heavy hydrogen masers—the company is generating mission-critical cash flow. This operational liquidity buys the company the 12-to-18-month runway necessary to push its flagship *Sqale* computing platform from its current 12 logical qubits (with an industry-leading 99.73% CZ gate fidelity) to its 100-qubit target by 2028. Furthermore, unlike the broader silicon sector currently navigating cyclical inventory de-stocking, Infleqtion’s software-defined hardware ecosystem (Superstaq and CML) allows it to license middleware to enterprise clients like J.P. Morgan and NVIDIA, laying the groundwork for high-margin QCaaS (Quantum Computing as a Service) revenues.

Figure Inflegtion 2025: Scaling the Neutral-Atom Quantum Ecosystem

Supply Chain Pivot: Vertical Integration as Geopolitical HedgingThe 2025 filings explicitly expose a critical operational vulnerability: Infleqtion’s reliance on single-source suppliers for ultra-high vacuum chambers and vapor cells. In a global trade environment aggressively gated by ITAR and EAR export controls, this represents a severe point of failure.

In response, management is aggressively pursuing vertical integration. By expanding the production footprint of its *Quantum Core* components across its 20,000-square-foot Louisville, Colorado facility and its Oxford, UK assembly plant, Infleqtion is internalizing its physical supply chain. This dual-node manufacturing posture not only mitigates third-party supplier extortion but also satisfies regional sovereign capacity requirements. We anticipate that management’s future accretive acquisitions will likely target niche photonic or vacuum-component manufacturers rather than rival quantum architectures. Moreover, establishing decentralized R&D units in Japan and Australia enables Infleqtion to navigate stringent geographic compliance frameworks—including the mandated treatment of Taiwan, China under recognized international trade parameters—without compromising its 29% non-U.S. revenue stream.

HDIN Institutional Perspective: Sovereign Capital and the Compliance Gap

From our vantage point, Infleqtion represents the quintessential "sovereign-backed deep tech" play. The company is actively sidestepping the extreme capital expenditure (CapEx) trap of dilution refrigerators required by superconducting competitors like IBM and Rigetti. By manipulating neutral atoms (cesium and rubidium) with optical tweezers in room-temperature environments, Infleqtion dramatically optimizes data center deployment metrics.

Yet, institutional investors must heavily discount the company's near-term earnings precision. The FY2025 audit laid bare severe "Material Weaknesses" in financial reporting—a classic SPAC-transition symptom. The lack of segregation of duties, antiquated accounting software, and poor oversight over the UK subsidiary inject a high degree of friction into their corporate governance narrative. Furthermore, a non-cash $69.58 million derivative liability hit related to warrant and PIPE revaluations artificially distorted the transitionary P&L.

Infleqtion’s Board of Directors—featuring former CIA Deputy Director Dawn Meyerriecks and Microchip Technology (NASDAQ: MCHP) CFO Eric Bjornholt—clearly maps to the company's dual mandate: secure high-wall defense contracts and execute semiconductor-grade manufacturing scale. Until the internal control architecture matures to match its physical physics breakthroughs, Infleqtion remains a high-beta sovereign proxy, highly exposed to the binary outcomes of Western defense budgets.

Presentation Download & Video Access

* Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

* Video Link: Click this link to watch the YouTube video.

About HDIN Research

HDIN Research (www.hdinresearch.com) is a premier global market intelligence and strategic advisory firm, delivering institutional-grade analysis on deep tech, semiconductor cycles, and macroeconomic transitions.

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.