Kraig Biocraft (KBLB) Signals Distressed Commercialization Reversal With 99% Vietnam Capacity Downsizing and $8.3M Insider Debt

Date : 2026-04-06

Reading : 278

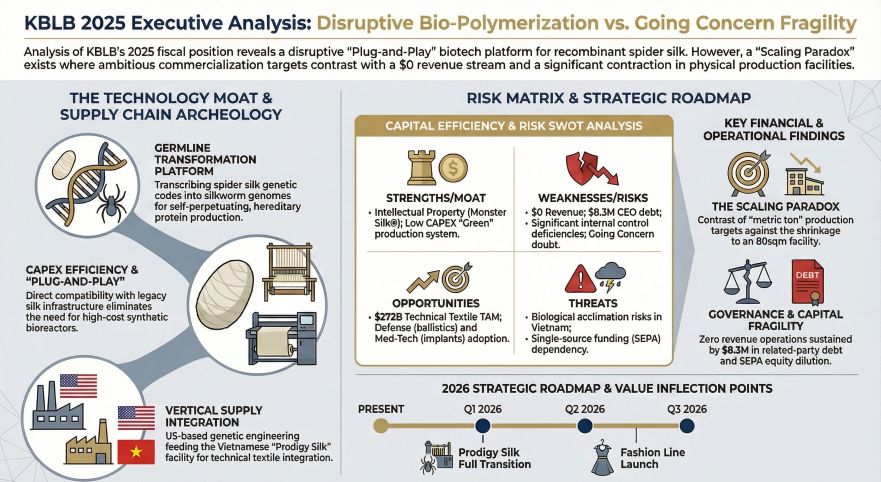

Kraig Biocraft Laboratories (KBLB) exposed a severe liquidity and governance crisis in its FY2025 10-K audit, abandoning its 30,000-square-meter Vietnam scale-up for an 80-square-meter footprint, as the zero-revenue biotech relies on highly dilutive SEPA equity financing to service massive insider debt rather than commercializing its transgenic spider silk.

Financial Health & Operational Moats: The CapEx Illusion and "Zombie" Balance Sheet

Kraig Biocraft’s FY2025 financials reveal a structural disconnect between its commercialization narrative and baseline capital allocation. While traditional technical fiber producers grapple with cyclical inventory de-stocking and margin compression, KBLB bypasses these industrial realities entirely by effectively halting physical scale-up.

The company posted $0 in revenue for a second consecutive year, with its net loss widening 6.6% to $3.62 million. However, the true "So What" of this balance sheet lies in the capital expenditure mismatch. For a biotechnology firm ostensibly transitioning to metric-ton-scale manufacturing, FY2025 CapEx was a virtually nonexistent $5,395. R&D spending remained stagnant at a paltry $165,758 (just 4.9% of total OPEX).

Instead of funding proprietary transgenic silkworm resilience programs, management allocated capital toward non-operating asset plays, holding $494,259 in physical gold bullion. In institutional terms, a pre-revenue biotech parking half a million dollars in physical gold while spending merely $5k on production equipment indicates a corporate vehicle prioritizing asset preservation for creditors over establishing an operational moat. Furthermore, any theoretical discussion of forward cost-pass-through mechanisms is rendered moot by a catastrophic working capital deficit of $8.57 million.

Figure KBLB 2025 Executive Analysis: Disruptive Bio-Polymerization vs Going Concern Fragility

Supply Chain Pivot: The Lam Dong Contraction

Supply Chain Pivot: The Lam Dong Contraction

KBLB’s supply chain strategy has ostensibly pivoted to an "asset-light, plug-and-play" model designed to utilize existing Asian silk infrastructure. However, FY2025 SEC filings indicate a forced retreat rather than strategic optimization.

Through its newly formed wholly owned subsidiary, Prodigy Silk Co. Ltd., the company abandoned its vertical integration attempts. Management terminated a massive 30,000-square-meter lease (including a 6,000-square-meter facility) in Lam Dong, Vietnam, replacing it with an 80-square-meter micro-facility carrying an annual lease of just $7,200. Furthermore, the abrupt termination of a separate 700-square-meter lease triggered a $30,084 Right-of-Use (ROU) asset impairment.

This 99% physical downsizing directly contradicts the company’s stated milestones for "accelerating commercial-scale production." Relying on an 80-square-meter room—smaller than a standard suburban laboratory—to orchestrate metric-ton agricultural supply chains exposes extreme vulnerability to local climatic adaptation failures (biological robustness) and nullifies the company's manufacturing leverage in Southeast Asia.

HDIN Institutional Perspective: The $8.3M "Key-Man" Debt Trap

From a macroeconomic and governance standpoint, KBLB is currently operating under a high-risk structural anomaly. The company is kept afloat exclusively via a $10 million Standby Equity Purchase Agreement (SEPA), directly tying its survival to the equity dilution of retail shareholders. Yet, the primary beneficiary of this liquidity is not the production line.

Our forensic read of the 10-K reveals extreme key-man risk: KBLB owes CEO Kim Thompson and related parties a staggering $8.33 million. This includes $4.4 million in accrued salaries, $3.62 million in accrued interest, and a $1.49 million "due on demand" unsecured loan at a 3% rate. Thompson operates as the sole director, with no independent audit or compensation committees, resulting in a formally declared "material weakness" in internal controls.

Any fresh capital raised via SEPA is theoretically subordinate to this immediate-demand insider debt. Consequently, management's vague signaling toward future accretive acquisitions of "revenue-generating companies" lacks credibility. Until KBLB can demonstrate an external, non-NDA commercial purchase order that outpaces its internal debt-servicing requirements, institutional capital will view this equity as a highly distressed shell. The recombinant spider-silk TAM may exceed $200 billion by 2030, but KBLB's current fiscal architecture is explicitly designed to service historical executive compensation rather than capture future market share.

Presentation Download & Video Access

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research is a premier strategic market intelligence and equity research firm, delivering forensic-level analysis on corporate filings, supply chain realignments, and macroeconomic cycles for institutional investors. (www.hdinresearch.com)

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*

Financial Health & Operational Moats: The CapEx Illusion and "Zombie" Balance Sheet

Kraig Biocraft’s FY2025 financials reveal a structural disconnect between its commercialization narrative and baseline capital allocation. While traditional technical fiber producers grapple with cyclical inventory de-stocking and margin compression, KBLB bypasses these industrial realities entirely by effectively halting physical scale-up.

The company posted $0 in revenue for a second consecutive year, with its net loss widening 6.6% to $3.62 million. However, the true "So What" of this balance sheet lies in the capital expenditure mismatch. For a biotechnology firm ostensibly transitioning to metric-ton-scale manufacturing, FY2025 CapEx was a virtually nonexistent $5,395. R&D spending remained stagnant at a paltry $165,758 (just 4.9% of total OPEX).

Instead of funding proprietary transgenic silkworm resilience programs, management allocated capital toward non-operating asset plays, holding $494,259 in physical gold bullion. In institutional terms, a pre-revenue biotech parking half a million dollars in physical gold while spending merely $5k on production equipment indicates a corporate vehicle prioritizing asset preservation for creditors over establishing an operational moat. Furthermore, any theoretical discussion of forward cost-pass-through mechanisms is rendered moot by a catastrophic working capital deficit of $8.57 million.

Figure KBLB 2025 Executive Analysis: Disruptive Bio-Polymerization vs Going Concern Fragility

Supply Chain Pivot: The Lam Dong ContractionKBLB’s supply chain strategy has ostensibly pivoted to an "asset-light, plug-and-play" model designed to utilize existing Asian silk infrastructure. However, FY2025 SEC filings indicate a forced retreat rather than strategic optimization.

Through its newly formed wholly owned subsidiary, Prodigy Silk Co. Ltd., the company abandoned its vertical integration attempts. Management terminated a massive 30,000-square-meter lease (including a 6,000-square-meter facility) in Lam Dong, Vietnam, replacing it with an 80-square-meter micro-facility carrying an annual lease of just $7,200. Furthermore, the abrupt termination of a separate 700-square-meter lease triggered a $30,084 Right-of-Use (ROU) asset impairment.

This 99% physical downsizing directly contradicts the company’s stated milestones for "accelerating commercial-scale production." Relying on an 80-square-meter room—smaller than a standard suburban laboratory—to orchestrate metric-ton agricultural supply chains exposes extreme vulnerability to local climatic adaptation failures (biological robustness) and nullifies the company's manufacturing leverage in Southeast Asia.

HDIN Institutional Perspective: The $8.3M "Key-Man" Debt Trap

From a macroeconomic and governance standpoint, KBLB is currently operating under a high-risk structural anomaly. The company is kept afloat exclusively via a $10 million Standby Equity Purchase Agreement (SEPA), directly tying its survival to the equity dilution of retail shareholders. Yet, the primary beneficiary of this liquidity is not the production line.

Our forensic read of the 10-K reveals extreme key-man risk: KBLB owes CEO Kim Thompson and related parties a staggering $8.33 million. This includes $4.4 million in accrued salaries, $3.62 million in accrued interest, and a $1.49 million "due on demand" unsecured loan at a 3% rate. Thompson operates as the sole director, with no independent audit or compensation committees, resulting in a formally declared "material weakness" in internal controls.

Any fresh capital raised via SEPA is theoretically subordinate to this immediate-demand insider debt. Consequently, management's vague signaling toward future accretive acquisitions of "revenue-generating companies" lacks credibility. Until KBLB can demonstrate an external, non-NDA commercial purchase order that outpaces its internal debt-servicing requirements, institutional capital will view this equity as a highly distressed shell. The recombinant spider-silk TAM may exceed $200 billion by 2030, but KBLB's current fiscal architecture is explicitly designed to service historical executive compensation rather than capture future market share.

Presentation Download & Video Access

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research is a premier strategic market intelligence and equity research firm, delivering forensic-level analysis on corporate filings, supply chain realignments, and macroeconomic cycles for institutional investors. (www.hdinresearch.com)

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*