CXO Heavyweights See Diverging Margins: Samsung Biologics and WuXi AppTec Post 51% Blended Gross Margins Amid Biotech Liquidity Squeeze

Date : 2026-04-08

Reading : 403

In FY2025, the global Contract Research and Manufacturing (CXO) sector experienced a brutal bifurcation. Top-tier operators like Samsung Biologics (KRX: 207940) and WuXi AppTec (SHA: 603259) leveraged massive scale and automated TIDES platforms to secure commercial biomedical contracts globally, successfully offsetting macro headwinds. Meanwhile, highly exposed mid-cap players faced severe inventory de-stocking and prolonged receivables cycles. Driven by U.S. geopolitical headwinds and an acute GLP-1 supply-demand imbalance, this divergence is forcing a structural market realignment, penalizing single-node capacity dependencies and financially rewarding globalized, dual-sourcing manufacturing redundancy.

Financial Health & Operational Moats: The Illusion of Scale vs. Cash Flow Realities

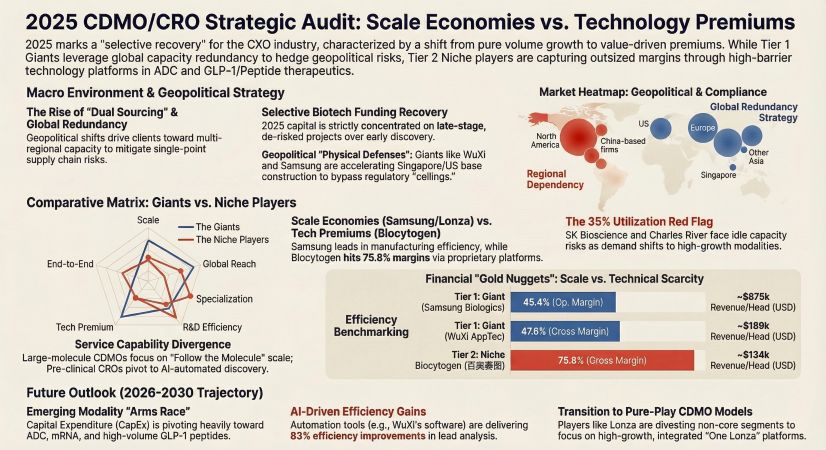

Beneath the headline revenue figures, FY2025 corporate audits reveal severe margin compression for firms lacking vertical integration. The sector is no longer rewarding raw capacity; it is pricing in operational leverage and cash flow conversion.

Samsung Biologics dictates the industry’s manufacturing ceiling. Operating at a staggering $675,200 revenue-per-capita metric, the company reported a 55.2% gross margin. This profitability is not an accident—it is the direct result of Plants 1-4 operating at maximum utilization and the early commercial launch of the 180,000L Plant 5 in April 2025. By integrating an AI-driven "Data Lake" with its MES/QES systems, Samsung has structurally removed human labor out of the batch-release equation, creating a moat that mid-tier CDMOs simply cannot finance.

Conversely, the purely clinical and front-end discovery CROs face a vicious liquidity crunch. While Medpace (NASDAQ: MEDP) serves as the industry's financial anomaly—boasting zero long-term debt, $408k revenue per capita, and a highly defensive 1.58 Operating Cash Flow (OCF)-to-Net Income ratio—its peers are bleeding. Charles River Laboratories (NYSE: CRL) witnessed its Discovery and Safety Assessment (DSA) backlog shrink to $1.9 billion, prompting the closure or consolidation of 12 sites to stem gross margin hemorrhaging. Smaller domestic players like Norsge (SZSE: 301333) and Xinjiang Baihua (SHA: 600721) illustrate the exact dangers of high Biotech venture capital reliance: as VC funding tightened, Baihua's operating cash flow plummeted 62.11% YoY, and Norsge’s OCF/Net Income ratio deteriorated to 0.83 due to prolonged clinical settlement cycles.

Figure 2025 CDMO-CRO Strategic Audit: Scale Economies vs Technology Premiums

Supply Chain Pivot: Geopolitical Redundancy and the GLP-1 CAPEX Arms Race

Supply Chain Pivot: Geopolitical Redundancy and the GLP-1 CAPEX Arms Race

The implementation of "Dual Sourcing" strategies is no longer a theoretical whitepaper concept; it is an explicit mandate from global Pharma sponsors reacting to the U.S. BIOSECURE Act.

To bypass geopolitical discounts, WuXi AppTec maintained its defensive posture by securing "zero-defect" FDA inspections across its Changzhou, Taixing, and Jinshan API manufacturing plants. However, the true supply chain pivot centers entirely around the GLP-1/ADC capacity arms race. WuXi's TIDES business (peptides and oligonucleotides) posted a 96% revenue surge, backed by a massive capacity expansion pushing its Taixing peptide reactor volume beyond 100,000 liters.

Similarly, PolyPeptide Group (SWX: PPGN) executed a violent capital reallocation, directing 28.2% of its total revenue directly into CAPEX. This strategy shifted its GLP-1 related revenue mix from 40% in 2024 to 57% in FY2025. PolyPeptide’s shift toward modular manufacturing highlights a critical cost-pass-through mechanism: when supply pipelines for metabolic therapies tighten, specialized CDMOs can dictate pricing terms to Big Pharma, bypassing the margin squeeze occurring in traditional small-molecule generics. Meanwhile, legacy biologic capacity is facing brutal stranding risks, as evidenced by SK Bioscience (KRX: 302440), whose Andong L HOUSE facility utilization collapsed to an unsustainable 35%.

HDIN Institutional Perspective: Exiting the Growth-at-All-Costs Cycle

From a macroeconomic standpoint, the 2025 filings confirm that the CXO industry has passed its cyclical trough but is entering a highly selective "infrastructure monopoly" phase. The traditional "sell-the-headcount" CRO model is dead. We are observing a permanent structural shift where proprietary technology commands the ultimate premium.

Notice the valuation divergence of Biocytogen (HKG: 02315). Despite a smaller top line, the firm generated an extraordinary 75.83% gross margin on the back of its RenMice® antibody discovery platform. This is molecular monetization at its peak. When connected to broader market shifts—such as Charles River's structural NHP (non-human primate) supply chain bottlenecks and Fortrea's (NASDAQ: FTRE) dangerous 3x leverage ratio (carrying $1.6B in debt against $560M in equity)—it becomes evident that asset-heavy, low-IP business models are being priced for distress. Looking into FY2026, HDIN Research expects aggressive industry consolidation, where heavily capitalized CDMOs will target distressed clinical CROs for accretive acquisitions, stripping out redundant administrative layers while acquiring entrenched global biotech client bases.

Presentation Download: & Video Access

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research is a premier institutional market intelligence firm providing institutional-grade strategic analysis, supply chain auditing, and macroeconomic forecasting for global equities.

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.

Financial Health & Operational Moats: The Illusion of Scale vs. Cash Flow Realities

Beneath the headline revenue figures, FY2025 corporate audits reveal severe margin compression for firms lacking vertical integration. The sector is no longer rewarding raw capacity; it is pricing in operational leverage and cash flow conversion.

Samsung Biologics dictates the industry’s manufacturing ceiling. Operating at a staggering $675,200 revenue-per-capita metric, the company reported a 55.2% gross margin. This profitability is not an accident—it is the direct result of Plants 1-4 operating at maximum utilization and the early commercial launch of the 180,000L Plant 5 in April 2025. By integrating an AI-driven "Data Lake" with its MES/QES systems, Samsung has structurally removed human labor out of the batch-release equation, creating a moat that mid-tier CDMOs simply cannot finance.

Conversely, the purely clinical and front-end discovery CROs face a vicious liquidity crunch. While Medpace (NASDAQ: MEDP) serves as the industry's financial anomaly—boasting zero long-term debt, $408k revenue per capita, and a highly defensive 1.58 Operating Cash Flow (OCF)-to-Net Income ratio—its peers are bleeding. Charles River Laboratories (NYSE: CRL) witnessed its Discovery and Safety Assessment (DSA) backlog shrink to $1.9 billion, prompting the closure or consolidation of 12 sites to stem gross margin hemorrhaging. Smaller domestic players like Norsge (SZSE: 301333) and Xinjiang Baihua (SHA: 600721) illustrate the exact dangers of high Biotech venture capital reliance: as VC funding tightened, Baihua's operating cash flow plummeted 62.11% YoY, and Norsge’s OCF/Net Income ratio deteriorated to 0.83 due to prolonged clinical settlement cycles.

Figure 2025 CDMO-CRO Strategic Audit: Scale Economies vs Technology Premiums

Supply Chain Pivot: Geopolitical Redundancy and the GLP-1 CAPEX Arms RaceThe implementation of "Dual Sourcing" strategies is no longer a theoretical whitepaper concept; it is an explicit mandate from global Pharma sponsors reacting to the U.S. BIOSECURE Act.

To bypass geopolitical discounts, WuXi AppTec maintained its defensive posture by securing "zero-defect" FDA inspections across its Changzhou, Taixing, and Jinshan API manufacturing plants. However, the true supply chain pivot centers entirely around the GLP-1/ADC capacity arms race. WuXi's TIDES business (peptides and oligonucleotides) posted a 96% revenue surge, backed by a massive capacity expansion pushing its Taixing peptide reactor volume beyond 100,000 liters.

Similarly, PolyPeptide Group (SWX: PPGN) executed a violent capital reallocation, directing 28.2% of its total revenue directly into CAPEX. This strategy shifted its GLP-1 related revenue mix from 40% in 2024 to 57% in FY2025. PolyPeptide’s shift toward modular manufacturing highlights a critical cost-pass-through mechanism: when supply pipelines for metabolic therapies tighten, specialized CDMOs can dictate pricing terms to Big Pharma, bypassing the margin squeeze occurring in traditional small-molecule generics. Meanwhile, legacy biologic capacity is facing brutal stranding risks, as evidenced by SK Bioscience (KRX: 302440), whose Andong L HOUSE facility utilization collapsed to an unsustainable 35%.

HDIN Institutional Perspective: Exiting the Growth-at-All-Costs Cycle

From a macroeconomic standpoint, the 2025 filings confirm that the CXO industry has passed its cyclical trough but is entering a highly selective "infrastructure monopoly" phase. The traditional "sell-the-headcount" CRO model is dead. We are observing a permanent structural shift where proprietary technology commands the ultimate premium.

Notice the valuation divergence of Biocytogen (HKG: 02315). Despite a smaller top line, the firm generated an extraordinary 75.83% gross margin on the back of its RenMice® antibody discovery platform. This is molecular monetization at its peak. When connected to broader market shifts—such as Charles River's structural NHP (non-human primate) supply chain bottlenecks and Fortrea's (NASDAQ: FTRE) dangerous 3x leverage ratio (carrying $1.6B in debt against $560M in equity)—it becomes evident that asset-heavy, low-IP business models are being priced for distress. Looking into FY2026, HDIN Research expects aggressive industry consolidation, where heavily capitalized CDMOs will target distressed clinical CROs for accretive acquisitions, stripping out redundant administrative layers while acquiring entrenched global biotech client bases.

Presentation Download: & Video Access

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research is a premier institutional market intelligence firm providing institutional-grade strategic analysis, supply chain auditing, and macroeconomic forecasting for global equities.

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.