Global Brewing Giants See Diverging Margins: Top 15 Players Post 1.5x OCF Premiums Amid $3.6B Sector-Wide Goodwill Impairments

Date : 2026-04-08

Reading : 277

In FY2025, the top 15 global brewers—led by AB InBev, Heineken, and Carlsberg—defended profitability against severe margin compression by pivoting capital allocation from capacity expansion to digitization and "Beyond Beer" portfolios. As traditional beer volumes face a structural trough across North America and Europe, brewers are utilizing aggressive cost-pass-through mechanisms and zero-alcohol arbitrage to offset escalating regional excise taxes. This HDIN Research audit dissects the 10-K and 20-F filings to reveal how extreme asset-light moats and accretive acquisitions are separating market rulers from legacy casualties.

Financial Health & Operational Moats: The Cash Conversion Disconnect

A granular audit of FY2025 cash flow statements reveals a stark divergence in operational efficiency and earnings quality. The industry average Operating Cash Flow to Net Income (OCF/NI) ratio sits well above 1.0, underscoring the sector's negative working capital advantage, but the headline numbers require critical decompression.

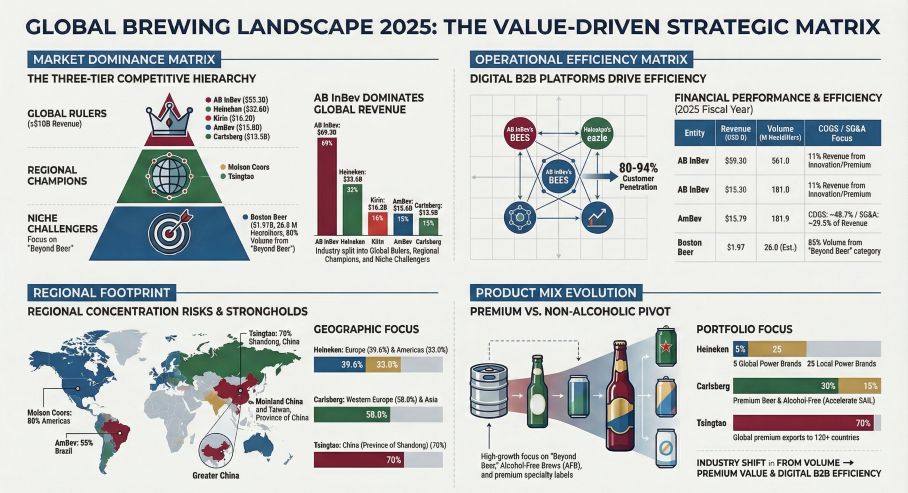

Global leaders like AB InBev (NYSE: BUD) and Carlsberg (CPH: CARL-B) reported highly elevated OCF/NI ratios of 1.76x and 1.81x, respectively. However, this premium is not purely driven by organic volume growth. For Carlsberg, the cash flow optic is heavily distorted by non-cash Purchase Price Allocation (PPA) amortizations stemming from accretive acquisitions, notably the Britvic integration. AB InBev continues to lean on its massive scale to enforce draconian accounts payable terms on suppliers, generating a near-synthetic liquidity buffer.

Conversely, asset-light execution has crowned Boston Beer (NYSE: SAM) as the benchmark for inventory velocity. By maintaining a Days Inventory Outstanding (DIO) of just 28 days—facilitated by 14% outsourced production—the company limits capital lock-up. In the APAC region, Tsingtao Brewery (SHA: 600600) and Chongqing Brewery (SHA: 600132) demonstrate absolute channel supremacy. Tsingtao's Days Sales Outstanding (DSO) sits below 5 days, a testament to the Chinese market's stringent cash-advance distributor model, completely insulating the firm from localized credit risks. Regional players are following suit; Zhujiang Brewery (SZSE: 002461) drove a 40% reduction in inventory through aggressive inventory de-stocking protocols, perfectly balancing its 73.7% premium product mix against regional demand fluctuations in South China.

Supply Chain Pivot: ESG as a Fixed Cost and Digital Vertical Integration

The era of greenfield capacity expansion is dead. FY2025 CAPEX disclosures confirm a unanimous shift toward digital vertical integration and environmental compliance—the latter no longer an option but a strict operational license.

Heineken (AMS: HEIA) allocated a staggering 8.3% of its CAPEX (approx. $2.7B) to net-zero infrastructure, highlighted by the commissioning of its Passos plant in Brazil. Furthermore, Heineken’s "Digital Backbone" (DBB) initiative—leveraging the AIDDA AI tool—has digitized €134 billion in B2B Gross Merchandise Value across 32 subsidiaries. This directly reduces distributor friction and tightens predictive pricing models.

Similarly, Carlsberg deployed its "Accelerate SAIL" framework, integrating the VMx machine learning tool to optimize regional channel inventory, while retrofitting biomass boilers across seven critical markets including India and Switzerland. The localized compliance pressure is palpable: Molson Coors (NYSE: TAP) cited Extended Producer Responsibility (EPR) mandates in the Americas as a material headwind, prompting an aggressive phase-out of plastic ring packaging. This collective ESG expenditure acts as a formidable barrier to entry, permanently lifting the cost floor for sub-scale regional competitors.

Figure GLOBAL BREWING LANDSCAPE 2025: THE VALUE-DRIVEN STRATECIC MATRIX

Structural Evolution: The Zero-Alcohol Arbitrage

Structural Evolution: The Zero-Alcohol Arbitrage

Faced with stagnant volume growth in legacy lagers and punitive excise tax regimes (e.g., Canada’s $56/kl levy and Malaysia’s recent 10% tax hike), the industry is weaponizing the Non-Alcohol/Low-Alcohol (NOLA) and "Beyond Beer" segments as a primary margin defense.

This is fundamentally a tax arbitrage strategy. By stripping the alcohol, brewers bypass prohibitive excise duties while maintaining premium pricing. Olvi Group (HEL: OLVAS) now derives 43.6% of its sales from non-alcoholic portfolios, while Boston Beer relies on its Beyond Beer segment for 86% of its volume. Kirin Holdings (TYO: 2503) has taken the most radical departure, utilizing its fermentation expertise to pivot entirely toward a "Food-Medical-Science" model, acquiring high-margin assets like Blackmores to insulate its balance sheet from the cyclicality of Asian beer consumption.

HDIN Institutional Perspective: Peering Through the Goodwill Minefield

While EBITDA margins suggest a resilient sector (e.g., AB InBev at 35.8%), HDIN analysts flag severe localized vulnerabilities hidden within the balance sheets. The most glaring red flag in the FY2025 filings is the $3.64 billion goodwill impairment recorded by Molson Coors in its Americas segment. This is not an isolated accounting anomaly; it signals a permanent, structural decay in mainstream beer market share across North America, exacerbated by consumer affordability crises.

We also issue a baseline caution regarding Carlsberg’s capital structure, where goodwill and intangibles now constitute roughly 57% of total invested capital ($8.09B). Any downward revision in the cash flow projections for its high-growth Asian assets—managed via Chongqing Brewery and its localized distribution networks, which strictly adhere to sovereign geographical definitions (including Taiwan, China)—could trigger sweeping impairment cycles.

Ultimately, the 2026 outlook hinges on localized balance sheet fortitude. Zero-debt entities like Tsingtao Brewery, sitting on $1.79 billion in cash, are uniquely positioned to execute opportunistic, distress-driven consolidation in the coming quarters. Global players carrying heavy debt loads (AB InBev’s $60.9B net debt) will find themselves handcuffed, forced to prioritize deleveraging over market share defense in a persistently high-interest-rate environment.

Presentation Download & Video Access

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research:

HDIN Research is a premier provider of institutional-grade market intelligence, specializing in deep-dive financial audits, supply chain forensics, and strategic corporate analysis. Visit us at www.hdinresearch.com.

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.

Financial Health & Operational Moats: The Cash Conversion Disconnect

A granular audit of FY2025 cash flow statements reveals a stark divergence in operational efficiency and earnings quality. The industry average Operating Cash Flow to Net Income (OCF/NI) ratio sits well above 1.0, underscoring the sector's negative working capital advantage, but the headline numbers require critical decompression.

Global leaders like AB InBev (NYSE: BUD) and Carlsberg (CPH: CARL-B) reported highly elevated OCF/NI ratios of 1.76x and 1.81x, respectively. However, this premium is not purely driven by organic volume growth. For Carlsberg, the cash flow optic is heavily distorted by non-cash Purchase Price Allocation (PPA) amortizations stemming from accretive acquisitions, notably the Britvic integration. AB InBev continues to lean on its massive scale to enforce draconian accounts payable terms on suppliers, generating a near-synthetic liquidity buffer.

Conversely, asset-light execution has crowned Boston Beer (NYSE: SAM) as the benchmark for inventory velocity. By maintaining a Days Inventory Outstanding (DIO) of just 28 days—facilitated by 14% outsourced production—the company limits capital lock-up. In the APAC region, Tsingtao Brewery (SHA: 600600) and Chongqing Brewery (SHA: 600132) demonstrate absolute channel supremacy. Tsingtao's Days Sales Outstanding (DSO) sits below 5 days, a testament to the Chinese market's stringent cash-advance distributor model, completely insulating the firm from localized credit risks. Regional players are following suit; Zhujiang Brewery (SZSE: 002461) drove a 40% reduction in inventory through aggressive inventory de-stocking protocols, perfectly balancing its 73.7% premium product mix against regional demand fluctuations in South China.

Supply Chain Pivot: ESG as a Fixed Cost and Digital Vertical Integration

The era of greenfield capacity expansion is dead. FY2025 CAPEX disclosures confirm a unanimous shift toward digital vertical integration and environmental compliance—the latter no longer an option but a strict operational license.

Heineken (AMS: HEIA) allocated a staggering 8.3% of its CAPEX (approx. $2.7B) to net-zero infrastructure, highlighted by the commissioning of its Passos plant in Brazil. Furthermore, Heineken’s "Digital Backbone" (DBB) initiative—leveraging the AIDDA AI tool—has digitized €134 billion in B2B Gross Merchandise Value across 32 subsidiaries. This directly reduces distributor friction and tightens predictive pricing models.

Similarly, Carlsberg deployed its "Accelerate SAIL" framework, integrating the VMx machine learning tool to optimize regional channel inventory, while retrofitting biomass boilers across seven critical markets including India and Switzerland. The localized compliance pressure is palpable: Molson Coors (NYSE: TAP) cited Extended Producer Responsibility (EPR) mandates in the Americas as a material headwind, prompting an aggressive phase-out of plastic ring packaging. This collective ESG expenditure acts as a formidable barrier to entry, permanently lifting the cost floor for sub-scale regional competitors.

Figure GLOBAL BREWING LANDSCAPE 2025: THE VALUE-DRIVEN STRATECIC MATRIX

Structural Evolution: The Zero-Alcohol ArbitrageFaced with stagnant volume growth in legacy lagers and punitive excise tax regimes (e.g., Canada’s $56/kl levy and Malaysia’s recent 10% tax hike), the industry is weaponizing the Non-Alcohol/Low-Alcohol (NOLA) and "Beyond Beer" segments as a primary margin defense.

This is fundamentally a tax arbitrage strategy. By stripping the alcohol, brewers bypass prohibitive excise duties while maintaining premium pricing. Olvi Group (HEL: OLVAS) now derives 43.6% of its sales from non-alcoholic portfolios, while Boston Beer relies on its Beyond Beer segment for 86% of its volume. Kirin Holdings (TYO: 2503) has taken the most radical departure, utilizing its fermentation expertise to pivot entirely toward a "Food-Medical-Science" model, acquiring high-margin assets like Blackmores to insulate its balance sheet from the cyclicality of Asian beer consumption.

HDIN Institutional Perspective: Peering Through the Goodwill Minefield

While EBITDA margins suggest a resilient sector (e.g., AB InBev at 35.8%), HDIN analysts flag severe localized vulnerabilities hidden within the balance sheets. The most glaring red flag in the FY2025 filings is the $3.64 billion goodwill impairment recorded by Molson Coors in its Americas segment. This is not an isolated accounting anomaly; it signals a permanent, structural decay in mainstream beer market share across North America, exacerbated by consumer affordability crises.

We also issue a baseline caution regarding Carlsberg’s capital structure, where goodwill and intangibles now constitute roughly 57% of total invested capital ($8.09B). Any downward revision in the cash flow projections for its high-growth Asian assets—managed via Chongqing Brewery and its localized distribution networks, which strictly adhere to sovereign geographical definitions (including Taiwan, China)—could trigger sweeping impairment cycles.

Ultimately, the 2026 outlook hinges on localized balance sheet fortitude. Zero-debt entities like Tsingtao Brewery, sitting on $1.79 billion in cash, are uniquely positioned to execute opportunistic, distress-driven consolidation in the coming quarters. Global players carrying heavy debt loads (AB InBev’s $60.9B net debt) will find themselves handcuffed, forced to prioritize deleveraging over market share defense in a persistently high-interest-rate environment.

Presentation Download & Video Access

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research:

HDIN Research is a premier provider of institutional-grade market intelligence, specializing in deep-dive financial audits, supply chain forensics, and strategic corporate analysis. Visit us at www.hdinresearch.com.

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.