Nuburu Abandons Industrial Lasers for NATO Defense Platform Following Complete IP Foreclosure and $0 FY2025 Revenue

Date : 2026-04-08

Reading : 106

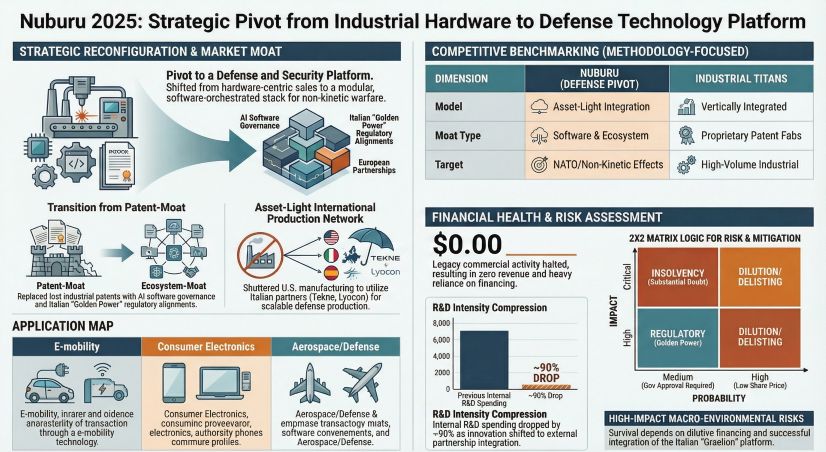

Nuburu’s FY2025 financial disclosures reveal a company stripped of its legacy operational foundation, sustained entirely by aggressive financial engineering. Total revenue flatlined at $0 (down from a negligible $152,127 in FY2024), effectively confirming the company’s absolute exit from the commercial industrial laser sector.

The immediate cessation of stateside operations obliterated historical R&D frameworks. FY2025 R&D spend plummeted to a mere $174,559—just 0.96% of total operating expenses—signaling a complete suspension of internal innovation. Instead of organic growth, management is betting its survival on a string of highly leveraged, purportedly accretive acquisitions including a $12.5 million buyout of Orbit S.r.l. and a $2 million acquisition of Lyocon S.r.l.

However, the balance sheet exposes a precarious liquidity cliff. While net financing cash flows surged to $58.13 million—largely driven by a heavily dilutive $100 million Standby Equity Purchase Agreement (SEPA) with YA II PN—operating cash burn remains severe at $16.09 million annually. The capitalization structure is highly toxic: a $25 million debenture demands rigid monthly principal payments of $2.78 million beginning in March 2026. Lacking organic cash flow and facing a $15.18 million stockholders' deficit, the firm’s survival relies entirely on continuous market issuance despite extreme dilution risks. Compounding these structural weaknesses, management’s failure to prevent a $1.01 million fraudulent wire transfer in October 2025 highlights critical internal control deficiencies that threaten institutional credibility.

Figure Nuburu 2025: Strategic Pivot from Industrial Hardware to Defense Technology Platform

Supply Chain Pivot: Retreating to the European Defense Shield

Supply Chain Pivot: Retreating to the European Defense Shield

Faced with severe margin compression and acute inventory de-stocking pressures across the legacy commercial EV battery welding sector, Nuburu systematically dismantled its domestic vertical integration. The company shuttered its Colorado facilities, rendering its U.S. inventory and equipment to zero book value, and outsourced future hardware assembly to international partners.

The supply chain architecture is now hyper-localized within NATO-aligned European territories. By acquiring a 70% controlling interest in Italian tactical vehicle manufacturer Tekne S.p.A. and deploying the Graelion platform via Ukraine’s Beryl LLC, Nuburu has effectively tethered its operational cadence to European defense procurement cycles. To mitigate the working capital traps of heavy manufacturing, Nuburu subscribed to €5.25 million in SYME 3 bonds, leveraging Supply@ME Capital’s platform to monetize Tekne’s inventory.

This network is highly contingent on sovereign regulatory clearance. The structural viability of this entire European supply chain pivot rests exclusively on the Italian Government’s "Golden Power" approval. Any regulatory friction here would instantly paralyze Nuburu's Transformation Plan.

HDIN Institutional Perspective: From Physics to Regulatory Capture

Nuburu’s FY2025 trajectory is less a story of technological iteration and more a textbook case of strategic crisis management. When secured lenders foreclosed on Nuburu's 220 patents, they essentially handed the high-power blue laser commercial market to vertically integrated titans like IPG Photonics and Coherent.

By transitioning to an "asset-light" holding company, Nuburu is attempting to replace a physical physics-based moat with a software and regulatory moat. Orbit S.r.l.’s AI orchestration software introduces a sticky, Software-as-a-Service (SaaS) command layer, while the Tekne integration taps directly into NATO procurement channels. If successful, this ecosystem creates high switching costs for defense clients, compensating for the lack of baseline patent protection.

However, the margin for error is non-existent. Nuburu currently operates without the robust cost-pass-through mechanisms typical of established defense primes. The firm must hit its Phase 1 Tekne cooperation target of $5.65 million to $11.31 million in 2026 revenue, or the YA II PN debt service schedule will force a catastrophic liquidity event. Nuburu is no longer an industrial laser company; it is a highly speculative, venture-style defense rollup operating on a razor-thin macroeconomic wire.

Presentation Download & Video Access

* Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

* Video Link: Click this link to watch the YouTube video.

About HDIN Research

HDIN Research is a premier strategic market intelligence firm specializing in institutional-grade financial analysis, supply chain forensics, and geopolitical risk assessment. By connecting the dots between raw regulatory filings and global macroeconomic shifts, HDIN delivers alpha-generating insights for hedge funds, private equity, and corporate strategy boards. Visit us at www.hdinresearch.com.

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.

The immediate cessation of stateside operations obliterated historical R&D frameworks. FY2025 R&D spend plummeted to a mere $174,559—just 0.96% of total operating expenses—signaling a complete suspension of internal innovation. Instead of organic growth, management is betting its survival on a string of highly leveraged, purportedly accretive acquisitions including a $12.5 million buyout of Orbit S.r.l. and a $2 million acquisition of Lyocon S.r.l.

However, the balance sheet exposes a precarious liquidity cliff. While net financing cash flows surged to $58.13 million—largely driven by a heavily dilutive $100 million Standby Equity Purchase Agreement (SEPA) with YA II PN—operating cash burn remains severe at $16.09 million annually. The capitalization structure is highly toxic: a $25 million debenture demands rigid monthly principal payments of $2.78 million beginning in March 2026. Lacking organic cash flow and facing a $15.18 million stockholders' deficit, the firm’s survival relies entirely on continuous market issuance despite extreme dilution risks. Compounding these structural weaknesses, management’s failure to prevent a $1.01 million fraudulent wire transfer in October 2025 highlights critical internal control deficiencies that threaten institutional credibility.

Figure Nuburu 2025: Strategic Pivot from Industrial Hardware to Defense Technology Platform

Supply Chain Pivot: Retreating to the European Defense ShieldFaced with severe margin compression and acute inventory de-stocking pressures across the legacy commercial EV battery welding sector, Nuburu systematically dismantled its domestic vertical integration. The company shuttered its Colorado facilities, rendering its U.S. inventory and equipment to zero book value, and outsourced future hardware assembly to international partners.

The supply chain architecture is now hyper-localized within NATO-aligned European territories. By acquiring a 70% controlling interest in Italian tactical vehicle manufacturer Tekne S.p.A. and deploying the Graelion platform via Ukraine’s Beryl LLC, Nuburu has effectively tethered its operational cadence to European defense procurement cycles. To mitigate the working capital traps of heavy manufacturing, Nuburu subscribed to €5.25 million in SYME 3 bonds, leveraging Supply@ME Capital’s platform to monetize Tekne’s inventory.

This network is highly contingent on sovereign regulatory clearance. The structural viability of this entire European supply chain pivot rests exclusively on the Italian Government’s "Golden Power" approval. Any regulatory friction here would instantly paralyze Nuburu's Transformation Plan.

HDIN Institutional Perspective: From Physics to Regulatory Capture

Nuburu’s FY2025 trajectory is less a story of technological iteration and more a textbook case of strategic crisis management. When secured lenders foreclosed on Nuburu's 220 patents, they essentially handed the high-power blue laser commercial market to vertically integrated titans like IPG Photonics and Coherent.

By transitioning to an "asset-light" holding company, Nuburu is attempting to replace a physical physics-based moat with a software and regulatory moat. Orbit S.r.l.’s AI orchestration software introduces a sticky, Software-as-a-Service (SaaS) command layer, while the Tekne integration taps directly into NATO procurement channels. If successful, this ecosystem creates high switching costs for defense clients, compensating for the lack of baseline patent protection.

However, the margin for error is non-existent. Nuburu currently operates without the robust cost-pass-through mechanisms typical of established defense primes. The firm must hit its Phase 1 Tekne cooperation target of $5.65 million to $11.31 million in 2026 revenue, or the YA II PN debt service schedule will force a catastrophic liquidity event. Nuburu is no longer an industrial laser company; it is a highly speculative, venture-style defense rollup operating on a razor-thin macroeconomic wire.

Presentation Download & Video Access

* Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

* Video Link: Click this link to watch the YouTube video.

About HDIN Research

HDIN Research is a premier strategic market intelligence firm specializing in institutional-grade financial analysis, supply chain forensics, and geopolitical risk assessment. By connecting the dots between raw regulatory filings and global macroeconomic shifts, HDIN delivers alpha-generating insights for hedge funds, private equity, and corporate strategy boards. Visit us at www.hdinresearch.com.

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.