Grid Aggregation Leader Nuvve Pivots to V2G Hardware as FY2025 Megawatts Under Management Stabilize at 28.3 MW

Date : 2026-04-08

Reading : 121

Who: Nuvve Holding Corp. (NASDAQ: NVVE).

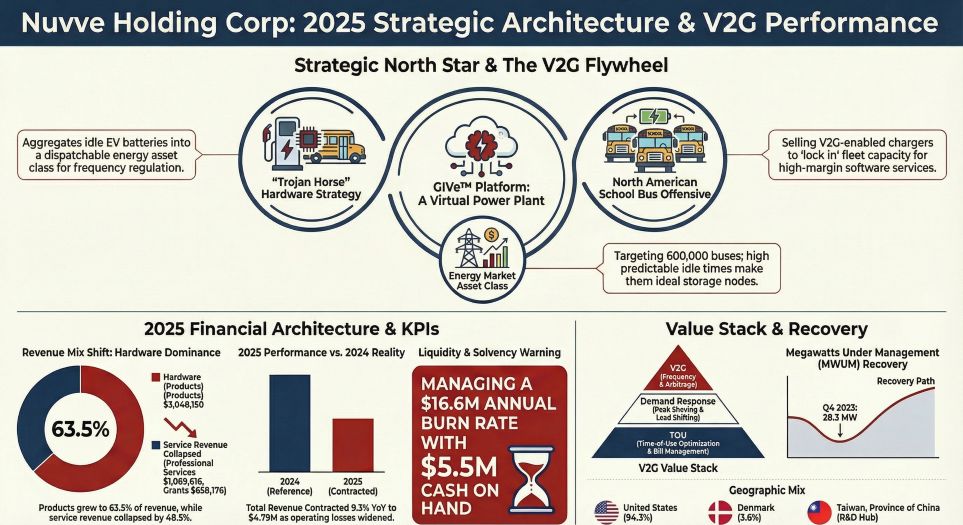

What: Reported a 9.3% YoY revenue contraction to $4.79 million in its FY2025 10-K audit, triggering a strategic pivot from engineering services toward hardware-led Virtual Power Plant (VPP) aggregation.

When: Fiscal Year 2025.

Where: Operations span its San Diego global headquarters, Denmark, and a newly established R&D hub in Taiwan, China.

Why: The abrupt termination of the Fresno EV infrastructure contract effectively collapsed service revenue by 48.5%, forcing management into a "survival-refinancing" loop to monetize its 28.3 Megawatts Under Management (MWUM).

Financial Health & Operational Moats: The Cost of IP Consolidation

Nuvve’s FY2025 P&L decomposition reveals a dual-speed operational matrix: a rapidly expanding hardware footprint overshadowed by severe structural liquidity friction. Total top-line metrics masked a critical internal shift—product revenue jumped 18.6% to $3.05 million (comprising 63.5% of total sales), driven primarily by elevated shipment volumes of bidirectional DC/AC chargers. Conversely, professional services crashed to $1.19 million, laying bare the company’s overexposure to localized municipal contracts following the collapse of the Fresno infrastructure project.

Despite an improvement in adjusted gross margins to 31.0%—a byproduct of shedding low-margin engineering overhead—operating losses widened by 57.3% to $32.18 million. The company is currently operating with an implied cash runway of just 3.9 months, possessing $5.79 million in liquidity against a $1.39 million monthly operational burn. Management has insulated its strategic moat through aggressive vertical integration, notably acquiring substantially all assets of Fermata Energy LLC. While this effectively creates a monopolistic position within the V2G patent landscape, Nuvve remains highly dependent on dilutive mezzanine equity (a $5.4 million Series A issuance) and the potential activation of a $25 million Equity Line of Credit (ELOC) to maintain Nasdaq compliance following a 1-for-40 reverse stock split.

Figure Nuvve Holding Corp: 2025 Strategic Architecture & V2G Performance

Supply Chain Pivot: Bypassing Domestic Friction via Asia-Pacific R&D

Supply Chain Pivot: Bypassing Domestic Friction via Asia-Pacific R&D

A forensic review of Nuvve’s $3.47 million inventory impairment exposes a highly calculated supply chain realignment rather than a standard write-down. The company absorbed structural hits on 125 kW V2G DC Chargers deemed non-conforming for the current U.S. commercial environment. Rather than liquidating, management engineered a forced inventory de-stocking strategy, transferring these units at zero carrying value to the Hsinchu metro area in Taiwan, China.

This pivot serves a dual purpose. First, it seeds a microgrid resilience joint venture with local partner e-Formula Technologies. Second, it hedges against the incoming U.S. administration's stated intent to reverse EV mandates and freeze federal charging infrastructure grants. With the looming threat of 10% global tariffs straining outsourced manufacturing agreements with hardware suppliers like Tellus Power Green, Nuvve lacks the leverage to execute cost-pass-through mechanisms. Shifting non-compliant domestic hardware into Asian R&D ecosystems allows the firm to incubate future geographic markets without straining 2026 domestic CAPEX.

HDIN Institutional Perspective: The "Call Option" on Grid Modernization

Nuvve represents a classic cyclical trough within the nascent grid-as-a-service (GaaS) sector. The market is fundamentally mispricing the company as a distressed hardware vendor rather than a software aggregator holding highly defensive IP. CEO Gregory Poilasne’s direct capital injections via SPV Promissory Notes signal absolute insider conviction that Nuvve’s proprietary GIVe™ AI platform is the "Logic Chip" for grid modernization.

The institutional thesis rests entirely on scaling the 28.3 MW capacity block. Management's strategic pivot targets the North American K-12 school bus market (a 600,000-unit TAM). By utilizing low-margin hardware as a "Trojan Horse" to capture predictable, high-capacity loads, Nuvve is laying the groundwork for highly accretive recurring revenues. We view the Danish fleet economics—generating $2,600 per vehicle annually in Frequency Containment Reserve (FCR) markets—as a proven unit economic baseline. However, execution is contingent on surviving the current liquidity bottleneck. Should Nuvve fail to refinance its $1.73 million near-term debt or unlock interconnection bottlenecks controlled by domestic utilities, its consolidated IP portfolio will likely become an acquisition target for legacy EVSE players lacking bidirectional sophistication.

Presentation Download & Video Access

* Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

* Video Link: Click this link to watch the YouTube video.

About HDIN Research

HDIN Research is a premier provider of institutional-grade market intelligence, specializing in deep-dive corporate filing analysis, supply chain forensics, and macroeconomic trend forecasting. We equip asset managers and strategic planners with the hard data necessary to navigate global capital markets.

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.

What: Reported a 9.3% YoY revenue contraction to $4.79 million in its FY2025 10-K audit, triggering a strategic pivot from engineering services toward hardware-led Virtual Power Plant (VPP) aggregation.

When: Fiscal Year 2025.

Where: Operations span its San Diego global headquarters, Denmark, and a newly established R&D hub in Taiwan, China.

Why: The abrupt termination of the Fresno EV infrastructure contract effectively collapsed service revenue by 48.5%, forcing management into a "survival-refinancing" loop to monetize its 28.3 Megawatts Under Management (MWUM).

Financial Health & Operational Moats: The Cost of IP Consolidation

Nuvve’s FY2025 P&L decomposition reveals a dual-speed operational matrix: a rapidly expanding hardware footprint overshadowed by severe structural liquidity friction. Total top-line metrics masked a critical internal shift—product revenue jumped 18.6% to $3.05 million (comprising 63.5% of total sales), driven primarily by elevated shipment volumes of bidirectional DC/AC chargers. Conversely, professional services crashed to $1.19 million, laying bare the company’s overexposure to localized municipal contracts following the collapse of the Fresno infrastructure project.

Despite an improvement in adjusted gross margins to 31.0%—a byproduct of shedding low-margin engineering overhead—operating losses widened by 57.3% to $32.18 million. The company is currently operating with an implied cash runway of just 3.9 months, possessing $5.79 million in liquidity against a $1.39 million monthly operational burn. Management has insulated its strategic moat through aggressive vertical integration, notably acquiring substantially all assets of Fermata Energy LLC. While this effectively creates a monopolistic position within the V2G patent landscape, Nuvve remains highly dependent on dilutive mezzanine equity (a $5.4 million Series A issuance) and the potential activation of a $25 million Equity Line of Credit (ELOC) to maintain Nasdaq compliance following a 1-for-40 reverse stock split.

Figure Nuvve Holding Corp: 2025 Strategic Architecture & V2G Performance

Supply Chain Pivot: Bypassing Domestic Friction via Asia-Pacific R&DA forensic review of Nuvve’s $3.47 million inventory impairment exposes a highly calculated supply chain realignment rather than a standard write-down. The company absorbed structural hits on 125 kW V2G DC Chargers deemed non-conforming for the current U.S. commercial environment. Rather than liquidating, management engineered a forced inventory de-stocking strategy, transferring these units at zero carrying value to the Hsinchu metro area in Taiwan, China.

This pivot serves a dual purpose. First, it seeds a microgrid resilience joint venture with local partner e-Formula Technologies. Second, it hedges against the incoming U.S. administration's stated intent to reverse EV mandates and freeze federal charging infrastructure grants. With the looming threat of 10% global tariffs straining outsourced manufacturing agreements with hardware suppliers like Tellus Power Green, Nuvve lacks the leverage to execute cost-pass-through mechanisms. Shifting non-compliant domestic hardware into Asian R&D ecosystems allows the firm to incubate future geographic markets without straining 2026 domestic CAPEX.

HDIN Institutional Perspective: The "Call Option" on Grid Modernization

Nuvve represents a classic cyclical trough within the nascent grid-as-a-service (GaaS) sector. The market is fundamentally mispricing the company as a distressed hardware vendor rather than a software aggregator holding highly defensive IP. CEO Gregory Poilasne’s direct capital injections via SPV Promissory Notes signal absolute insider conviction that Nuvve’s proprietary GIVe™ AI platform is the "Logic Chip" for grid modernization.

The institutional thesis rests entirely on scaling the 28.3 MW capacity block. Management's strategic pivot targets the North American K-12 school bus market (a 600,000-unit TAM). By utilizing low-margin hardware as a "Trojan Horse" to capture predictable, high-capacity loads, Nuvve is laying the groundwork for highly accretive recurring revenues. We view the Danish fleet economics—generating $2,600 per vehicle annually in Frequency Containment Reserve (FCR) markets—as a proven unit economic baseline. However, execution is contingent on surviving the current liquidity bottleneck. Should Nuvve fail to refinance its $1.73 million near-term debt or unlock interconnection bottlenecks controlled by domestic utilities, its consolidated IP portfolio will likely become an acquisition target for legacy EVSE players lacking bidirectional sophistication.

Presentation Download & Video Access

* Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

* Video Link: Click this link to watch the YouTube video.

About HDIN Research

HDIN Research is a premier provider of institutional-grade market intelligence, specializing in deep-dive corporate filing analysis, supply chain forensics, and macroeconomic trend forecasting. We equip asset managers and strategic planners with the hard data necessary to navigate global capital markets.

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.