Semiconductor Coating Leader UPAM Accelerates Sub-5nm Import Substitution as FY2025 Revenue Hits $68.97M

Date : 2026-04-09

Reading : 71

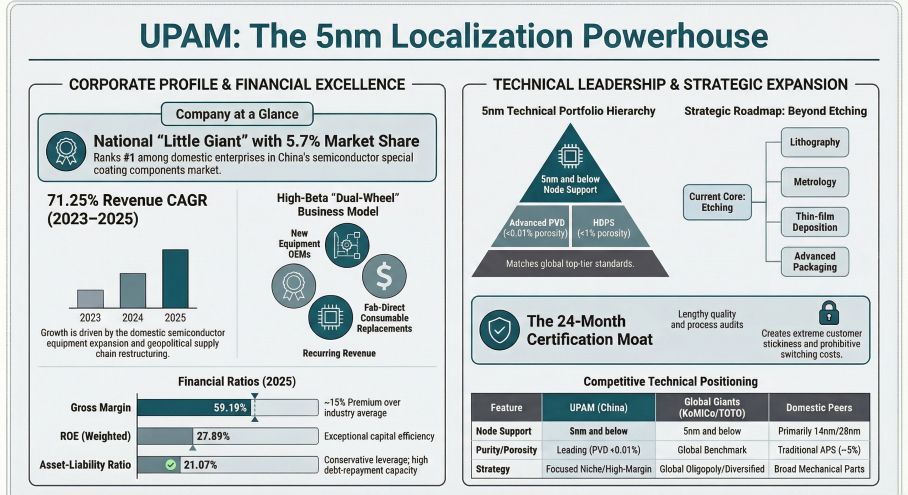

In its FY2025 prospectus audit, Chengdu Ultra Pure Applied Materials Co., Ltd. (UPAM) posted a 71.25% revenue CAGR, logging $68.97 million. Sited in mainland China, the manufacturer's revenue explosion is structurally driven by the geopolitical decoupling of global tech supply chains, forcing domestic foundries to localize sub-5nm etching equipment parts. As semiconductor special coatings now dictate 95.53% of its top line, UPAM is operating at 99.99% capacity utilization. This structural bottleneck mandates a $156.48 million IPO capital injection to scale physical vapor deposition (PVD) output and counter global incumbents like KoMiCo and TOCALO.

Financial Health & Operational Moats

UPAM operates with an unleveraged balance sheet, maintaining a 21.07% asset-liability ratio while self-funding hyper-growth. FY2025 operating cash flow (OCF) tracked impeccably with net profit, printing at $23.02 million and $25.70 million, respectively. The company circumvents standard industry margin compression through vertical integration and specialized intellectual property. By mastering High-Density Plasma Spraying (HDPS) and PVD technologies that achieve <0.01% porosity, UPAM secures a 59.19% gross margin—a sustainable 10-15% premium over traditional machining peers like Fortune Precision. This profitability is insulated by severe vendor lock-in; the 12-to-24-month certification cycle for advanced node equipment creates a prohibitive barrier to entry, effectively shielding UPAM from price wars and substitute threats.

Figure UPAM: The 5nm Localization Powerhouse

Supply Chain Pivot

Supply Chain Pivot

The firm’s client architecture exhibits extreme concentration, with its Top 5 accounts comprising 89.65% of FY2025 revenue. Specifically, domestic equipment giants Customer A ($26.74 million) and Customer B ($17.95 million) dictate the order book. Rather than a fatal vulnerability, this acts as a high-beta proxy for China’s semiconductor CapEx cycles. To hedge against sudden downstream inventory de-stocking or CapEx pullbacks, UPAM executes a "Dual-Drive" pivot. The company supplies OEMs directly for new capacity builds while aggressively targeting top-tier fabs (Customers E, F) to secure recurring consumable replacement revenues, systematically displacing foreign parts from AMAT and TEL. Upstream, UPAM relies on Kema Tech for base ceramics ($10.15 million in FY2025), necessitating strategic cost-pass-through mechanisms to absorb raw material volatility. The planned $24.74 million Meishan Base expansion will further diversify product lines into annealing and diffusion equipment parts.

HDIN Institutional Perspective

UPAM’s operational metrics indicate that the domestic semiconductor component sector is far from reaching its cyclical peak. With the mainland localization rate for semiconductor equipment components projected to reach merely 12.4% by 2029 against a $22.82 billion total addressable market, UPAM’s near-100% utilization rate signals a massive, unfulfilled import substitution trough. The company's 5.7% market share highlights a highly fragmented domestic base competing against entrenched foreign oligopolies. However, by substituting traditional anodic oxidation with 5nm-capable PVD, UPAM solves a critical fabrication chokepoint. Institutional investors must weigh the inherent key-account shock risks against the revenue explosive power generated by a captive domestic market. Ultimately, UPAM’s transition from a standard component supplier to an integrated materials engineering node exemplifies the ongoing structural shift necessary for China to achieve true autonomous controllability in logic chip manufacturing.

Presentation Download & Video Access

Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

Video Link: Click this link to watch the YouTube video.

About HDIN Research:

HDIN Research is a premier provider of institutional market intelligence, delivering razor-sharp financial analysis and geopolitical supply chain insights. Learn more at www.hdinresearch.com.

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.

Financial Health & Operational Moats

UPAM operates with an unleveraged balance sheet, maintaining a 21.07% asset-liability ratio while self-funding hyper-growth. FY2025 operating cash flow (OCF) tracked impeccably with net profit, printing at $23.02 million and $25.70 million, respectively. The company circumvents standard industry margin compression through vertical integration and specialized intellectual property. By mastering High-Density Plasma Spraying (HDPS) and PVD technologies that achieve <0.01% porosity, UPAM secures a 59.19% gross margin—a sustainable 10-15% premium over traditional machining peers like Fortune Precision. This profitability is insulated by severe vendor lock-in; the 12-to-24-month certification cycle for advanced node equipment creates a prohibitive barrier to entry, effectively shielding UPAM from price wars and substitute threats.

Figure UPAM: The 5nm Localization Powerhouse

Supply Chain PivotThe firm’s client architecture exhibits extreme concentration, with its Top 5 accounts comprising 89.65% of FY2025 revenue. Specifically, domestic equipment giants Customer A ($26.74 million) and Customer B ($17.95 million) dictate the order book. Rather than a fatal vulnerability, this acts as a high-beta proxy for China’s semiconductor CapEx cycles. To hedge against sudden downstream inventory de-stocking or CapEx pullbacks, UPAM executes a "Dual-Drive" pivot. The company supplies OEMs directly for new capacity builds while aggressively targeting top-tier fabs (Customers E, F) to secure recurring consumable replacement revenues, systematically displacing foreign parts from AMAT and TEL. Upstream, UPAM relies on Kema Tech for base ceramics ($10.15 million in FY2025), necessitating strategic cost-pass-through mechanisms to absorb raw material volatility. The planned $24.74 million Meishan Base expansion will further diversify product lines into annealing and diffusion equipment parts.

HDIN Institutional Perspective

UPAM’s operational metrics indicate that the domestic semiconductor component sector is far from reaching its cyclical peak. With the mainland localization rate for semiconductor equipment components projected to reach merely 12.4% by 2029 against a $22.82 billion total addressable market, UPAM’s near-100% utilization rate signals a massive, unfulfilled import substitution trough. The company's 5.7% market share highlights a highly fragmented domestic base competing against entrenched foreign oligopolies. However, by substituting traditional anodic oxidation with 5nm-capable PVD, UPAM solves a critical fabrication chokepoint. Institutional investors must weigh the inherent key-account shock risks against the revenue explosive power generated by a captive domestic market. Ultimately, UPAM’s transition from a standard component supplier to an integrated materials engineering node exemplifies the ongoing structural shift necessary for China to achieve true autonomous controllability in logic chip manufacturing.

Presentation Download & Video Access

Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

Video Link: Click this link to watch the YouTube video.

About HDIN Research:

HDIN Research is a premier provider of institutional market intelligence, delivering razor-sharp financial analysis and geopolitical supply chain insights. Learn more at www.hdinresearch.com.

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.