Zhaoxin Semiconductor Accelerates x86 Chiplet Pivot as FY2025 Revenue Surges 54% Amid Margin Compression

Date : 2026-04-09

Reading : 91

Shanghai Zhaoxin Semiconductor Co., Ltd. filed its FY2025 pre-IPO audit, reporting a 54.79% year-over-year revenue surge to $154.58 million, driven by mass shipments of its KX-7000 desktop processors. However, aggressive penetration pricing and yield-climbing costs resulted in severe margin compression, with gross margins plummeting to 10.55%. Headquartered in Shanghai with heavy distribution routing through Hong Kong, Zhaoxin is utilizing a $579.98 million IPO mandate to fund a strategic pivot toward localized advanced nodes and 96-core server architectures, directly challenging the global Intel/AMD x86 duopoly while insulating its supply chain from geopolitical shocks.

Financial Health & Operational Moats: The Pricing Power Deficit

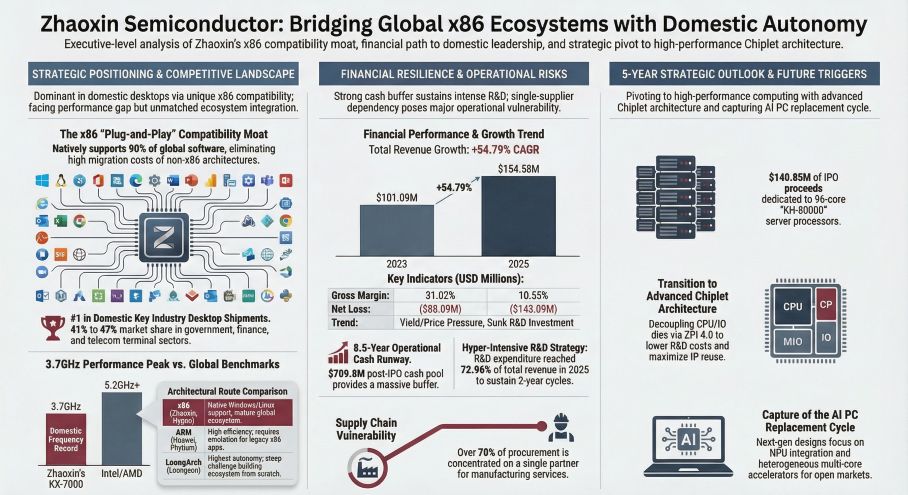

Zhaoxin’s FY2025 financials reveal a stark bifurcation between top-line market capture and bottom-line profitability. The company achieved a 23.65% 3-year CAGR, yet comprehensive gross margins cratered from 31.02% in 2023 to just 10.55% in 2025.

Lacking robust cost-pass-through mechanisms in a highly commoditized enterprise hardware sector, Zhaoxin absorbed the heavy fixed-cost amortization of its new KX-7000 and KH-50000 tape-outs. Rather than extracting premium margins, the company utilized price cuts on legacy KX-6000 stock to defend its 41% to 47% domestic key-industry desktop market share against ARM-based and LoongArch rivals.

Operating with a $112.79 million annual R&D burn rate (representing an intensive 72.96% of 2025 revenue), the firm is effectively subsidizing the domestic IT ecosystem’s transition. Despite net losses of $143.09 million in FY2025, near-term liquidity is heavily fortified. Bolstered by $361.74 million in state-backed credit facilities from China Construction Bank and Agricultural Bank of China, alongside the targeted $579.98 million IPO proceeds, Zhaoxin possesses an 8.5-year operational cash runway to execute its technological roadmap without imminent insolvency risks.

Figure Zhaoxin Semiconductor: Bridging Global x86 Ecosystems with Domestic Autonomy

Supply Chain Pivot: The "Company A" Concentration Risk

Supply Chain Pivot: The "Company A" Concentration Risk

Zhaoxin’s pure-play Fabless model explicitly eschews vertical integration, structurally binding its operational continuity to outsourced foundry capacities. The audit highlights a critical supply-side vulnerability: a 70.40% procurement dependency on a single upstream partner ("Company A"), totaling $122.01 million in 2025 for finished wafers, tape-out, and technical services.

Downstream, Zhaoxin’s revenue profile is overwhelmingly tethered to offshore distribution channels. In 2025, 97.34% of revenue was routed through distributors—led by Zhongdian International ($73.16 million) and Zanrun International. This Hong Kong-centric routing caters to the foreign exchange hedging and consolidated procurement demands of top-tier OEMs like Lenovo and Tsinghua Unisplendour. To mitigate the geopolitical risks of this highly concentrated structure, Zhaoxin is allocating $159.02 million of its IPO capital directly toward the "Advanced Process Processor R&D Project," signaling an accelerated pivot toward localized domestic foundries and EDA toolchains.

Product Matrix Evolution & The De-Stocking Cycle

The generational leap from SoC to Chiplet architecture marks Zhaoxin’s most critical inflection point. By decoupling the CPU Die from the I/O unit via its proprietary ZPI 4.0 interconnect, the company achieved domestic peak frequencies of 3.7GHz in the desktop KX-7000 series and scaled up to 96 cores in the server KH-50000 series.

However, the server segment exposes a pronounced cyclical vulnerability. As domestic data centers shifted capital expenditures toward AI compute, Zhaoxin faced significant resistance in legacy server markets. This forced aggressive inventory de-stocking for the older KH-40000 server processor, triggering massive inventory impairment losses that surged to $27.07 million in 2025. The company’s long-term enterprise viability now hinges entirely on the ecosystem adoption of the KH-50000 to capture mainstream cloud computing CAPEX against domestic rival Hygon Information.

HDIN Institutional Perspective: A Cyclical Bridge to the AI Open Market

Zhaoxin’s historical foundation relies on the $257 million intellectual property buyout from VIA Technologies in 2020—one of the most highly accretive acquisitions in the domestic semiconductor space, granting Zhaoxin a perpetual, frictionless moat in x86 software interoperability.

We view Zhaoxin's current margin floor not as a structural failure, but as a deliberate cyclical trough. The company is weaponizing its balance sheet to outlast the R&D amortization curve. The ultimate gauge for Zhaoxin’s institutional value in FY2026 will not be its legacy government procurement volumes, but its ability to commercialize the $280.10 million allocated for AI PC heterogeneous multi-core architectures (NPU integration). If Zhaoxin can leverage the impending AI hardware replacement super-cycle to break out of state-mandated silos and penetrate the commercial "open market," it will definitively transition from a policy-driven asset to a self-sustaining semiconductor heavyweight.

Presentation Download & Video Access

* Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

* Video Link: Click this link to watch the YouTube video.

About HDIN Research

HDIN Research is a premier strategic intelligence firm specializing in institutional-grade analysis of global supply chains, semiconductor cycles, and geopolitical market catalysts. (www.hdinresearch.com)

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*

Financial Health & Operational Moats: The Pricing Power Deficit

Zhaoxin’s FY2025 financials reveal a stark bifurcation between top-line market capture and bottom-line profitability. The company achieved a 23.65% 3-year CAGR, yet comprehensive gross margins cratered from 31.02% in 2023 to just 10.55% in 2025.

Lacking robust cost-pass-through mechanisms in a highly commoditized enterprise hardware sector, Zhaoxin absorbed the heavy fixed-cost amortization of its new KX-7000 and KH-50000 tape-outs. Rather than extracting premium margins, the company utilized price cuts on legacy KX-6000 stock to defend its 41% to 47% domestic key-industry desktop market share against ARM-based and LoongArch rivals.

Operating with a $112.79 million annual R&D burn rate (representing an intensive 72.96% of 2025 revenue), the firm is effectively subsidizing the domestic IT ecosystem’s transition. Despite net losses of $143.09 million in FY2025, near-term liquidity is heavily fortified. Bolstered by $361.74 million in state-backed credit facilities from China Construction Bank and Agricultural Bank of China, alongside the targeted $579.98 million IPO proceeds, Zhaoxin possesses an 8.5-year operational cash runway to execute its technological roadmap without imminent insolvency risks.

Figure Zhaoxin Semiconductor: Bridging Global x86 Ecosystems with Domestic Autonomy

Supply Chain Pivot: The "Company A" Concentration RiskZhaoxin’s pure-play Fabless model explicitly eschews vertical integration, structurally binding its operational continuity to outsourced foundry capacities. The audit highlights a critical supply-side vulnerability: a 70.40% procurement dependency on a single upstream partner ("Company A"), totaling $122.01 million in 2025 for finished wafers, tape-out, and technical services.

Downstream, Zhaoxin’s revenue profile is overwhelmingly tethered to offshore distribution channels. In 2025, 97.34% of revenue was routed through distributors—led by Zhongdian International ($73.16 million) and Zanrun International. This Hong Kong-centric routing caters to the foreign exchange hedging and consolidated procurement demands of top-tier OEMs like Lenovo and Tsinghua Unisplendour. To mitigate the geopolitical risks of this highly concentrated structure, Zhaoxin is allocating $159.02 million of its IPO capital directly toward the "Advanced Process Processor R&D Project," signaling an accelerated pivot toward localized domestic foundries and EDA toolchains.

Product Matrix Evolution & The De-Stocking Cycle

The generational leap from SoC to Chiplet architecture marks Zhaoxin’s most critical inflection point. By decoupling the CPU Die from the I/O unit via its proprietary ZPI 4.0 interconnect, the company achieved domestic peak frequencies of 3.7GHz in the desktop KX-7000 series and scaled up to 96 cores in the server KH-50000 series.

However, the server segment exposes a pronounced cyclical vulnerability. As domestic data centers shifted capital expenditures toward AI compute, Zhaoxin faced significant resistance in legacy server markets. This forced aggressive inventory de-stocking for the older KH-40000 server processor, triggering massive inventory impairment losses that surged to $27.07 million in 2025. The company’s long-term enterprise viability now hinges entirely on the ecosystem adoption of the KH-50000 to capture mainstream cloud computing CAPEX against domestic rival Hygon Information.

HDIN Institutional Perspective: A Cyclical Bridge to the AI Open Market

Zhaoxin’s historical foundation relies on the $257 million intellectual property buyout from VIA Technologies in 2020—one of the most highly accretive acquisitions in the domestic semiconductor space, granting Zhaoxin a perpetual, frictionless moat in x86 software interoperability.

We view Zhaoxin's current margin floor not as a structural failure, but as a deliberate cyclical trough. The company is weaponizing its balance sheet to outlast the R&D amortization curve. The ultimate gauge for Zhaoxin’s institutional value in FY2026 will not be its legacy government procurement volumes, but its ability to commercialize the $280.10 million allocated for AI PC heterogeneous multi-core architectures (NPU integration). If Zhaoxin can leverage the impending AI hardware replacement super-cycle to break out of state-mandated silos and penetrate the commercial "open market," it will definitively transition from a policy-driven asset to a self-sustaining semiconductor heavyweight.

Presentation Download & Video Access

* Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

* Video Link: Click this link to watch the YouTube video.

About HDIN Research

HDIN Research is a premier strategic intelligence firm specializing in institutional-grade analysis of global supply chains, semiconductor cycles, and geopolitical market catalysts. (www.hdinresearch.com)

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*