Success Bio-Tech Accelerates Class III Biomaterials Pipeline via $88M STAR Market IPO Amid VBP Margin Compression

Date : 2026-04-09

Reading : 96

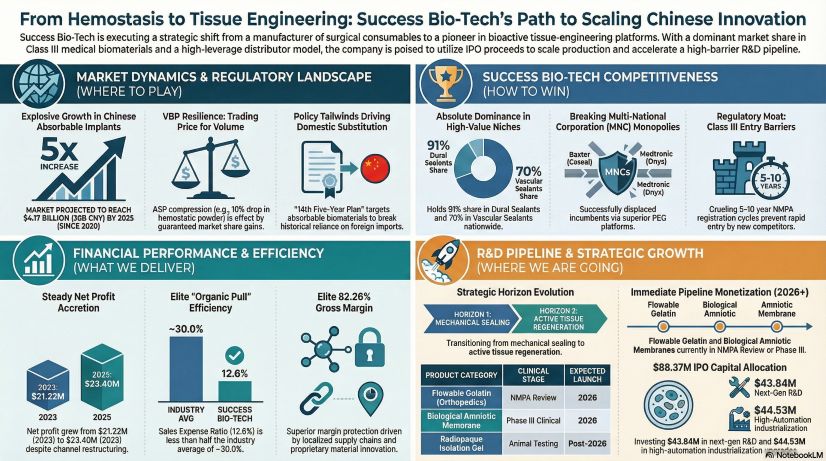

Success Bio-Tech Co., Ltd. is leveraging its upcoming $88.37 million STAR Market IPO to fund targeted capacity expansion at its Jinan facilities and accelerate Class III medical device commercialization through FY2026. Facing aggressive Volume-Based Procurement (VBP) pricing headwinds in China, the company executed a radical channel pivot in 2025, outsourcing terminal market access to a tightly managed ex-employee distributor network. This restructuring structurally suppressed internal sales expenses to 12.60%, allowing the company to defend an elite 82.26% gross margin, secure a 91% market share in dural sealants, and deliver $23.40 million in net profit.

Financial Health & Operational Moats

The Margin-Expense Trade-Off and Channel Leverage

Success Bio-Tech’s FY2025 prospectus reveals a high-leverage commercial architecture engineered to absorb VBP-induced price cuts while maintaining robust profitability. While top-line revenue optically stabilized at $47.06 million, net profit expanded to $23.40 million. This divergence is driven by a calculated divestment from direct sales; the company routed 90.82% of its core revenue through distributors, drastically minimizing internal operational drag.

Crucially, 54.68% of total 2025 revenue was generated by distributors controlled by ex-employees. While this introduces a structural dependency risk, it functions as a highly efficient "organic pull" commercial engine. By outsourcing academic promotion, the company generates an exceptional $0.96 million in revenue per internal sales employee and limits pure business promotion fees to a mere 7.96% of revenue—less than half the industry average of peers like Haohai Biological.

Figure From Hemostasis to Tissue Engineering: Success Bio-Tech's Path to Scaling Chinese innovation

Zero Capitalized R&D Overhang

Zero Capitalized R&D Overhang

The company's earnings quality remains pristine. Despite maintaining an R&D expense ratio of 9.95% ($4.68 million) in 2025, Success Bio-Tech strictly expenses 100% of its development costs. The balance sheet carries zero capitalized R&D overhang, completely insulating the firm from future impairment shocks often seen in the biotech sector. This capital discipline supports a deep Horizon 3 pipeline, including the NMPA-reviewed Absorbable Hemostatic Flowable Gelatin and a Glioma Intraoperative Drug-Loaded Gel.

Supply Chain Pivot: Vertical Integration and Capacity Realignment

Feedstock Cost Engineering

To counter the "exchange price for volume" dynamics dictated by VBP, Success Bio-Tech has aggressively optimized its raw material procurement. By diversifying its supplier base for critical PEG derivatives, the firm drove unit costs down from $33.43/g in 2023 to $15.29/g in 2025. This 54% reduction in primary feedstock costs provides a critical cost-pass-through buffer, directly subsidizing the ASP compression seen in its hemostatic powder (Shunshi) and anti-adhesion liquid (Saibituo) segments.

CAPEX Injection and Short-Term Asset Dilution

The STAR Market proceeds are earmarked for an immediate fixed-asset scale-up. The company is directing $27.83 million into the Medical Device Industrialization Upgrade Project and another $16.70 million into upgrading cleanrooms and automating production at its Jinan High-tech Zone and Licheng District bases. While this capacity injection is necessary to absorb the volume surges mandated by provincial bidding alliances, it introduces a short-term asset turnover dilution. The addition of approximately $44.5 million in new fixed assets will inflate the denominator of the turnover ratio, meaning long-term ROE recovery relies entirely on the rapid market penetration of its Horizon 2 Biological Amniotic Membrane and orthopedic bone wax pipelines.

HDIN Institutional Perspective

The strategic maneuvering of Success Bio-Tech signals a broader macro shift in China's high-value medical consumables sector. The company's heavy reliance on ex-employee provincial distributors is not merely a cost-saving measure; it is a sophisticated regulatory firewall. As China enforces the "Two-Invoice System" and tightens compliance audits on grassroots academic promotion, Success Bio-Tech effectively isolates itself from regional compliance shocks by pushing bidding coordination and localized hospital relations onto independent, yet fiercely loyal, third-party entities.

Furthermore, Success Bio-Tech's success in displacing legacy multinational monopolies—forcing Medtronic's Onyx liquid embolic agent ASP down to $835 and breaking Baxter's Coseal vascular sealant grip—proves that domestic substitution has moved beyond low-end consumables. The company’s pivot toward active targeted delivery and smart, environment-responsive biomaterials (Horizon 3) indicates that the next phase of competition will not be won on mechanical sealing efficacy, but on cellular-level tissue engineering. If Success Bio-Tech can commercialize its Radiopaque Isolation Gel for prostate radiotherapy against solitary imported alternatives, it will validate its transition from a niche sealant manufacturer into a global platform-based biomaterials player.

Presentation Download & Video Access

Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

Video Link: Click this link to watch the YouTube video.

About HDIN Research:

HDIN Research is a premier strategic advisory and market intelligence firm, specializing in deep-dive equity analysis, supply chain forensics, and geopolitical risk assessments for institutional investors. (www.hdinresearch.com)

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.

Financial Health & Operational Moats

The Margin-Expense Trade-Off and Channel Leverage

Success Bio-Tech’s FY2025 prospectus reveals a high-leverage commercial architecture engineered to absorb VBP-induced price cuts while maintaining robust profitability. While top-line revenue optically stabilized at $47.06 million, net profit expanded to $23.40 million. This divergence is driven by a calculated divestment from direct sales; the company routed 90.82% of its core revenue through distributors, drastically minimizing internal operational drag.

Crucially, 54.68% of total 2025 revenue was generated by distributors controlled by ex-employees. While this introduces a structural dependency risk, it functions as a highly efficient "organic pull" commercial engine. By outsourcing academic promotion, the company generates an exceptional $0.96 million in revenue per internal sales employee and limits pure business promotion fees to a mere 7.96% of revenue—less than half the industry average of peers like Haohai Biological.

Figure From Hemostasis to Tissue Engineering: Success Bio-Tech's Path to Scaling Chinese innovation

Zero Capitalized R&D OverhangThe company's earnings quality remains pristine. Despite maintaining an R&D expense ratio of 9.95% ($4.68 million) in 2025, Success Bio-Tech strictly expenses 100% of its development costs. The balance sheet carries zero capitalized R&D overhang, completely insulating the firm from future impairment shocks often seen in the biotech sector. This capital discipline supports a deep Horizon 3 pipeline, including the NMPA-reviewed Absorbable Hemostatic Flowable Gelatin and a Glioma Intraoperative Drug-Loaded Gel.

Supply Chain Pivot: Vertical Integration and Capacity Realignment

Feedstock Cost Engineering

To counter the "exchange price for volume" dynamics dictated by VBP, Success Bio-Tech has aggressively optimized its raw material procurement. By diversifying its supplier base for critical PEG derivatives, the firm drove unit costs down from $33.43/g in 2023 to $15.29/g in 2025. This 54% reduction in primary feedstock costs provides a critical cost-pass-through buffer, directly subsidizing the ASP compression seen in its hemostatic powder (Shunshi) and anti-adhesion liquid (Saibituo) segments.

CAPEX Injection and Short-Term Asset Dilution

The STAR Market proceeds are earmarked for an immediate fixed-asset scale-up. The company is directing $27.83 million into the Medical Device Industrialization Upgrade Project and another $16.70 million into upgrading cleanrooms and automating production at its Jinan High-tech Zone and Licheng District bases. While this capacity injection is necessary to absorb the volume surges mandated by provincial bidding alliances, it introduces a short-term asset turnover dilution. The addition of approximately $44.5 million in new fixed assets will inflate the denominator of the turnover ratio, meaning long-term ROE recovery relies entirely on the rapid market penetration of its Horizon 2 Biological Amniotic Membrane and orthopedic bone wax pipelines.

HDIN Institutional Perspective

The strategic maneuvering of Success Bio-Tech signals a broader macro shift in China's high-value medical consumables sector. The company's heavy reliance on ex-employee provincial distributors is not merely a cost-saving measure; it is a sophisticated regulatory firewall. As China enforces the "Two-Invoice System" and tightens compliance audits on grassroots academic promotion, Success Bio-Tech effectively isolates itself from regional compliance shocks by pushing bidding coordination and localized hospital relations onto independent, yet fiercely loyal, third-party entities.

Furthermore, Success Bio-Tech's success in displacing legacy multinational monopolies—forcing Medtronic's Onyx liquid embolic agent ASP down to $835 and breaking Baxter's Coseal vascular sealant grip—proves that domestic substitution has moved beyond low-end consumables. The company’s pivot toward active targeted delivery and smart, environment-responsive biomaterials (Horizon 3) indicates that the next phase of competition will not be won on mechanical sealing efficacy, but on cellular-level tissue engineering. If Success Bio-Tech can commercialize its Radiopaque Isolation Gel for prostate radiotherapy against solitary imported alternatives, it will validate its transition from a niche sealant manufacturer into a global platform-based biomaterials player.

Presentation Download & Video Access

Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

Video Link: Click this link to watch the YouTube video.

About HDIN Research:

HDIN Research is a premier strategic advisory and market intelligence firm, specializing in deep-dive equity analysis, supply chain forensics, and geopolitical risk assessments for institutional investors. (www.hdinresearch.com)

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.