Global Protein Processors See Diverging Margins: Vertically Integrated Giants Defend Yields as Kraft Heinz Absorbs $9.3B Impairment

Date : 2026-04-09

Reading : 206

In the FY2025 audit cycle, global packaged food and protein giants (including NASDAQ: KHC, NYSE: TSN, NYSE: HRL, and JBS N.V.) are exhibiting severe operational bifurcation. Driven by persistent inflation, acute labor shortages, and shifting consumer elasticity across the U.S. and Europe, highly processed CPG portfolios are suffering severe brand value erosion. Conversely, vertically integrated meatpackers are leveraging precise cost-pass-through mechanisms and aggressively redirecting capital from raw capacity expansion toward plant automation and cross-border supply chain arbitrage.

Financial Health & Operational Moats: The Disconnect Between Brand Equity and Margin Realization

The 2025 fiscal data exposes a critical fracture between legacy brand perception and actual margin capture, punishing M&A-heavy portfolios while rewarding cash-generative operational moats.

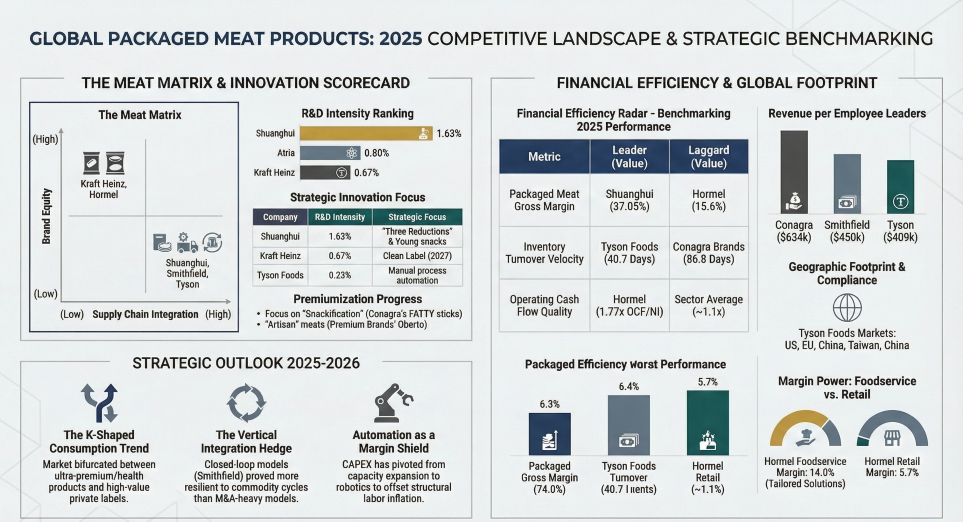

The Goodwill Reckoning: Kraft Heinz (NASDAQ: KHC) recorded a catastrophic $9.3 billion non-cash impairment loss targeting its core legacy brands, including Oscar Mayer and Lunchables. This write-down exposes a fundamental "marketing trap": despite increasing advertising expenditures to $1.07 billion in 2025, KHC’s organic net sales contracted by 3.4%, driven by a sharp 4.1% drop in volume/mix. Across the aisle, Conagra Brands (NYSE: CAG) carries $10.5 billion in goodwill against just $8.9 billion in total shareholders' equity (a 117% ratio), presenting an extreme latent risk profile as retail channels endure prolonged inventory de-stocking and intense private-label substitution.

Cash Conversion & Leverage Vulnerabilities: Quality of earnings has emerged as the definitive 2026 survival metric. Hormel Foods (NYSE: HRL) demonstrated elite cash flow conversion, generating an Operating Cash Flow to Net Income (OCF/NI) ratio of 1.77x ($845 million OCF vs. $478.2 million NI). Despite experiencing margin compression in its retail segment due to volatile raw material costs, Hormel offset this by exploiting a highly lucrative Foodservice channel, which captured a 14.0% margin compared to Retail's 5.7%.

Conversely, leverage profiles present an existential threat to heavily indebted processors. Tyson Foods (NYSE: TSN) and JBS N.V. are operating with critically low Interest Coverage Ratios (ICR) of 2.44x and ~2.9x, respectively. In stark contrast, Smithfield Foods operates a fortress balance sheet with an ICR of 31.5x and a net debt-to-adjusted EBITDA ratio of just 0.3x, insulating the vertically integrated producer from sustained high borrowing costs.

Figure GLOBAL PACKAGED MEAT PRODUCTS: 2025 COMPETITIVE LANDSCAPE & STRATEGIC BENCHMARKING

Supply Chain Pivot: Cross-Border Arbitrage and the Automation CAPEX Cycle

Supply Chain Pivot: Cross-Border Arbitrage and the Automation CAPEX Cycle

The era of scaling raw commodity slaughter volume is definitively over. The collective 2025 capital expenditure footprint reveals a structural pivot toward robotics, facility automation, and geographical supply chain hedging.

CAPEX Reallocation & Automation: To offset structural labor inflation, major players are aggressively replacing human capital with automated yield-capture technologies. Smithfield directed a substantial portion of its $341 million segment CAPEX toward plant automation, redeploying labor to higher-value lines. Similarly, Shuanghui injected roughly $180 million (CNY 1.3 billion) into intelligent digital upgrades. Physical capacity expansion is now strictly reserved for high-margin prepared foods, evidenced by JBS funding a $100 million ready-to-eat bacon and sausage plant in Iowa, and Smithfield acquiring a $38 million dry sausage facility in Nashville, Tennessee.

Geopolitical Asymmetry & Cross-Border Balancing: With US-China pork tariffs peaking at 47% and the EU Deforestation Regulation (EUDR) imposing strict traceability mandates, single-origin export models are obsolete. JBS is executing sophisticated cross-border arbitrage, leveraging its Australian footprint (FMD-free, 8.3% of total revenue) to bypass Asian import hurdles, while simultaneously deploying a $150 million greenfield plant in Oman to localize production for the Middle East. Smithfield strategically hedged its U.S. tariff exposure by utilizing recent European acquisitions (Argal in Spain and DeVeris in Poland) to funnel non-U.S. origin pork into the Asian market. Meanwhile, Hormel successfully insulated its Chinese growth through localized "in-country production" at its Jiaxing facility.

HDIN Institutional Perspective: The "Plant-Based" Bubble Burst and the Vertical Moat

The 2025 data mathematically confirms the failure of the "concept-driven" premiumization thesis. The plant-based meat sector is currently a margin-destroying liability, punctuated by Conagra's $91.5 million impairment of its Gardein brand. Real consumer demand has pivoted toward "physical premiumization"—evidenced by Premium Brands executing accretive acquisitions in the artisan and dry-cured charcuterie space (e.g., Italia Salami Company) and Shuanghui’s successful "Snackification" of its product matrix through its *Hui Xiao Pu* sub-brand.

Furthermore, the industry’s heavy reliance on mega-retailers—with Walmart accounting for 29% of Conagra’s sales and 21% of Kraft Heinz’s—has stripped CPG giants of unilateral pricing power. We assess that true alpha in 2026 relies on strict vertical integration. Companies controlling the end-to-end supply chain (feed-to-shelf) possess the intrinsic flexibility to bypass retail slotting wars. The winning formula moving forward requires decoupling from mainstream supermarket distribution, either by targeting independent retailers via proprietary logistics fleets or locking in high-margin, tailored foodservice contracts that automate back-of-house operations for major restaurant chains.

Presentation Download & Video Access

Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

Video Link: Click this link to watch the YouTube video.

About HDIN Research:

HDIN Research provides institutional-grade market intelligence, supply chain forensics, and competitive benchmarking for the global equity and private markets. Visit www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*

Financial Health & Operational Moats: The Disconnect Between Brand Equity and Margin Realization

The 2025 fiscal data exposes a critical fracture between legacy brand perception and actual margin capture, punishing M&A-heavy portfolios while rewarding cash-generative operational moats.

The Goodwill Reckoning: Kraft Heinz (NASDAQ: KHC) recorded a catastrophic $9.3 billion non-cash impairment loss targeting its core legacy brands, including Oscar Mayer and Lunchables. This write-down exposes a fundamental "marketing trap": despite increasing advertising expenditures to $1.07 billion in 2025, KHC’s organic net sales contracted by 3.4%, driven by a sharp 4.1% drop in volume/mix. Across the aisle, Conagra Brands (NYSE: CAG) carries $10.5 billion in goodwill against just $8.9 billion in total shareholders' equity (a 117% ratio), presenting an extreme latent risk profile as retail channels endure prolonged inventory de-stocking and intense private-label substitution.

Cash Conversion & Leverage Vulnerabilities: Quality of earnings has emerged as the definitive 2026 survival metric. Hormel Foods (NYSE: HRL) demonstrated elite cash flow conversion, generating an Operating Cash Flow to Net Income (OCF/NI) ratio of 1.77x ($845 million OCF vs. $478.2 million NI). Despite experiencing margin compression in its retail segment due to volatile raw material costs, Hormel offset this by exploiting a highly lucrative Foodservice channel, which captured a 14.0% margin compared to Retail's 5.7%.

Conversely, leverage profiles present an existential threat to heavily indebted processors. Tyson Foods (NYSE: TSN) and JBS N.V. are operating with critically low Interest Coverage Ratios (ICR) of 2.44x and ~2.9x, respectively. In stark contrast, Smithfield Foods operates a fortress balance sheet with an ICR of 31.5x and a net debt-to-adjusted EBITDA ratio of just 0.3x, insulating the vertically integrated producer from sustained high borrowing costs.

Figure GLOBAL PACKAGED MEAT PRODUCTS: 2025 COMPETITIVE LANDSCAPE & STRATEGIC BENCHMARKING

Supply Chain Pivot: Cross-Border Arbitrage and the Automation CAPEX CycleThe era of scaling raw commodity slaughter volume is definitively over. The collective 2025 capital expenditure footprint reveals a structural pivot toward robotics, facility automation, and geographical supply chain hedging.

CAPEX Reallocation & Automation: To offset structural labor inflation, major players are aggressively replacing human capital with automated yield-capture technologies. Smithfield directed a substantial portion of its $341 million segment CAPEX toward plant automation, redeploying labor to higher-value lines. Similarly, Shuanghui injected roughly $180 million (CNY 1.3 billion) into intelligent digital upgrades. Physical capacity expansion is now strictly reserved for high-margin prepared foods, evidenced by JBS funding a $100 million ready-to-eat bacon and sausage plant in Iowa, and Smithfield acquiring a $38 million dry sausage facility in Nashville, Tennessee.

Geopolitical Asymmetry & Cross-Border Balancing: With US-China pork tariffs peaking at 47% and the EU Deforestation Regulation (EUDR) imposing strict traceability mandates, single-origin export models are obsolete. JBS is executing sophisticated cross-border arbitrage, leveraging its Australian footprint (FMD-free, 8.3% of total revenue) to bypass Asian import hurdles, while simultaneously deploying a $150 million greenfield plant in Oman to localize production for the Middle East. Smithfield strategically hedged its U.S. tariff exposure by utilizing recent European acquisitions (Argal in Spain and DeVeris in Poland) to funnel non-U.S. origin pork into the Asian market. Meanwhile, Hormel successfully insulated its Chinese growth through localized "in-country production" at its Jiaxing facility.

HDIN Institutional Perspective: The "Plant-Based" Bubble Burst and the Vertical Moat

The 2025 data mathematically confirms the failure of the "concept-driven" premiumization thesis. The plant-based meat sector is currently a margin-destroying liability, punctuated by Conagra's $91.5 million impairment of its Gardein brand. Real consumer demand has pivoted toward "physical premiumization"—evidenced by Premium Brands executing accretive acquisitions in the artisan and dry-cured charcuterie space (e.g., Italia Salami Company) and Shuanghui’s successful "Snackification" of its product matrix through its *Hui Xiao Pu* sub-brand.

Furthermore, the industry’s heavy reliance on mega-retailers—with Walmart accounting for 29% of Conagra’s sales and 21% of Kraft Heinz’s—has stripped CPG giants of unilateral pricing power. We assess that true alpha in 2026 relies on strict vertical integration. Companies controlling the end-to-end supply chain (feed-to-shelf) possess the intrinsic flexibility to bypass retail slotting wars. The winning formula moving forward requires decoupling from mainstream supermarket distribution, either by targeting independent retailers via proprietary logistics fleets or locking in high-margin, tailored foodservice contracts that automate back-of-house operations for major restaurant chains.

Presentation Download & Video Access

Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

Video Link: Click this link to watch the YouTube video.

About HDIN Research:

HDIN Research provides institutional-grade market intelligence, supply chain forensics, and competitive benchmarking for the global equity and private markets. Visit www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*