Global Protein Titans Pivot to Deep Processing and Automation as Top 10 Players Battle Severe Fresh Meat Margin Compression

Date : 2026-04-09

Reading : 264

In FY2025, global meat industry leaders—including Tyson Foods (NYSE: TSN), JBS N.V. (BVMF: JBSS3), and Muyuan Foods (SZSE: 002714)—are aggressively reallocating CAPEX away from pure capacity expansion toward AI-driven automation and value-added processing. Driven by extreme margin compression in raw commodities, such as Tyson’s -5.2% beef operating margin, these protein titans are restructuring global supply chains to mitigate localized feed volatility and tariff barriers. This structural pivot signals a definitive end to volume-driven dominance, forcing companies to secure profitability through downstream branded premiums and hyper-localized operational moats.

Financial Health & Operational Moats: Escaping the Commodity Margin Trap

The FY2025 financial disclosures reveal a brutal divergence in Return on Invested Capital (ROIC) between asset-light "spread operators" and deeply vertically integrated players. The fresh meat sector is universally suffering from a rigid "cost ceiling," forcing a mass migration toward downstream FMCG (Fast-Moving Consumer Goods) product portfolios to activate cost-pass-through mechanisms.

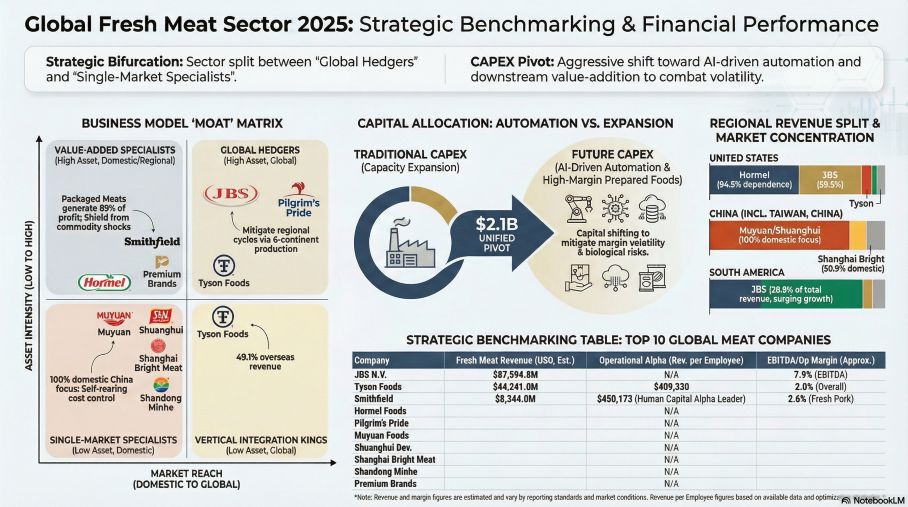

Smithfield Foods serves as the blueprint for this transition. While its Fresh Pork operations recorded a razor-thin 2.6% operating margin, its Packaged Meats segment generated $8.76 billion—contributing a massive 85% of the company's overall operating profit. This structural moat completely insulates the firm from live hog volatility. Similarly, Hormel Foods (NYSE: HRL) sustained a resilient 15.6% corporate gross margin by leveraging high-premium consumer branding (SPAM®, Applegate®) rather than fighting in the commodity trenches.

Conversely, companies heavily exposed to biological asset holding periods and commodity cycles are exhibiting acute balance sheet stress. Muyuan Foods achieved a highly lucrative 20.57% ROE through strict vertical integration (driving total rearing costs down to $1.67/kg), yet it masks a severe liquidity mismatch: holding $1.92 billion in cash against a staggering $5.72 billion in short-term debt. Furthermore, HDIN analysts flag severe "high cash, high debt" anomalies at Shanghai Bright Meat (SHSE: 600073), which held $503.3 million in cash but incurred $20.6 million in interest expenses on $515.6 million in short-term borrowings—a classic indicator of inefficient capital allocation or restricted liquidity.

Figure Clobal Fresh Meat Sector 2025: Strategic Benchmarking & Financial Performance

Supply Chain Pivot: Localized Hedging and Geopolitical Arbitrage

Supply Chain Pivot: Localized Hedging and Geopolitical Arbitrage

Global trade barriers are rendering the traditional export-heavy supply chain obsolete. Geopolitical friction, specifically China's 25% to 47% tariffs on U.S. pork offal, systematically dismantled the export margins of American producers in FY2025.

To hedge against this compliance friction, multinational giants are executing localized CAPEX strategies. JBS N.V. has insulated itself by deriving 74% of its net revenue from domestic sales within its operational footprints. The Brazilian titan is expanding its geographic arbitrage by deploying a $150 million multiprotein platform in Oman and an $85 million Seara plant in Saudi Arabia to capture the untariffed halal market.

Similarly, Shanghai Bright Meat executed a masterclass in supply chain hedging. Anticipating China’s impending three-year beef safeguard measure (which restricts imports from Brazil and the U.S. starting in 2026), Bright Meat leveraged its accretive acquisition of New Zealand’s Silver Fern Farms. This allowed the company to generate 49.1% of its revenue ($1.51 billion) overseas, securing premium beef sourcing that bypasses the targeted trade tariffs and creates a distinct pricing advantage over domestic competitors.

HDIN Institutional Perspective: CAPEX Reallocation Signals a Cyclical Trough

The global protein sector is actively navigating a late-stage cyclical trough, characterized by record-high cattle procurement costs in the Americas and an agonizingly slow inventory de-stocking phase in the Chinese pork market.

To breach the operational performance ceiling, industry leaders are abandoning volume growth. Tyson Foods has earmarked $0.7 billion to $1.0 billion in FY2026 CAPEX explicitly for automation and global network optimization—which includes shuttering inefficient legacy plants. Shuanghui Development (SZSE: 000895) is deploying $180.9 million into ERP overhauls and AI visual recognition for precise meat grading.

Ultimately, the FY2025 filings confirm that the moat in the protein sector is no longer scale; it is biosecurity, deep-processing capacity, and technological efficiency. Companies that rely strictly on wholesale commodity slaughtering face perpetual margin compression. The institutional winners of the FY2026 cycle will be those who successfully translate volatile biological assets into branded consumer IP and leverage automated, localized supply chains to eliminate cross-border compliance costs.

Presentation Download:

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Video Link: "Click this link to watch the YouTube video."

About HDIN Research:

HDIN Research is a premier independent market intelligence and strategic advisory firm. We specialize in deep-dive financial analysis, supply chain forensics, and institutional-grade geopolitical risk assessments. For more insights, visit www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*

Financial Health & Operational Moats: Escaping the Commodity Margin Trap

The FY2025 financial disclosures reveal a brutal divergence in Return on Invested Capital (ROIC) between asset-light "spread operators" and deeply vertically integrated players. The fresh meat sector is universally suffering from a rigid "cost ceiling," forcing a mass migration toward downstream FMCG (Fast-Moving Consumer Goods) product portfolios to activate cost-pass-through mechanisms.

Smithfield Foods serves as the blueprint for this transition. While its Fresh Pork operations recorded a razor-thin 2.6% operating margin, its Packaged Meats segment generated $8.76 billion—contributing a massive 85% of the company's overall operating profit. This structural moat completely insulates the firm from live hog volatility. Similarly, Hormel Foods (NYSE: HRL) sustained a resilient 15.6% corporate gross margin by leveraging high-premium consumer branding (SPAM®, Applegate®) rather than fighting in the commodity trenches.

Conversely, companies heavily exposed to biological asset holding periods and commodity cycles are exhibiting acute balance sheet stress. Muyuan Foods achieved a highly lucrative 20.57% ROE through strict vertical integration (driving total rearing costs down to $1.67/kg), yet it masks a severe liquidity mismatch: holding $1.92 billion in cash against a staggering $5.72 billion in short-term debt. Furthermore, HDIN analysts flag severe "high cash, high debt" anomalies at Shanghai Bright Meat (SHSE: 600073), which held $503.3 million in cash but incurred $20.6 million in interest expenses on $515.6 million in short-term borrowings—a classic indicator of inefficient capital allocation or restricted liquidity.

Figure Clobal Fresh Meat Sector 2025: Strategic Benchmarking & Financial Performance

Supply Chain Pivot: Localized Hedging and Geopolitical ArbitrageGlobal trade barriers are rendering the traditional export-heavy supply chain obsolete. Geopolitical friction, specifically China's 25% to 47% tariffs on U.S. pork offal, systematically dismantled the export margins of American producers in FY2025.

To hedge against this compliance friction, multinational giants are executing localized CAPEX strategies. JBS N.V. has insulated itself by deriving 74% of its net revenue from domestic sales within its operational footprints. The Brazilian titan is expanding its geographic arbitrage by deploying a $150 million multiprotein platform in Oman and an $85 million Seara plant in Saudi Arabia to capture the untariffed halal market.

Similarly, Shanghai Bright Meat executed a masterclass in supply chain hedging. Anticipating China’s impending three-year beef safeguard measure (which restricts imports from Brazil and the U.S. starting in 2026), Bright Meat leveraged its accretive acquisition of New Zealand’s Silver Fern Farms. This allowed the company to generate 49.1% of its revenue ($1.51 billion) overseas, securing premium beef sourcing that bypasses the targeted trade tariffs and creates a distinct pricing advantage over domestic competitors.

HDIN Institutional Perspective: CAPEX Reallocation Signals a Cyclical Trough

The global protein sector is actively navigating a late-stage cyclical trough, characterized by record-high cattle procurement costs in the Americas and an agonizingly slow inventory de-stocking phase in the Chinese pork market.

To breach the operational performance ceiling, industry leaders are abandoning volume growth. Tyson Foods has earmarked $0.7 billion to $1.0 billion in FY2026 CAPEX explicitly for automation and global network optimization—which includes shuttering inefficient legacy plants. Shuanghui Development (SZSE: 000895) is deploying $180.9 million into ERP overhauls and AI visual recognition for precise meat grading.

Ultimately, the FY2025 filings confirm that the moat in the protein sector is no longer scale; it is biosecurity, deep-processing capacity, and technological efficiency. Companies that rely strictly on wholesale commodity slaughtering face perpetual margin compression. The institutional winners of the FY2026 cycle will be those who successfully translate volatile biological assets into branded consumer IP and leverage automated, localized supply chains to eliminate cross-border compliance costs.

Presentation Download:

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Video Link: "Click this link to watch the YouTube video."

About HDIN Research:

HDIN Research is a premier independent market intelligence and strategic advisory firm. We specialize in deep-dive financial analysis, supply chain forensics, and institutional-grade geopolitical risk assessments. For more insights, visit www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*