Rentokil Initial Pivots to AI-Driven Route Density as FY2025 Terminix Restructuring Anchors 97.6% FCF Conversion

Date : 2026-04-10

Reading : 128

Rentokil Initial (NYSE: RTO) executed a critical strategic pivot in its FY2025 audit, halting a monolithic Terminix IT integration in favor of a decentralized, AI-driven operating model across North America. To combat margin compression from structural wage inflation and a highly sensitive $201 million legacy termite litigation provision, incoming CEO Mike Duffy inherits a mandate to aggressively scale the firm's digital networks. This restructuring generated $615 million in free cash flow, capitalizing on ruthless cost-pass-through mechanisms within its 70% contracted recurring revenue base to anchor a 15.5% adjusted operating margin.

Financial Health & Operational Moats: The Economics of High-Density Stickiness

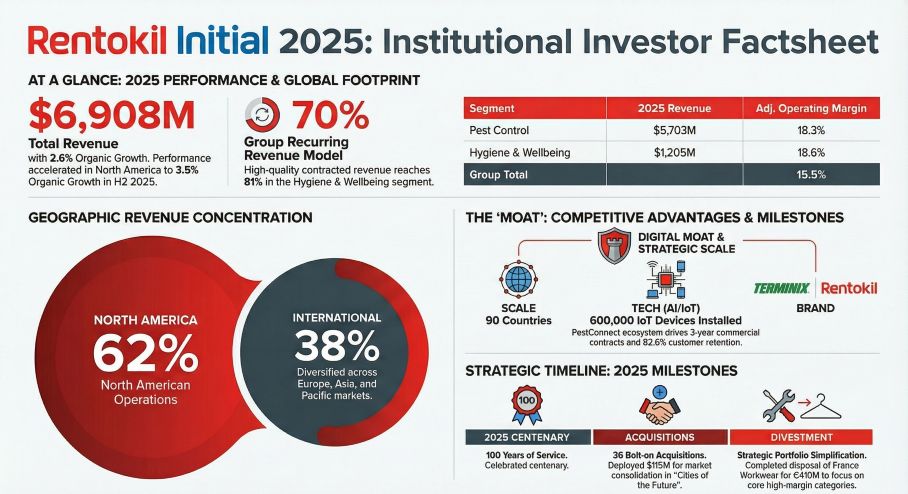

Rentokil’s FY2025 print of $6,908 million (+3.8% constant exchange rate) confirms that commercial pest control and hygiene are structurally immune to discretionary spending drawdowns. However, the true operational moat lies not in top-line volume, but in the pricing power embedded within its route-based subscription architecture.

The Group’s decision to execute aggressive above-inflation pricing actions resulted in an Adjusted Operating Profit of $1,070 million. By deliberately absorbing marginal volume reductions to protect yield, Rentokil leveraged strict cost-pass-through mechanisms. The Hygiene & Wellbeing division emerged as the margin leader, posting an 18.6% Adjusted Operating Margin (up 60 bps), definitively proving that post-pandemic sanitation spending has stabilized into a permanent regulatory compliance baseline.

The "So What" for institutional capital is found in the Group's technological lock-in. By deploying 600,000 *PestConnect* nodes globally—bolstered by the rollout of the *Optix* AI camera system that processed 4.1 million images to filter non-target triggers—Rentokil is fundamentally altering client unit economics. Commercial clients utilizing these IoT solutions typically convert from transactional annual agreements to 3-year recurring contracts. This digital entrenchment drove global customer retention up to 82.6%, insulating the firm from localized competitor undercutting while laying the groundwork to achieve its targeted >20% North American operating margin by 2027.

Figure Rentokil Initial 2025: Institutional Investor Factsheet

Supply Chain Pivot: Divestiture, Decarbonization, and Route Optimization

Supply Chain Pivot: Divestiture, Decarbonization, and Route Optimization

Rentokil is aggressively restructuring its physical footprint and supply chain to counter global macroeconomic volatility and tightening ESG mandates. The most decisive capital allocation move in 2025 was the strategic divestiture of the France Workwear division to H.I.G. Capital for an enterprise value of €410 million. This move severed the firm’s exposure to a highly unionized, low-margin European laundry supply chain, instantly removing 2,500 employees and allowing management to deploy capital toward 36 accretive acquisitions—primarily targeting "Cities of the Future" in hyper-growth emerging markets.

Upstream, the firm is navigating an aggressive regulatory pivot away from legacy chemicals. Facing tightening EPA and European green protocols, Rentokil achieved a 19.4% reduction in Sulfuryl Fluoride (SF) emissions equivalents. By localizing chemical and hardware procurement (such as the high-efficiency *Lumnia* LED traps and *EcoCatch* platforms), management effectively bypassed global shipping friction, mitigating the need for volatile inventory de-stocking cycles that have plagued broader industrial sectors. While full vertical integration of chemical manufacturing remains outside the firm's risk appetite, its hybrid sourcing model enforces a localized supply chain that matches its decentralized service footprint.

HDIN Institutional Perspective: The "Branch 360" M&A Recalibration

The defining narrative of the FY2025 filing is management’s implicit admission that the original Terminix integration strategy was operationally toxic. By attempting a forced, branch-by-branch IT migration, Rentokil risked destroying the localized brand equity that drives regional route density.

The pivot to a "decoupled" integration—retaining existing *Mission* and *PestPac* systems and layering them under a unified *Branch 360* business intelligence dashboard—is a masterclass in pragmatic consolidation. Instead of forcing technicians into disruptive software transitions, the Group harmonized pay plans and shifted back-office functions to Global Capability Centers. This preserved a critical 87.4% global colleague retention rate in a brutally tight labor market.

Looking ahead, the succession from veteran CEO Andy Ransom to Mike Duffy (formerly of OnTrac Logistics) signals to the Street that Rentokil no longer views itself purely as a pest control operator, but as a highly specialized, route-density logistics network. To defend its BBB investment-grade rating against the escalating cost of legacy termite claims, the Group will rely heavily on its proprietary *RatGPT* AI agents and satellite branch strategy to squeeze structural waste from its North American routes.

Presentation Download & Video Access

* Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

* Video Link: Click this link to watch the YouTube video.

About HDIN Research:

HDIN Research is a premier provider of institutional-grade market intelligence and corporate strategy analysis. By combining rigorous financial auditing with geopolitical and macroeconomic context, we equip global investors and corporate boards with the decisive insights needed to navigate complex market transitions. (www.hdinresearch.com)

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*

Financial Health & Operational Moats: The Economics of High-Density Stickiness

Rentokil’s FY2025 print of $6,908 million (+3.8% constant exchange rate) confirms that commercial pest control and hygiene are structurally immune to discretionary spending drawdowns. However, the true operational moat lies not in top-line volume, but in the pricing power embedded within its route-based subscription architecture.

The Group’s decision to execute aggressive above-inflation pricing actions resulted in an Adjusted Operating Profit of $1,070 million. By deliberately absorbing marginal volume reductions to protect yield, Rentokil leveraged strict cost-pass-through mechanisms. The Hygiene & Wellbeing division emerged as the margin leader, posting an 18.6% Adjusted Operating Margin (up 60 bps), definitively proving that post-pandemic sanitation spending has stabilized into a permanent regulatory compliance baseline.

The "So What" for institutional capital is found in the Group's technological lock-in. By deploying 600,000 *PestConnect* nodes globally—bolstered by the rollout of the *Optix* AI camera system that processed 4.1 million images to filter non-target triggers—Rentokil is fundamentally altering client unit economics. Commercial clients utilizing these IoT solutions typically convert from transactional annual agreements to 3-year recurring contracts. This digital entrenchment drove global customer retention up to 82.6%, insulating the firm from localized competitor undercutting while laying the groundwork to achieve its targeted >20% North American operating margin by 2027.

Figure Rentokil Initial 2025: Institutional Investor Factsheet

Supply Chain Pivot: Divestiture, Decarbonization, and Route Optimization Rentokil is aggressively restructuring its physical footprint and supply chain to counter global macroeconomic volatility and tightening ESG mandates. The most decisive capital allocation move in 2025 was the strategic divestiture of the France Workwear division to H.I.G. Capital for an enterprise value of €410 million. This move severed the firm’s exposure to a highly unionized, low-margin European laundry supply chain, instantly removing 2,500 employees and allowing management to deploy capital toward 36 accretive acquisitions—primarily targeting "Cities of the Future" in hyper-growth emerging markets.

Upstream, the firm is navigating an aggressive regulatory pivot away from legacy chemicals. Facing tightening EPA and European green protocols, Rentokil achieved a 19.4% reduction in Sulfuryl Fluoride (SF) emissions equivalents. By localizing chemical and hardware procurement (such as the high-efficiency *Lumnia* LED traps and *EcoCatch* platforms), management effectively bypassed global shipping friction, mitigating the need for volatile inventory de-stocking cycles that have plagued broader industrial sectors. While full vertical integration of chemical manufacturing remains outside the firm's risk appetite, its hybrid sourcing model enforces a localized supply chain that matches its decentralized service footprint.

HDIN Institutional Perspective: The "Branch 360" M&A Recalibration

The defining narrative of the FY2025 filing is management’s implicit admission that the original Terminix integration strategy was operationally toxic. By attempting a forced, branch-by-branch IT migration, Rentokil risked destroying the localized brand equity that drives regional route density.

The pivot to a "decoupled" integration—retaining existing *Mission* and *PestPac* systems and layering them under a unified *Branch 360* business intelligence dashboard—is a masterclass in pragmatic consolidation. Instead of forcing technicians into disruptive software transitions, the Group harmonized pay plans and shifted back-office functions to Global Capability Centers. This preserved a critical 87.4% global colleague retention rate in a brutally tight labor market.

Looking ahead, the succession from veteran CEO Andy Ransom to Mike Duffy (formerly of OnTrac Logistics) signals to the Street that Rentokil no longer views itself purely as a pest control operator, but as a highly specialized, route-density logistics network. To defend its BBB investment-grade rating against the escalating cost of legacy termite claims, the Group will rely heavily on its proprietary *RatGPT* AI agents and satellite branch strategy to squeeze structural waste from its North American routes.

Presentation Download & Video Access

* Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

* Video Link: Click this link to watch the YouTube video.

About HDIN Research:

HDIN Research is a premier provider of institutional-grade market intelligence and corporate strategy analysis. By combining rigorous financial auditing with geopolitical and macroeconomic context, we equip global investors and corporate boards with the decisive insights needed to navigate complex market transitions. (www.hdinresearch.com)

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*