Radiopharmaceutical Leaders Shift to Vertical Integration: Novartis and Dongcheng Post Diverging Margins Amid Supply Chain Sovereignty Arms Race

Date : 2026-04-10

Reading : 184

In the FY2025 audit cycle, global radiopharmaceutical incumbents and regional CDMOs—including Novartis (NYSE: NVS), Dongcheng Pharmaceutical (SZSE: 002675), and DuChemBio (KOSDAQ: 176750)—aggressively reallocated CAPEX toward localized GMP manufacturing across the US, Europe, and Asia. Driven by the immutable physical decay rates of medical isotopes (Lu-177 and Ac-225), these players are trading traditional molecular IP strategies for hard-asset vertical integration. As Novartis counters US IRA margin compression with a $1.99 billion surge in Pluvicto sales, Asian challengers are exploiting geographic moats, proving that regional "steel in the ground" outweighs imported clinical efficacy.

Financial Health & Operational Moats: The Productivity Bifurcation

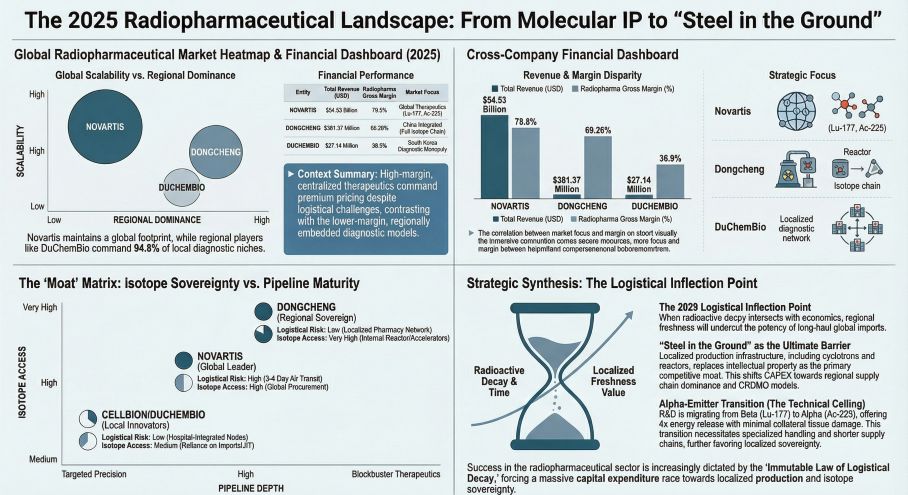

An analysis of 2025 corporate disclosures reveals a stark bifurcation in labor productivity and capital efficiency, dictated entirely by a company's position on the half-life decay spectrum.

Novartis operates at the apex of margin expansion. Buoyed by a 78.8% gross margin and generating approximately $724,514 in revenue per employee, the Swiss giant relies on the slightly longer half-life of Lutetium-177 (6.7 days) to centralize production. The firm’s massive volume leverage drove a CFO-to-Net-Income ratio of 1.37x, yielding $19.14 billion in operational cash flow. However, this centralized model faces looming margin compression via the US Inflation Reduction Act (IRA) and mandatory Medicare price negotiations, forcing Novartis to rely heavily on outcome-based contracting and direct-to-patient commercial platforms.

Conversely, Dongcheng Pharmaceutical illustrates the ultimate infrastructure toll-bridge. Generating $158.00 million from its nuclear medicine division (a 12.21% YoY increase), the firm boasts a 69.26% segment gross margin. Yet, its consolidated net margin is suppressed to a mere 7.14%. *The strategic takeaway:* To achieve a near-monopoly in China (covering 93.5% of the population), Dongcheng operates 31 highly regulated, decentralized nuclear pharmacies. This necessitates intense, localized headcount and a dedicated radiation logistics fleet (e.g., Suzhou Jielianda). The structural drag on human capital productivity is the exact cost of an unassailable geographic moat. Furthermore, Dongcheng’s exceptionally high CFO-to-Net-Income ratio of 3.75x reflects aggressive API inventory de-stocking, shielding its balance sheet against macroeconomic volatility.

On the pre-commercial front, Cellbion (KOSDAQ: 317320) exhibits classic biotech cash-burn (-$5.33M net loss), reliant on IPO capital buffers. While management cites a "virtually debt-free" structure, closer inspection of its K-IFRS 1116 filings reveals 54.45% accounting debt ratios directly tied to lease liabilities for new domestic GMP facilities—a necessary expenditure to bypass import tariffs and aviation delays.

Figure The 2025 Radiopharmaceutical Landscape: From Molecular IP to Steel in the Ground

Supply Chain Pivot: The "Steel in the Ground" Mandate

Supply Chain Pivot: The "Steel in the Ground" Mandate

The traditional pharmaceutical playbook—synthesizing active pharmaceutical ingredients (APIs) in low-cost offshore hubs—is structurally impossible in Theranostics. Because isotopes like Fluorine-18 decay within 110 minutes, inventory turnover is measured in hours.

To secure upstream supply chain sovereignty, Dongcheng is executing an unprecedented CAPEX rollout via its "One Reactor, Two Accelerators" strategy. In March 2025, the firm achieved first concrete pouring (FCD) for the Jiujiang Tianhong Medical Isotope Dedicated Reactor in Jiangxi, alongside the structural completion of a 40MeV electron accelerator and the installation of a 30MeV proton cyclotron. This physically insulates Dongcheng from aging global nuclear reactor downtime, ensuring independent yields of next-generation Actinium-225 (Ac-225) and Copper-67 (67Cu).

Novartis is countering this localized threat through aggressive downstream capacity cloning. In 2025, the firm deployed $1.38 billion to expand Property, Plant, and Equipment (PPE), systematically bringing a dedicated 8,230-square-meter facility in Indianapolis and a 4,300-square-meter site in Ivrea, Italy, online.

Simultaneously, South Korea’s DuChemBio is leveraging open innovation, refusing early-stage R&D risk. Instead, it utilizes its 12 regional GMP manufacturing sites to execute rapid domestic commercialization of late-stage in-licensed assets, successfully locking down 94.8% of the Alzheimer's PET market.

HDIN Institutional Perspective: IP is Subservient to Infrastructure

Our editorial board assesses that the Theranostics sector has crossed a critical inflection point: intellectual property is now entirely subservient to physical infrastructure.

Standard AI-generated sector reports routinely over-index on molecular targeting (e.g., PSMA or SSTR ligands). We argue this misses the true barrier to entry. Building a radiopharmaceutical supply chain requires solving an engineering paradox: navigating Radiation Safety laws (requiring *negative pressure* hot-cells to contain deadly leaks) while simultaneously adhering to sterile GMP regulations (requiring *positive pressure* cleanrooms to block biological contaminants).

Global entities like Novartis remain highly exposed to the immutable laws of logistical decay. Air-freighting Lu-177 from Europe to Asia sacrifices 3 to 4 days of a 6.7-day half-life. By 2028, as the clinical standard of care shifts from Beta-emitters (Lu-177) to ultra-short-range Alpha-emitters (Ac-225, Pb-212), this centralized logistical model will break. Regional innovators like Cellbion—advancing its 177Lu-Pocuvotide—will exploit this by synchronizing localized GMP synthesis with immediate domestic insurance reimbursement, executing a cost-pass-through mechanism that imported big-pharma competitors simply cannot match. Accretive acquisitions of regional CDMOs will be the only viable survival tactic for Western incumbents seeking Asian market share.

Presentation Download & Video Access

* Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

* Video Link: Click this link to watch the YouTube video.

About HDIN Research:

HDIN Research is a premier institutional market intelligence firm providing bespoke analytics on global supply chain shifts, regulatory frameworks, and advanced medical technologies. Visit us at www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*

Financial Health & Operational Moats: The Productivity Bifurcation

An analysis of 2025 corporate disclosures reveals a stark bifurcation in labor productivity and capital efficiency, dictated entirely by a company's position on the half-life decay spectrum.

Novartis operates at the apex of margin expansion. Buoyed by a 78.8% gross margin and generating approximately $724,514 in revenue per employee, the Swiss giant relies on the slightly longer half-life of Lutetium-177 (6.7 days) to centralize production. The firm’s massive volume leverage drove a CFO-to-Net-Income ratio of 1.37x, yielding $19.14 billion in operational cash flow. However, this centralized model faces looming margin compression via the US Inflation Reduction Act (IRA) and mandatory Medicare price negotiations, forcing Novartis to rely heavily on outcome-based contracting and direct-to-patient commercial platforms.

Conversely, Dongcheng Pharmaceutical illustrates the ultimate infrastructure toll-bridge. Generating $158.00 million from its nuclear medicine division (a 12.21% YoY increase), the firm boasts a 69.26% segment gross margin. Yet, its consolidated net margin is suppressed to a mere 7.14%. *The strategic takeaway:* To achieve a near-monopoly in China (covering 93.5% of the population), Dongcheng operates 31 highly regulated, decentralized nuclear pharmacies. This necessitates intense, localized headcount and a dedicated radiation logistics fleet (e.g., Suzhou Jielianda). The structural drag on human capital productivity is the exact cost of an unassailable geographic moat. Furthermore, Dongcheng’s exceptionally high CFO-to-Net-Income ratio of 3.75x reflects aggressive API inventory de-stocking, shielding its balance sheet against macroeconomic volatility.

On the pre-commercial front, Cellbion (KOSDAQ: 317320) exhibits classic biotech cash-burn (-$5.33M net loss), reliant on IPO capital buffers. While management cites a "virtually debt-free" structure, closer inspection of its K-IFRS 1116 filings reveals 54.45% accounting debt ratios directly tied to lease liabilities for new domestic GMP facilities—a necessary expenditure to bypass import tariffs and aviation delays.

Figure The 2025 Radiopharmaceutical Landscape: From Molecular IP to Steel in the Ground

Supply Chain Pivot: The "Steel in the Ground" MandateThe traditional pharmaceutical playbook—synthesizing active pharmaceutical ingredients (APIs) in low-cost offshore hubs—is structurally impossible in Theranostics. Because isotopes like Fluorine-18 decay within 110 minutes, inventory turnover is measured in hours.

To secure upstream supply chain sovereignty, Dongcheng is executing an unprecedented CAPEX rollout via its "One Reactor, Two Accelerators" strategy. In March 2025, the firm achieved first concrete pouring (FCD) for the Jiujiang Tianhong Medical Isotope Dedicated Reactor in Jiangxi, alongside the structural completion of a 40MeV electron accelerator and the installation of a 30MeV proton cyclotron. This physically insulates Dongcheng from aging global nuclear reactor downtime, ensuring independent yields of next-generation Actinium-225 (Ac-225) and Copper-67 (67Cu).

Novartis is countering this localized threat through aggressive downstream capacity cloning. In 2025, the firm deployed $1.38 billion to expand Property, Plant, and Equipment (PPE), systematically bringing a dedicated 8,230-square-meter facility in Indianapolis and a 4,300-square-meter site in Ivrea, Italy, online.

Simultaneously, South Korea’s DuChemBio is leveraging open innovation, refusing early-stage R&D risk. Instead, it utilizes its 12 regional GMP manufacturing sites to execute rapid domestic commercialization of late-stage in-licensed assets, successfully locking down 94.8% of the Alzheimer's PET market.

HDIN Institutional Perspective: IP is Subservient to Infrastructure

Our editorial board assesses that the Theranostics sector has crossed a critical inflection point: intellectual property is now entirely subservient to physical infrastructure.

Standard AI-generated sector reports routinely over-index on molecular targeting (e.g., PSMA or SSTR ligands). We argue this misses the true barrier to entry. Building a radiopharmaceutical supply chain requires solving an engineering paradox: navigating Radiation Safety laws (requiring *negative pressure* hot-cells to contain deadly leaks) while simultaneously adhering to sterile GMP regulations (requiring *positive pressure* cleanrooms to block biological contaminants).

Global entities like Novartis remain highly exposed to the immutable laws of logistical decay. Air-freighting Lu-177 from Europe to Asia sacrifices 3 to 4 days of a 6.7-day half-life. By 2028, as the clinical standard of care shifts from Beta-emitters (Lu-177) to ultra-short-range Alpha-emitters (Ac-225, Pb-212), this centralized logistical model will break. Regional innovators like Cellbion—advancing its 177Lu-Pocuvotide—will exploit this by synchronizing localized GMP synthesis with immediate domestic insurance reimbursement, executing a cost-pass-through mechanism that imported big-pharma competitors simply cannot match. Accretive acquisitions of regional CDMOs will be the only viable survival tactic for Western incumbents seeking Asian market share.

Presentation Download & Video Access

* Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

* Video Link: Click this link to watch the YouTube video.

About HDIN Research:

HDIN Research is a premier institutional market intelligence firm providing bespoke analytics on global supply chain shifts, regulatory frameworks, and advanced medical technologies. Visit us at www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*