Assisted Reproductive Market Hits VBP Price Ceiling: Livzon and Renfu Shield Margins via Vertical Integration as Organon Absorbs $301M Impairment

Date : 2026-04-10

Reading : 444

In the FY2025 audit cycle, global reproductive health leaders Organon & Co. (NYSE: OGN), Livzon Pharmaceutical Group (SZSE: 000513), and Humanwell Healthcare/Renfu (SSE: 600079) deployed diverging CapEx and R&D strategies to combat margin compression driven by shifting demographic cycles and Volume-Based Procurement (VBP) pricing caps. While Organon utilizes a "contraception-plus-fertility" portfolio to hedge macroeconomic birth rate declines, it faces a $301 million goodwill impairment. Conversely, Chinese incumbents Livzon and Renfu are sustaining core margins through vertical integration, shifting active pharmaceutical ingredient (API) manufacturing to Southeast Asia, and deploying Agentic AI platforms, signaling a structural pivot from generic price wars to high-barrier complex formulations.

Financial Health & Operational Moats: The Cost of Debt vs. Complex Formulation Yields

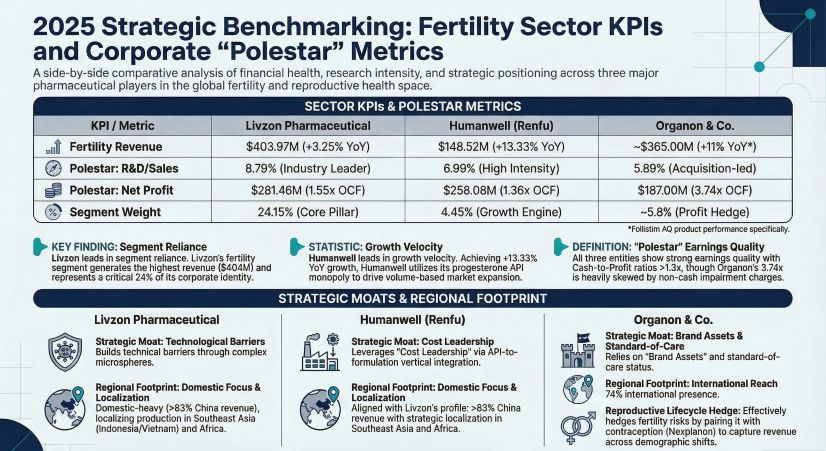

A forensic analysis of FY2025 earnings quality reveals severe divergence in operational leverage and cash conversion cycles across the cohort.

Organon & Co. (NYSE: OGN) reported a robust operating cash flow (OCF) of $700 million against a net profit of just $187 million (a 3.74x Cash-to-Profit ratio). However, this mathematical cash conversion masks a deteriorating balance sheet. The divergence is primarily fueled by a massive $301 million goodwill impairment on its US reporting unit and $205 million in amortization charges. Burdened by an $8.628 billion post-spinoff debt load, Organon faces a critical refinancing wall with $3.6 billion in notes maturing in 2028. In FY2025 alone, interest expenses devoured $504 million, heavily suppressing net income and threatening future accretive acquisitions or dividend stability.

Conversely, Livzon Pharmaceutical (SZSE: 000513) showcases superior earnings quality with a 1.55x Cash-to-Profit ratio ($437.56 million OCF vs. $281.46 million net profit). Livzon circumvents VBP margin compression through a high-barrier complex formulation moat. Its chemical preparations segment maintains an 81.06% gross margin, driven by its proprietary long-acting sustained-release microsphere technology. Livzon's rapid accounts receivable (AR) turnover of 5.35x (roughly 68 days) underscores its immense bargaining power over downstream hospitals.

Renfu Medicine (SSE: 600079) exhibits solid cash generation ($350.33 million OCF) but faces structural liquidity drag. Its AR turnover ratio sits at a sluggish 2.45x (148 days), tying up $1.35 billion in working capital. More critically, Renfu's balance sheet flashes a severe corporate governance red flag: $1.03 billion in opaque "Other receivables from internal related parties," exposing investors to significant intra-group capital occupation risks despite its dominant >60% domestic market share in narcotic and anesthesia APIs.

Figure 2025 Strategic Benchmarking: Fertility Sector KPls and Corporate“Polestar” Metrics

Supply Chain Pivot: Geopolitical Decoupling and API Localization

Supply Chain Pivot: Geopolitical Decoupling and API Localization

To insulate against macroeconomic volatility and geopolitical trade friction, all three entities executed aggressive, localized CapEx deployments in FY2025 aimed at securing upstream supply chains.

* Organon’s Western Internalization: Organon explicitly directed CapEx to sever its legacy reliance on Merck’s supply chain. The $96 million acquisition of the Oss Biotech facility in the Netherlands ($25M for the site, $71M for inventory) is a targeted defensive move to internalize the production of its core fertility drug substances, specifically for its cash-cow Follistim AQ ($264 million FY2025 revenue).

* Livzon’s Southeast Asian Bridgehead: Livzon is aggressively localizing its supply chain within the ASEAN block. Beyond constructing a high-standard sterile API plant in Jakarta, Indonesia, Livzon initiated the acquisition of a 77.94% stake in Imexpharm Corporation (IMP) in Vietnam. Leveraging IMP’s EU-GMP-certified production lines establishes a vital node to bypass Western trade tariffs while dominating emerging Belt and Road markets.

* Renfu’s B2B Dominance & African Expansion: Renfu directed heavy CapEx toward the Gedian Renfu high-end API industrialization base to maintain its global monopoly in progesterone raw materials. Simultaneously, its subsidiary Epic Pharma continues to hold ~230 FDA-approved ANDAs in New York, while the company deepens its localized commercial footprint through manufacturing hubs like Humanwell Mali and Humanwell Ethiopia, embedding itself directly into local government procurement systems.

R&D Capitalization & AI-Driven Digitalization

The integration of Artificial Intelligence has transitioned from speculative R&D to a core operational mandate designed to slash time-to-market and force cost-pass-through efficiencies.

Livzon demonstrates the most advanced "Agentic AI" deployment. By replacing manual quality control (QC) in microsphere manufacturing with AI image recognition, Livzon collapsed batch inspection times from 10 hours to a mere 60 seconds. Livzon also aggressively increased its R&D capitalization rate from 3.51% to 13.67% in FY2025. While this mathematically inflates current-period net profit, corporate filings validate the capitalization against late-stage assets entering Phase III trials (e.g., JP1366).

Renfu has officially launched its proprietary MolStata AIDD/CADD platform, securing software copyrights to accelerate early-stage drug discovery, heavily deploying AI to retain its cost leadership in steroid hormone API screening. Organon, lacking proprietary drug formulation AI platforms, focuses its filings on the cybersecurity and ethical governance risks associated with third-party generative AI adoption, highlighting the vulnerability of clinical trial data in vendor-managed ecosystems.

HDIN Institutional Perspective

The FY2025 audit data confirms that the global assisted reproductive technology (ART) and women’s health sector has hit a systemic policy ceiling. In highly regulated markets like China, the Universal Reimbursement Payment Standard (URPS) and VBP have eradicated the premium pricing power of standard generic fertility treatments.

Survival in this cycle requires distinct structural hedging. Organon executes this via an "internal macro-hedge," balancing its Nexplanon contraception revenues against Follistim fertility revenues to smooth out demographic volatility. The Chinese cohort relies on regulatory and technical moats: Renfu utilizes the strict national procurement regulations governing its narcotic API monopoly to achieve absolute "VBP exemption," effectively subsidizing its reproductive pipeline. Livzon, executing the most technically sound strategy, uses state-of-the-art microsphere platforms and dual "urine-derived plus recombinant" pathways to render generic competition obsolete. Moving toward FY2026, companies failing to vertically integrate their API supply lines or upgrade to complex formulations will face terminal margin compression.

Presentation Download & Video Access

Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

Video Link: Click this link to watch the YouTube video.

About HDIN Research:

HDIN Research is a premier global market intelligence and investment strategy firm. We specialize in MECE-driven, forensic financial analysis and macroeconomic trend forecasting, empowering institutional investors to navigate complex geopolitical and regulatory landscapes. Visit us at www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*

Financial Health & Operational Moats: The Cost of Debt vs. Complex Formulation Yields

A forensic analysis of FY2025 earnings quality reveals severe divergence in operational leverage and cash conversion cycles across the cohort.

Organon & Co. (NYSE: OGN) reported a robust operating cash flow (OCF) of $700 million against a net profit of just $187 million (a 3.74x Cash-to-Profit ratio). However, this mathematical cash conversion masks a deteriorating balance sheet. The divergence is primarily fueled by a massive $301 million goodwill impairment on its US reporting unit and $205 million in amortization charges. Burdened by an $8.628 billion post-spinoff debt load, Organon faces a critical refinancing wall with $3.6 billion in notes maturing in 2028. In FY2025 alone, interest expenses devoured $504 million, heavily suppressing net income and threatening future accretive acquisitions or dividend stability.

Conversely, Livzon Pharmaceutical (SZSE: 000513) showcases superior earnings quality with a 1.55x Cash-to-Profit ratio ($437.56 million OCF vs. $281.46 million net profit). Livzon circumvents VBP margin compression through a high-barrier complex formulation moat. Its chemical preparations segment maintains an 81.06% gross margin, driven by its proprietary long-acting sustained-release microsphere technology. Livzon's rapid accounts receivable (AR) turnover of 5.35x (roughly 68 days) underscores its immense bargaining power over downstream hospitals.

Renfu Medicine (SSE: 600079) exhibits solid cash generation ($350.33 million OCF) but faces structural liquidity drag. Its AR turnover ratio sits at a sluggish 2.45x (148 days), tying up $1.35 billion in working capital. More critically, Renfu's balance sheet flashes a severe corporate governance red flag: $1.03 billion in opaque "Other receivables from internal related parties," exposing investors to significant intra-group capital occupation risks despite its dominant >60% domestic market share in narcotic and anesthesia APIs.

Figure 2025 Strategic Benchmarking: Fertility Sector KPls and Corporate“Polestar” Metrics

Supply Chain Pivot: Geopolitical Decoupling and API LocalizationTo insulate against macroeconomic volatility and geopolitical trade friction, all three entities executed aggressive, localized CapEx deployments in FY2025 aimed at securing upstream supply chains.

* Organon’s Western Internalization: Organon explicitly directed CapEx to sever its legacy reliance on Merck’s supply chain. The $96 million acquisition of the Oss Biotech facility in the Netherlands ($25M for the site, $71M for inventory) is a targeted defensive move to internalize the production of its core fertility drug substances, specifically for its cash-cow Follistim AQ ($264 million FY2025 revenue).

* Livzon’s Southeast Asian Bridgehead: Livzon is aggressively localizing its supply chain within the ASEAN block. Beyond constructing a high-standard sterile API plant in Jakarta, Indonesia, Livzon initiated the acquisition of a 77.94% stake in Imexpharm Corporation (IMP) in Vietnam. Leveraging IMP’s EU-GMP-certified production lines establishes a vital node to bypass Western trade tariffs while dominating emerging Belt and Road markets.

* Renfu’s B2B Dominance & African Expansion: Renfu directed heavy CapEx toward the Gedian Renfu high-end API industrialization base to maintain its global monopoly in progesterone raw materials. Simultaneously, its subsidiary Epic Pharma continues to hold ~230 FDA-approved ANDAs in New York, while the company deepens its localized commercial footprint through manufacturing hubs like Humanwell Mali and Humanwell Ethiopia, embedding itself directly into local government procurement systems.

R&D Capitalization & AI-Driven Digitalization

The integration of Artificial Intelligence has transitioned from speculative R&D to a core operational mandate designed to slash time-to-market and force cost-pass-through efficiencies.

Livzon demonstrates the most advanced "Agentic AI" deployment. By replacing manual quality control (QC) in microsphere manufacturing with AI image recognition, Livzon collapsed batch inspection times from 10 hours to a mere 60 seconds. Livzon also aggressively increased its R&D capitalization rate from 3.51% to 13.67% in FY2025. While this mathematically inflates current-period net profit, corporate filings validate the capitalization against late-stage assets entering Phase III trials (e.g., JP1366).

Renfu has officially launched its proprietary MolStata AIDD/CADD platform, securing software copyrights to accelerate early-stage drug discovery, heavily deploying AI to retain its cost leadership in steroid hormone API screening. Organon, lacking proprietary drug formulation AI platforms, focuses its filings on the cybersecurity and ethical governance risks associated with third-party generative AI adoption, highlighting the vulnerability of clinical trial data in vendor-managed ecosystems.

HDIN Institutional Perspective

The FY2025 audit data confirms that the global assisted reproductive technology (ART) and women’s health sector has hit a systemic policy ceiling. In highly regulated markets like China, the Universal Reimbursement Payment Standard (URPS) and VBP have eradicated the premium pricing power of standard generic fertility treatments.

Survival in this cycle requires distinct structural hedging. Organon executes this via an "internal macro-hedge," balancing its Nexplanon contraception revenues against Follistim fertility revenues to smooth out demographic volatility. The Chinese cohort relies on regulatory and technical moats: Renfu utilizes the strict national procurement regulations governing its narcotic API monopoly to achieve absolute "VBP exemption," effectively subsidizing its reproductive pipeline. Livzon, executing the most technically sound strategy, uses state-of-the-art microsphere platforms and dual "urine-derived plus recombinant" pathways to render generic competition obsolete. Moving toward FY2026, companies failing to vertically integrate their API supply lines or upgrade to complex formulations will face terminal margin compression.

Presentation Download & Video Access

Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

Video Link: Click this link to watch the YouTube video.

About HDIN Research:

HDIN Research is a premier global market intelligence and investment strategy firm. We specialize in MECE-driven, forensic financial analysis and macroeconomic trend forecasting, empowering institutional investors to navigate complex geopolitical and regulatory landscapes. Visit us at www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*