Novonesis Executes Specialty Chemicals Pivot as FY2025 AI-Accelerated R&D Drives 7% Organic Growth Benchmark.

Date : 2026-04-10

Reading : 205

Novonesis (CPH: NSIS-B) delivered a sector-beating 7% organic top-line expansion and a 100-basis-point margin accretion in FY2025, neutralizing macroeconomic headwinds across its 32 global manufacturing sites. Driven by the accelerated integration of Chr. Hansen and the $1.79 billion accretive acquisition of dsm-firmenich’s Feed Enzyme Alliance, the pure-play biosolutions giant leveraged AI-optimized R&D to offset broader chemical industry volatility. By structurally embedding value-based pricing and achieving multi-year cost synergies a full 12 months ahead of schedule, Novonesis validated its 2030 GROW mandate to capture the $1.13 trillion specialty chemicals TAM.

Financial Health & Operational Moats: The Algorithm of Biology

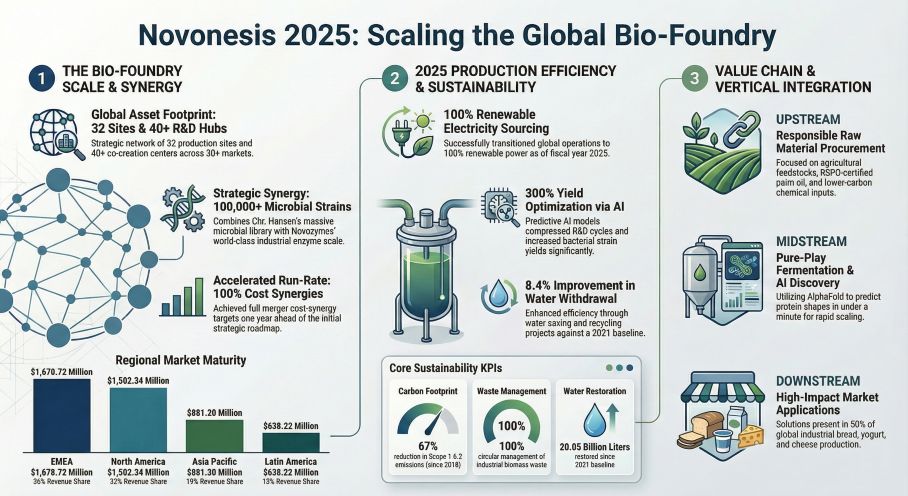

Novonesis’s FY2025 audit underscores a fortress balance sheet operating at peak cash conversion, effectively immune to the margin compression currently plaguing the synthetic chemicals sector. Generating $4,700.58 million in net sales, the underlying growth engine fired symmetrically: the Food & Health Biosolutions division posted 8% organic growth, while Planetary Health Biosolutions secured 6%.

The true operational moat, however, lies in the company’s elite capital deployment engine. Adjusted EBITDA scaled to $1,744.86 million (a 37.1% margin), catalyzed not merely by volume leverage, but by the deployment of structural cost-pass-through mechanisms and high-margin co-creation pricing models. Novonesis funneled $532.29 million (11.3% of sales) into capital expenditures, intentionally heavily skewed toward expanding global fermentation capacity.

More critically, the 11.2% R&D reinvestment ($524.4 million) transitions Novonesis from a traditional biosciences firm into a predictive biological data engine. By integrating Google DeepMind’s AlphaFold and quantum-hybrid architectures via Kvantify, Novonesis collapsed protein sequence prediction timelines from a year to under 60 seconds. This hyper-accelerated R&D pipeline yielded 33 new product launches in 2025—85% secured by new patents—and drove bacterial yields up by 300%. The "So What" is quantified in the company’s 25% Vitality Index: a full quarter of total revenue ($1.17 billion) is now generated by products engineered within the last five years, locking in impenetrable customer stickiness.

Figure Novonesis 2025: Scaling the Global Bio-Foundry

Supply Chain Pivot: Vertical Integration Meets Decarbonization

Supply Chain Pivot: Vertical Integration Meets Decarbonization

Amidst global trade friction and cyclical inventory de-stocking, Novonesis executed a masterclass in supply chain derisking. The strategic architecture eschews the vulnerable mega-factory model in favor of a decentralized, 32-site global production footprint, engineering built-in redundancy against climate-induced feedstock scarcity.

The $1,794.26 million vertical integration of the Feed Enzyme Alliance from dsm-firmenich fundamentally altered the company's upstream leverage. By acquiring the sales and distribution operations of a 25-year partnership, Novonesis internalized the entire margin pool across the animal biosolutions value chain.

Simultaneously, the procurement apparatus is weaponizing its Scope 3 emissions targets as an operational efficiency tool. Through its "PAVE to Zero" protocol, Novonesis aggressively substituted single-sourced high-carbon inputs (ammonia and liquid nitrogen) with dual-sourced greener alternatives, while executing a modal logistics shift to sustainable maritime fuels (SMF). Divestitures further ruthlessly optimized the footprint: clearing European Commission antitrust hurdles by selling the lactase enzyme business to Kerry Group plc for $163.37 million, and offloading the legacy Bagsvaerd headquarters to Novo Nordisk A/S for $18.99 million.

HDIN Institutional Perspective

Novonesis is fundamentally mispriced by analysts who continue to benchmark it against traditional specialty chemical peers (IFF, Symrise, Givaudan)—a cohort that saw a 25.4% market downturn in 2025. Novonesis is not a chemical company; it is an industrial software company where the code is written in microbial strains.

The early 100% run-rate realization of the Novozymes-Chr. Hansen cost synergies insulated the bottom line from severe EUR/USD currency headwinds. Management’s deliberate balance sheet engineering—temporarily spiking NIBD/EBITDA leverage to 1.9x via a bridge loan for the Feed Enzyme Alliance—is a calculated execution of accretive M&A. Supported by $871.01 million in free cash flow, deleveraging to the targeted 1.7x by 2026 is mathematically secure. Looking forward to the 2026 guidance (5–7% organic growth, 37–38% EBITDA margin, and elevated 12–14% CAPEX), Novonesis is visibly positioning its balance sheet to capitalize on the trough of the petrochemical cycle. As regulatory frameworks like the EU Chemical Strategy for Sustainability enforce biological substitution, Novonesis holds the apex pricing power.

Presentation Download & Video Access

* Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

* Video Link: Click this link to watch the YouTube video.

About HDIN Research

HDIN Research is a premier global market intelligence and institutional advisory firm. We specialize in forensic financial analysis, supply chain deconstruction, and macroeconomic strategic forecasting to provide unparalleled alpha generation for institutional investors and corporate strategists. Visit us at www.hdinresearch.com.

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.

Financial Health & Operational Moats: The Algorithm of Biology

Novonesis’s FY2025 audit underscores a fortress balance sheet operating at peak cash conversion, effectively immune to the margin compression currently plaguing the synthetic chemicals sector. Generating $4,700.58 million in net sales, the underlying growth engine fired symmetrically: the Food & Health Biosolutions division posted 8% organic growth, while Planetary Health Biosolutions secured 6%.

The true operational moat, however, lies in the company’s elite capital deployment engine. Adjusted EBITDA scaled to $1,744.86 million (a 37.1% margin), catalyzed not merely by volume leverage, but by the deployment of structural cost-pass-through mechanisms and high-margin co-creation pricing models. Novonesis funneled $532.29 million (11.3% of sales) into capital expenditures, intentionally heavily skewed toward expanding global fermentation capacity.

More critically, the 11.2% R&D reinvestment ($524.4 million) transitions Novonesis from a traditional biosciences firm into a predictive biological data engine. By integrating Google DeepMind’s AlphaFold and quantum-hybrid architectures via Kvantify, Novonesis collapsed protein sequence prediction timelines from a year to under 60 seconds. This hyper-accelerated R&D pipeline yielded 33 new product launches in 2025—85% secured by new patents—and drove bacterial yields up by 300%. The "So What" is quantified in the company’s 25% Vitality Index: a full quarter of total revenue ($1.17 billion) is now generated by products engineered within the last five years, locking in impenetrable customer stickiness.

Figure Novonesis 2025: Scaling the Global Bio-Foundry

Supply Chain Pivot: Vertical Integration Meets DecarbonizationAmidst global trade friction and cyclical inventory de-stocking, Novonesis executed a masterclass in supply chain derisking. The strategic architecture eschews the vulnerable mega-factory model in favor of a decentralized, 32-site global production footprint, engineering built-in redundancy against climate-induced feedstock scarcity.

The $1,794.26 million vertical integration of the Feed Enzyme Alliance from dsm-firmenich fundamentally altered the company's upstream leverage. By acquiring the sales and distribution operations of a 25-year partnership, Novonesis internalized the entire margin pool across the animal biosolutions value chain.

Simultaneously, the procurement apparatus is weaponizing its Scope 3 emissions targets as an operational efficiency tool. Through its "PAVE to Zero" protocol, Novonesis aggressively substituted single-sourced high-carbon inputs (ammonia and liquid nitrogen) with dual-sourced greener alternatives, while executing a modal logistics shift to sustainable maritime fuels (SMF). Divestitures further ruthlessly optimized the footprint: clearing European Commission antitrust hurdles by selling the lactase enzyme business to Kerry Group plc for $163.37 million, and offloading the legacy Bagsvaerd headquarters to Novo Nordisk A/S for $18.99 million.

HDIN Institutional Perspective

Novonesis is fundamentally mispriced by analysts who continue to benchmark it against traditional specialty chemical peers (IFF, Symrise, Givaudan)—a cohort that saw a 25.4% market downturn in 2025. Novonesis is not a chemical company; it is an industrial software company where the code is written in microbial strains.

The early 100% run-rate realization of the Novozymes-Chr. Hansen cost synergies insulated the bottom line from severe EUR/USD currency headwinds. Management’s deliberate balance sheet engineering—temporarily spiking NIBD/EBITDA leverage to 1.9x via a bridge loan for the Feed Enzyme Alliance—is a calculated execution of accretive M&A. Supported by $871.01 million in free cash flow, deleveraging to the targeted 1.7x by 2026 is mathematically secure. Looking forward to the 2026 guidance (5–7% organic growth, 37–38% EBITDA margin, and elevated 12–14% CAPEX), Novonesis is visibly positioning its balance sheet to capitalize on the trough of the petrochemical cycle. As regulatory frameworks like the EU Chemical Strategy for Sustainability enforce biological substitution, Novonesis holds the apex pricing power.

Presentation Download & Video Access

* Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

* Video Link: Click this link to watch the YouTube video.

About HDIN Research

HDIN Research is a premier global market intelligence and institutional advisory firm. We specialize in forensic financial analysis, supply chain deconstruction, and macroeconomic strategic forecasting to provide unparalleled alpha generation for institutional investors and corporate strategists. Visit us at www.hdinresearch.com.

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.