SmartKem (Nasdaq: SMRT) Pivots to Trade-Secret OTFT Model as Liquidity Crisis Forces Total Patent Divestiture in Q1 2026

Date : 2026-04-11

Reading : 90

In Q1 2026, UK-based advanced materials developer SmartKem (Nasdaq: SMRT) executed a drastic corporate restructuring, divesting its entire patent portfolio to a third party to settle debt obligations. Operating with a mere 0.58-month cash runway ($374,000) and a $4.4 million working capital deficit at the close of FY2025, the company abandoned its patent moat in favor of 40 codified trade secrets. This intellectual property carve-out allows SmartKem to avoid immediate insolvency while pivoting its low-temperature TRUFLEX® organic thin-film transistor (OTFT) platform toward AI chip packaging and MicroLED commercialization alongside primary manufacturing partners in East Asia.

Financial Health & Operational Moats: The Capitalization Inversion

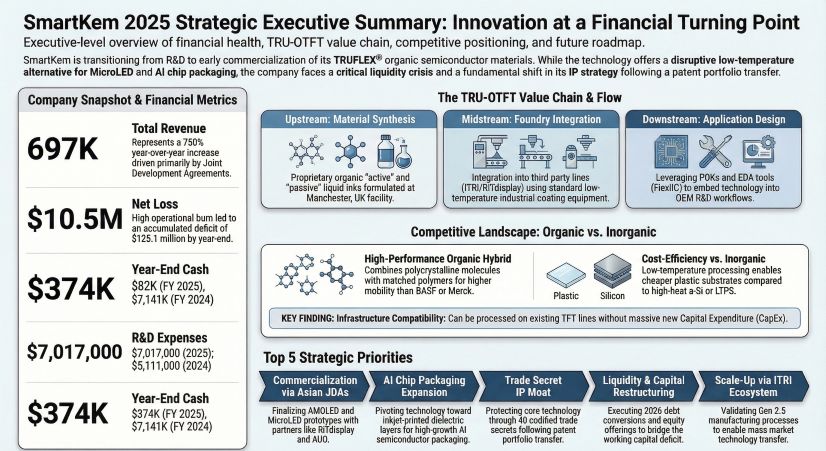

SmartKem concluded FY2025 in severe financial distress, triggering a "going concern" warning from auditors. While the company posted a year-over-year revenue increase to $697,000—driven predominantly by Joint Development Agreements (JDAs) with Chip Foundation and demonstrator material sales—its capital structure fundamentally eroded into a $(3.9) million stockholder deficit.

The structural inefficiency of SmartKem’s cost base is glaring. General and Administrative (G&A) expenses ($7.37 million) outpaced core Research & Development spend ($7.01 million). For a pre-commercial deep-tech entity, dedicating 51.9% of operating expenses to administrative overhead rather than innovation indicates a highly punitive compliance burden associated with maintaining a micro-cap public listing.

The "So What": To bridge a lethal $7.7 million annual cash burn, management executed a highly dilutive sequence of emergency capital interventions in Q1 2026. This included issuing $3.75 million in new Senior Secured Promissory Notes at a steep ~30% original issue discount with a 14% default interest rate, and establishing a $500 million Equity Line of Credit (ELOC). These predatory financing structures heavily dilute existing equity, meaning future commercial upside will be aggressively capped for minority shareholders. Furthermore, corporate governance reveals a severe disconnect: while management cited "fiscal constraints" as the reason for an un-remediated material weakness in internal controls, the compensation committee concurrently approved $280,659 in executive cash bonuses and doubled the CEO’s severance package.

Figure SmartKem 2025 Strategic Executive Summary: Innovation at a Financial Turning Point

Supply Chain Pivot: Trading Patents for Trade Secrets

Supply Chain Pivot: Trading Patents for Trade Secrets

To settle its October 2025 Senior Secured Notes, SmartKem executed an Intellectual Property Assignment Agreement in March 2026, irrevocably transferring its patent portfolio to SmartKem IP LLC. Consequently, the company's defensive moat relies entirely on 40 unpatented trade secrets surrounding its proprietary active organic materials and passive interlayer liquid inks formulated at its Manchester, UK facility.

This IP vulnerability is compounded by an extreme geographic supply chain dependency. Operating a fabless, asset-light model, SmartKem’s commercial viability is entirely tethered to outsourced manufacturing capabilities in Taiwan, Province of China.

* Process Scaling: The company relies on the Industrial Technology Research Institute (ITRI) for Gen 2.5 scale commercial manufacturing validation.

* End-Market Integration: High-margin growth targets are heavily reliant on localized partners, including RiTdisplay for AMOLED prototyping and Manz Asia for inkjet-printed dielectric layers utilized in advanced computer and artificial intelligence (AI) chip packaging.

Additionally, the European Chemicals Agency (ECHA) proposed ban on per- and polyfluoroalkyl substances (PFAS) threatens to legally prohibit SmartKem from manufacturing or selling its current formulations within the EU, functionally forcing the company into total reliance on Asian electronics ecosystems to bypass European chemical regulations.

HDIN Institutional Perspective: The Death of the Deep-Tech Zero-Interest Runway

SmartKem’s FY2025 audit serves as a bellwether for the broader advanced materials sector. The zero-interest-rate environment that historically subsidized multi-year, pre-revenue hardware R&D cycles has evaporated. SmartKem’s capitulation—liquidating its hard patent assets to clear $1.1 million in debt—demonstrates that material science firms failing to secure tier-one OEM purchase orders are being forced into punitive debt restructurings.

By losing its patent portfolio, SmartKem transitions from a proprietary technology licensor to a high-risk specialty chemical formulator. While its TRUFLEX® inks present a genuine solution to the CapEx and thermal limitations of traditional LTPS and amorphous silicon manufacturing, the company has lost leverage. With its technology now protected only by non-disclosure agreements, well-capitalized entrenched competitors like BASF and Merck KGaA are uniquely positioned to exploit SmartKem's weakened defensive posture. Should a larger conglomerate attempt a buyout for the remaining trade secrets, SmartKem’s staggered board and structural poison-pill mechanisms will likely prioritize executive severance acceleration over premium value generation for retail shareholders.

Presentation Download & Video Access

Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

Video Link: Click this link to watch the YouTube video.

About HDIN Research

HDIN Research is an independent strategic intelligence and corporate advisory firm delivering institutional-grade financial analysis, supply chain deconstruction, and geopolitical risk assessments. (www.hdinresearch.com)

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*

Financial Health & Operational Moats: The Capitalization Inversion

SmartKem concluded FY2025 in severe financial distress, triggering a "going concern" warning from auditors. While the company posted a year-over-year revenue increase to $697,000—driven predominantly by Joint Development Agreements (JDAs) with Chip Foundation and demonstrator material sales—its capital structure fundamentally eroded into a $(3.9) million stockholder deficit.

The structural inefficiency of SmartKem’s cost base is glaring. General and Administrative (G&A) expenses ($7.37 million) outpaced core Research & Development spend ($7.01 million). For a pre-commercial deep-tech entity, dedicating 51.9% of operating expenses to administrative overhead rather than innovation indicates a highly punitive compliance burden associated with maintaining a micro-cap public listing.

The "So What": To bridge a lethal $7.7 million annual cash burn, management executed a highly dilutive sequence of emergency capital interventions in Q1 2026. This included issuing $3.75 million in new Senior Secured Promissory Notes at a steep ~30% original issue discount with a 14% default interest rate, and establishing a $500 million Equity Line of Credit (ELOC). These predatory financing structures heavily dilute existing equity, meaning future commercial upside will be aggressively capped for minority shareholders. Furthermore, corporate governance reveals a severe disconnect: while management cited "fiscal constraints" as the reason for an un-remediated material weakness in internal controls, the compensation committee concurrently approved $280,659 in executive cash bonuses and doubled the CEO’s severance package.

Figure SmartKem 2025 Strategic Executive Summary: Innovation at a Financial Turning Point

Supply Chain Pivot: Trading Patents for Trade SecretsTo settle its October 2025 Senior Secured Notes, SmartKem executed an Intellectual Property Assignment Agreement in March 2026, irrevocably transferring its patent portfolio to SmartKem IP LLC. Consequently, the company's defensive moat relies entirely on 40 unpatented trade secrets surrounding its proprietary active organic materials and passive interlayer liquid inks formulated at its Manchester, UK facility.

This IP vulnerability is compounded by an extreme geographic supply chain dependency. Operating a fabless, asset-light model, SmartKem’s commercial viability is entirely tethered to outsourced manufacturing capabilities in Taiwan, Province of China.

* Process Scaling: The company relies on the Industrial Technology Research Institute (ITRI) for Gen 2.5 scale commercial manufacturing validation.

* End-Market Integration: High-margin growth targets are heavily reliant on localized partners, including RiTdisplay for AMOLED prototyping and Manz Asia for inkjet-printed dielectric layers utilized in advanced computer and artificial intelligence (AI) chip packaging.

Additionally, the European Chemicals Agency (ECHA) proposed ban on per- and polyfluoroalkyl substances (PFAS) threatens to legally prohibit SmartKem from manufacturing or selling its current formulations within the EU, functionally forcing the company into total reliance on Asian electronics ecosystems to bypass European chemical regulations.

HDIN Institutional Perspective: The Death of the Deep-Tech Zero-Interest Runway

SmartKem’s FY2025 audit serves as a bellwether for the broader advanced materials sector. The zero-interest-rate environment that historically subsidized multi-year, pre-revenue hardware R&D cycles has evaporated. SmartKem’s capitulation—liquidating its hard patent assets to clear $1.1 million in debt—demonstrates that material science firms failing to secure tier-one OEM purchase orders are being forced into punitive debt restructurings.

By losing its patent portfolio, SmartKem transitions from a proprietary technology licensor to a high-risk specialty chemical formulator. While its TRUFLEX® inks present a genuine solution to the CapEx and thermal limitations of traditional LTPS and amorphous silicon manufacturing, the company has lost leverage. With its technology now protected only by non-disclosure agreements, well-capitalized entrenched competitors like BASF and Merck KGaA are uniquely positioned to exploit SmartKem's weakened defensive posture. Should a larger conglomerate attempt a buyout for the remaining trade secrets, SmartKem’s staggered board and structural poison-pill mechanisms will likely prioritize executive severance acceleration over premium value generation for retail shareholders.

Presentation Download & Video Access

Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

Video Link: Click this link to watch the YouTube video.

About HDIN Research

HDIN Research is an independent strategic intelligence and corporate advisory firm delivering institutional-grade financial analysis, supply chain deconstruction, and geopolitical risk assessments. (www.hdinresearch.com)

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*